Good morning, traders. Welcome to our weekly preview of the market calendar, where we focus primary on the economic data and market narrative that could have the biggest impact on gold and silver prices, as well as the Dollar and precious metals’ other correlated assets.

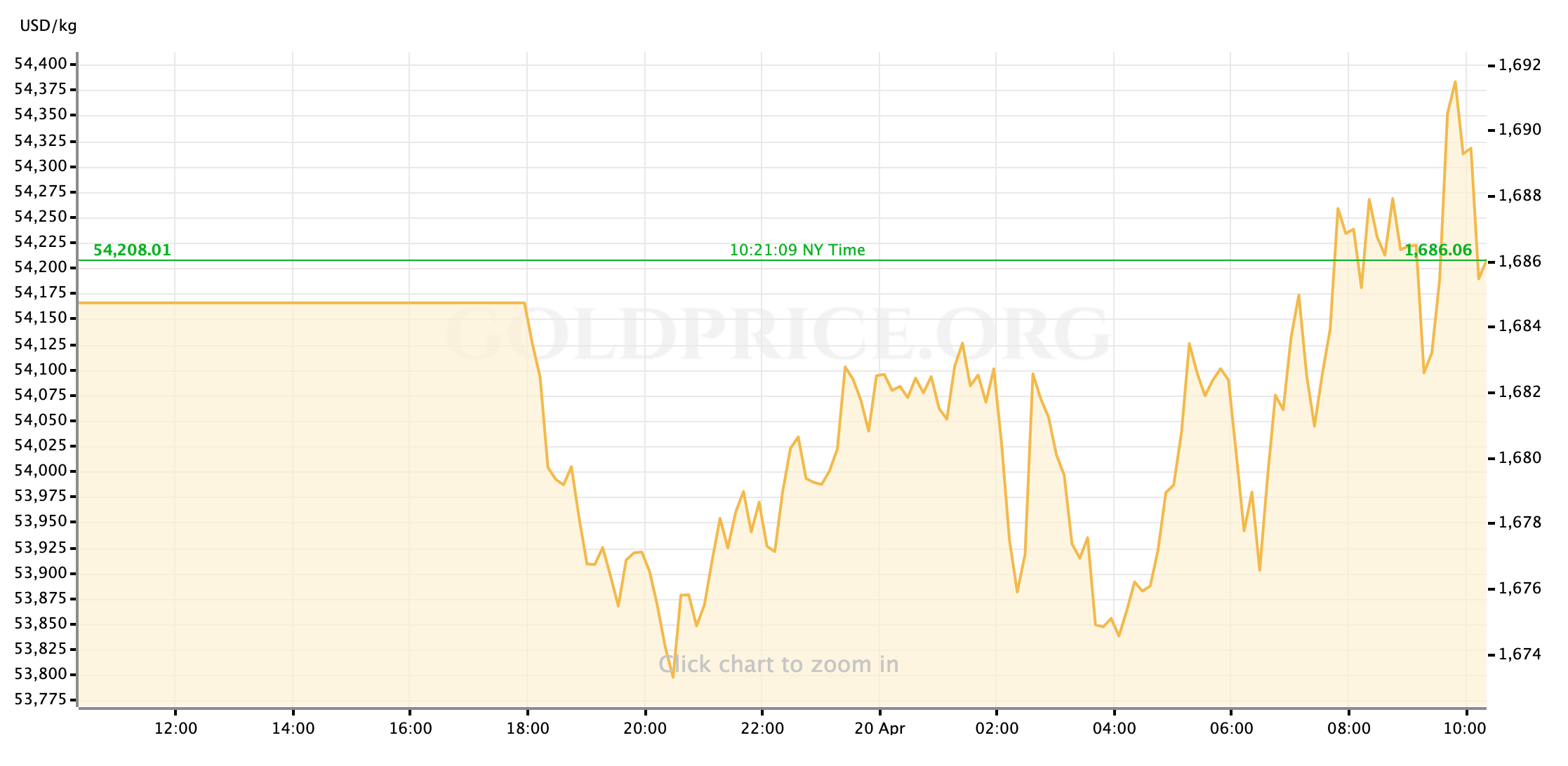

Precious metals prices are trading slightly higher compared to the global open for the week, with gold spot marking just below $1685/oz while silver prices sit near $15.25/oz after recovering from declines overnight. Gold prices had initially rallied on the start of equity trading in the US as the major stock indices have taken a step back, but the yellow metal’s advance was rebuffed at $1690 so we’ll watch for continued resistance at that level to start the week.

Some of the pressure on metals prices as well as US equities is coming from the crude oil market, where the headlines are bad and getting worse priced now collapsing to multi-decade lows.

