Happy Friday, traders. Welcome to our weekly market wrap, where we take a look back at these last five trading days with a focus on the market news, economic data, and headlines that had the most impact on gold prices—and may continue to into the future—as well as the charts for silver, the US Dollar and other key correlated assets.

Gold prices on Friday look to close the week at a healthy premium to Monday’s opening bids, as a mostly quiet final week of summer ends with a sharp rally for the yellow metal following the heavily watched August Jobs Report.

So, what kind of week has it been?

For the second week running, a relatively muted market week is closing out with a Friday banger—this time, it’s the release of the August Jobs Report headlined by an NFP number coming in well below the consensus expectation.

-

The US economy added just 235,000 new jobs in the month of August according to the Labor Department, a stark disappointment compared to expectations for a number above 700,000.

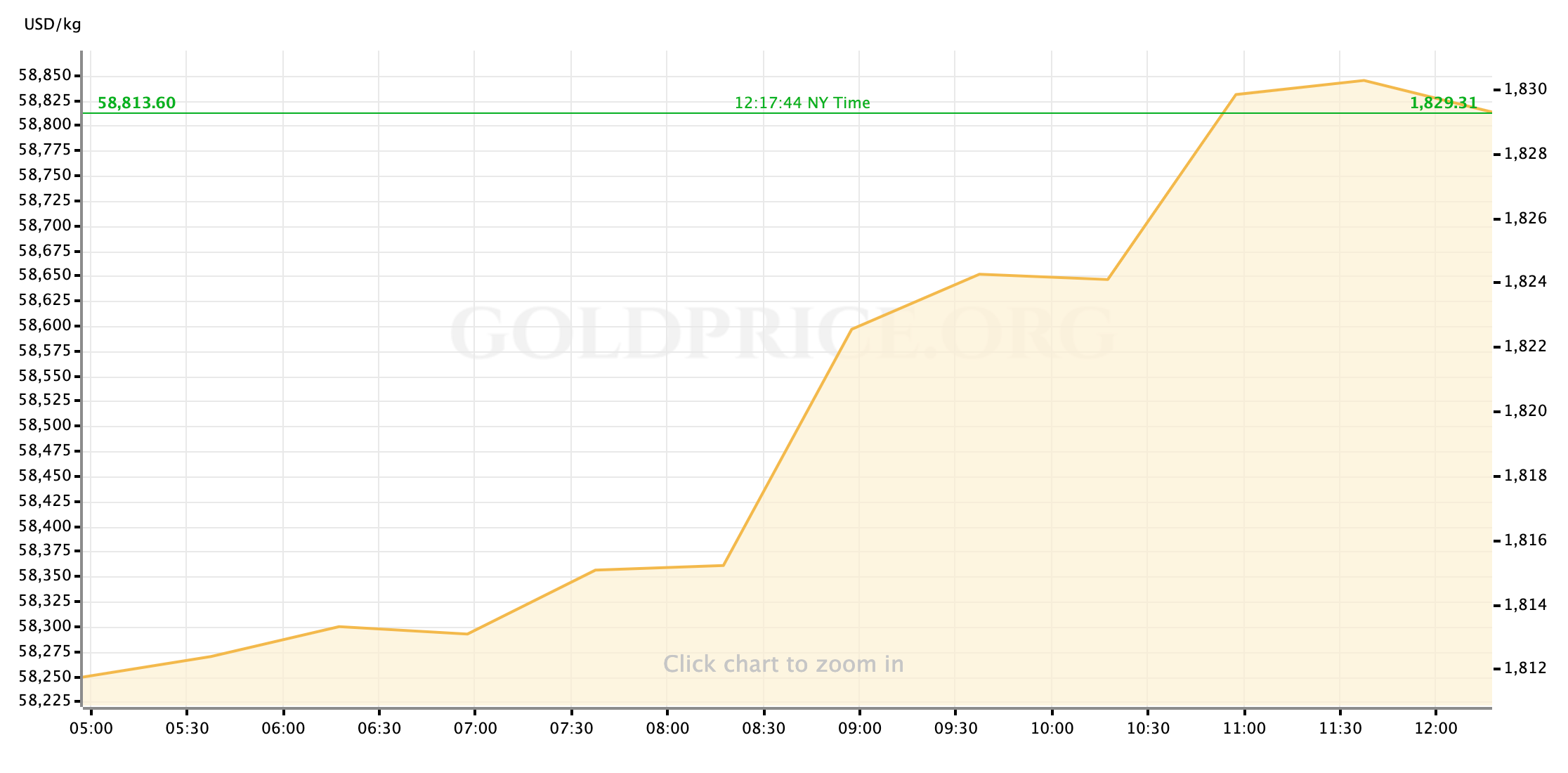

The gold market’s reaction to a labor recovery miss that will have to play into the Fed’s policy planning is in line with what we would have expected: from a Friday morning base around $1815, the spot rate for gold delivery ripped higher following the Jobs Report, initially picking up roughly $10/oz before consolidating and then rising higher again with the US market open.

-

At the time of writing, mid-session of Friday, the yellow metal’s spot price trades just shy of $1830/oz after pulling back a bit from the top.

Gold prices are likely benefiting from two tailwinds as a result of the NFP miss. Primarily, gold is rising because such a sudden stumble in the labor market recovery (at least in investors’ initial perception) weakens the case for the Federal Reserve to start slowly withdrawing monetary support for the overall economic recovery (by starting to taper) before the end of this year.

-

Whether the taper and eventual rate tightening are linked or not, the fact remains that any delay in starting the taper necessarily delays an eventual rate hike and locks in a more supportive (zero-rate) environment for gold prices for longer.

-

The implication of a delayed taper also weighs on the US Dollar, providing another mild counter-push to gold.

-

Of course, it was always unlikely that the Fed would announce a taper this month (September,) and investors were even starting to ease away from projections for November prior to Friday. So, markets haven’t been totally blindsided by the suggestion that the taper may be pushed into 2022; we can see evidence of this in the fact that investors haven’t taken gold on an unstoppable tear this morning and US equity markets, while off the pace in some sectors, aren’t experiencing a sharp downturn.

-

The last caveat to mention, but an important one, is that this is a Friday session ahead of a long weekend. It’s possible that Tuesday’s trading might see a stronger (over-)reaction to Friday’s NFP miss.

So, was the Jobs Report actually that bad? You’ll notice that, before now, I’ve only mentioned the NFP specifically. That’s because the overall unemployment rate actually fell, from 5.4% to 5.2%. Also, July’s NFP number was revised by more than 100,000 which pulled the total above 1 million; the report for August also shows wages continue to grow at a decent pace.

-

Taken as a whole, with a general awareness of what’s going on in the world outside of the US labor market, the August Jobs Report suggests that the labor market recovery has hit a snag, but one that we can almost entirely attribute to the summer surge of the Covid-19 delta variant across the US.

-

This is objectively bad, to be sure. But it also implies a very fixable problem, rather than a more systemic issue that would take more time (and probably more caustic measures) to pinpoint and correct.

-

With data starting to accumulate that suggests the current surge may have recently peaked, investors, and economists inside and outside of the Fed, will be even more focused on the next monthly Jobs Report (or two) in hopes that August’s stumble is an outlier in the economy’s trajectory towards recovery.

Though Friday’s catalyst for a gold rally was a disappointing macroeconomic data point, if reporting over the coming weeks suggests that the labor market recovery is able to resume as (hopefully) the US battles back against the delta variant, then gold prices may also benefit from the “reflation trade” that has been such a boon to equities and (at times) gold over the course of 2021.

On Tuesday (Monday is the Labor Day holiday for US markets,) we’ll kick off a truncated and presumably quiet(er) trading week with a sparse macroeconomic data calendar. As I mentioned earlier, the first focus will to watch how post-summer investors might rethink today’s (Friday’s) reaction to and repositioning around the NFP release.

For now, traders, I hope you can get out and safely enjoy your weekend for the next couple of days. After that, I’ll see everyone back here on Tuesday for our preview of the week ahead.

Gold Price Chart

More articles from John Moncrief