Oil prices have dropped to their lowest level in more than 20 years, as the coronavirus crisis continues to eat away at demand and storage tanks in the U.S. are nearing their limits. https://t.co/Ry8zbUoJ4F pic.twitter.com/QVqZVyZJGU

— CNBC (@CNBC) April 20, 2020

As the world continues to battle against the Covid-19 pandemic in hopes of making moves towards resuming a version of “normal” economic activity, it looks like a real paradigm shift in energy markets may be another market narrative that impacts metals pricing this week.

For now, let’s have a look at the economic data on order in the days ahead.

US Economic Data to Watch

Tuesday, April 21 at 10am EDT // Existing Home Sales (Mar)

[consensus expectation: -9% MoM // previous: +6.5%]

Last week’s data on Housing Starts marked a 35-year low for one of the US housing market’s key metrics as one of the persistent bright spots in the US economy’s historic expansion of 2009-2020 took a battering from the “closing” of economic activity compelled by efforts to fight the coronavirus pandemic. Safe to expect, then, that Existing Home Sales for the same month will be punishing as well. Based on the reaction to last week’s housing data, and the pull of risk markets’ attention towards monetary/fiscal action and more specific Covid-19 data sets, I expect this report will be supportive of gold prices but not a strong catalyst for move higher.

Thursday, April 23 at 8:30am EDT // Initial Jobless Claims

[consensus exp.: 4,500k // prev.: 5,245k]

Here’s something I never really expected to say: analysts and economists this week are hoping to see a mild reprieve from weekly jobless claims dipping back below 5 million. Still, 4 million isn’t going to kick off a tickertape parade (although something like that would probably create at least a few new jobs,) so I’m looking for this week’s release to hold gold prices steady. I don’t think anything above 3,000k (or 3 million) drives risk-appetite, but I’m wary that another print with a 5-handle might ratchet up the fear gauge unexpectedly—the tough part lately is guessing which way that would push gold prices. If gold spot is still below $1700/oz, I imagine higher claims will drive prices higher in a standard safe-haven bid; if the yellow metal has risen above $1700 by Thursday, we may see a repeat of last Thursday when ugly economic data encouraged investors and managers to liquidate profitable gold positions in a rotation to cash and US debt.

Thursday, April 23 at 9:45am EDT // Markit Manufacturing & Services PMI (Apr)

[consensus exp. (mfg.): 38.0 // prev.: 48.5]

[consensus exp. (svc.): 31.3 // prev.: 39.8]

A month ago, the Markit PMI for the US manufacturing sector didn’t reflect as a deep a fall for March as was expected but given the ugly regional PMI data we saw last week it seems safe to assume that the bill comes due this time. I think that preceding regional data has inured the risk markets to any big shock from seeing a manufacturing number in the 30s, but to have the service sector component threaten to fall below 30 will probably be another risk-off signal this week. Once again, the question is whether that impulse means investors rotating into gold for protection, or out of it for cash. By the time Markit’s data prints mid-morning, we’ll have seen the gold market’s reaction to Initial Jobless Claims and should be better able to judge which dynamic is in play.

Friday, April 24 at 8:30am EDT // Durable Goods Orders (Mar)

[consensus exp.: -12.0% MoM // prev.: +1.2%]

The math for Durable Goods Orders in March looks pretty easy, and we don’t have to parse out the airline orders or industrial equipment either: under the constrictions of a global effort to arrest the spread of Covid-19, almost nobody inside or outside the US is ordering long-term capital goods, and practically nobody is manufacturing them during the shutdown. Orders are going to be down across the board, shipments will be down more. I expect this data set is very priced into the markets right now, so without a big shift in positioning (in gold or risk assets) over the next few days I’m not looking for a big reaction on Friday’s print.

Global Economic Data to Watch

As opposed to the US-centric slate, the rest of the developed world has a lot of macroeconomic data updating this week. They most interesting run for our purposes will come in the earliest hours of Thursday morning, as Markit reports its PMI numbers for most of Europe (and the Eurozone as a whole.) On the continent things are expected to look dire, with the composite PMI for the whole of the common currency area expected to fall to 25 or lower. The UK’s data is expected to be “less bad” but not an improvement. It’s possible that before trading starts in earnest in the US, we could see Europe and London-based managers moving to safety in gold, Treasuries, or debt. Most of the PMI numbers will be released between 3-4am EDT.

And that’s how the week lays out for us, traders. As always, I wish you the very best of luck in your markets this week. I’ll look forward to seeing everyone back here on Friday for our weekly market wrap.

Gold Price Chart

More articles from John Moncrief