Good morning, traders. Welcome to your preview of the macroeconomic week ahead for precious metals and currency traders.

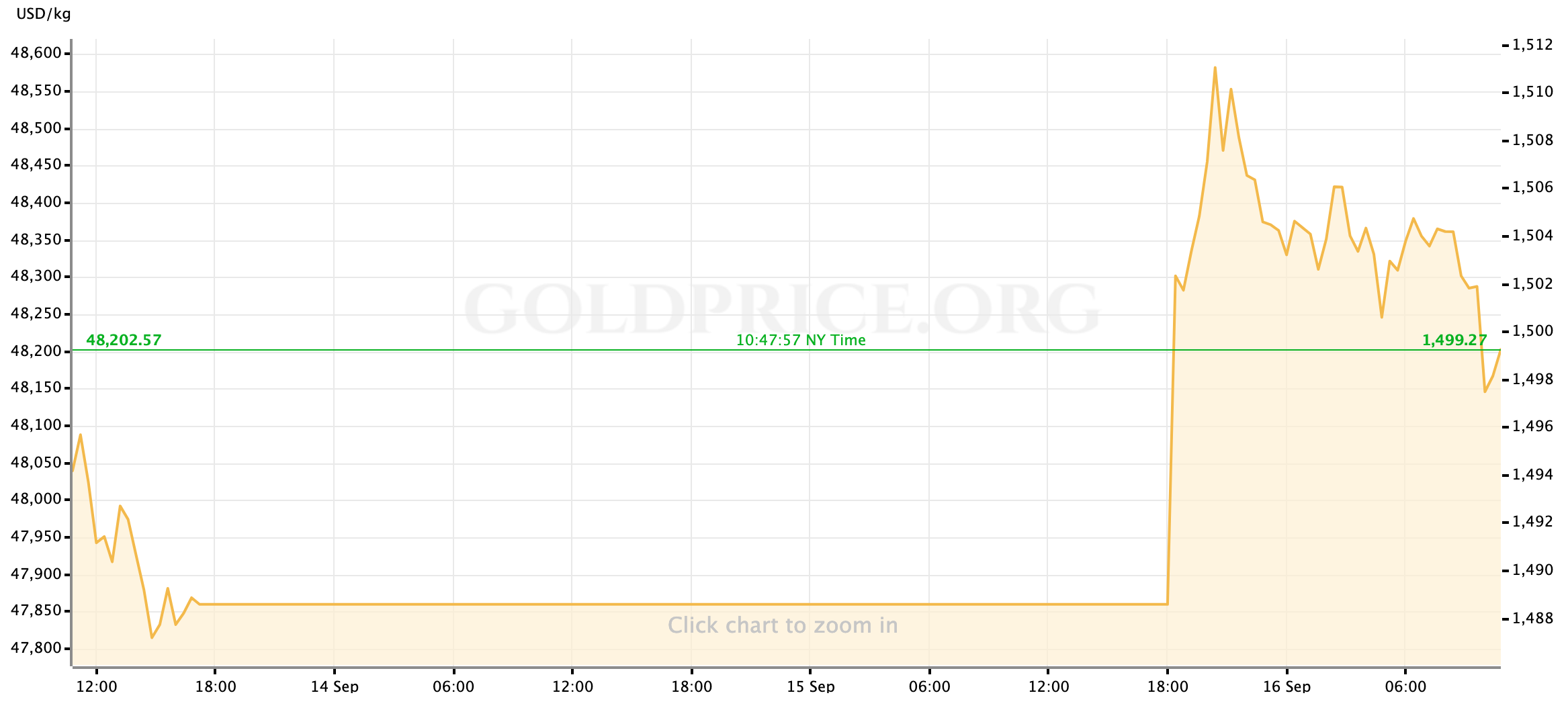

Gold spot prices are trading just below $1500/oz this morning, roughly $10 higher than last week’s closing price and the same $10 or so below the high points reached in overnight trading. Silver is currently going for $17.83/oz.

The fast action in precious metals to start the week is wholly driven by the sudden injection of geopolitical risk into markets as, over the weekend, a terrorist attack on a Saudi oil facility effectively knocked out 5% of global supply. Brent crude futures contracts made their biggest-ever leap higher when the global commodities markets reopened Sunday evening and major safe haven assets like gold jumped alongside them—spot prices for the yellow metal reached as high as $1512/oz during the Asian session.

Since that outsized move, we’ve seen a reasonable pullback from the highs; after all, the market was trading a news story that had changed little since breaking over the weekend so there was only so much fuel to be burned (no pun intended.) Perhaps surprisingly, with gold prices back around the $1505 level the open of US equities markets has seen the US Dollar become the lead runner for the day and that counterbalance drove gold prices quickly below $1500 again.

The unfolding story of this attack, as well as the timetable for the Kingdom’s oil production to get back to 100%, will be added to our list of stories to watch this week. The primary of which is still the next actions in the US-China trade conflict; an outsized spike in oil prices is likely to pile unwanted pressure on the Beijing delegation so those developments may look different this week than they would otherwise have. Just ahead of, and then after, the FOMC meeting on Wednesday we’ll also be adjusting our expectations for the rate path and the later late stages of this US economic expansion.

For now, let’s have a look at what else is on the calendar.

US Economic Data to Watch

Monday, September 16 at 8:30am EDT // NY Empire State Manufacturing Index (Sep)

[consensus expectation: +4.0 // previous: +4.8]

[actual: +2.00]

The Empire State index has strung a couple positive months together since June’s surprisingly ugly data, and the data for September is largely expected to continue that trend. On the surface this looks like another argument for the idea that we were all a little too panicky about the US manufacturing sector at the beginning of the summer, but we shouldn’t overlook the fact that the “bounce back” numbers are struggling to hold onto a 4-handle. For perspective, a year ago the Empire State number was running much closer to +20.0.

My red flag waving aside: coming as it does on the Monday of a major Fed week, I don’t anticipate Dollar or metals markets to react much to this data point without a major upside or downside surprise. Still, the usual correlation is expected to hold: weak manufacturing data is a tailwind for gold, while the opposite is true of strong data.

[This data point was released prior to posting our article. While it disappointed expectations, as we supposed it went largely ignored by the market amid all geopolitical risk-trading this morning.]

Tuesday, September 17 at 9:15am EDT // Industrial Production (Aug)

[consensus exp.: +0.2% MoM // prev.: -0.2%]

So far this year, there have been more months of contraction than expansion in Industrial Production, but a negative handle on this number is not very uncommon over longer time horizons. This can pretty often be an easy to ignore number for Dollar and gold traders.

That said, this month’s Industrial Production read does print just ahead of a big Fed meeting. I really don’t think the Fed (as a committee) is going into this week so on the fence about cutting 25bp or 50bp that the final decision will be made by manufacturing data, but the market as a less rational hive-mind might ascribe a little more importance to the data this time around anyway, and that could make rates-correlated assets like gold a little extra sensitive to a surprisingly strong or weak print.

Wednesday, September 18 at 8:30am EDT // Housing Starts (Aug)

[consensus exp.: +4.4% MoM // prev.: -4.0%]

Housing Starts data should continue humming along, as supporting data for August (an uptick in construction jobs, lower mortgage rates) points to a rebound from July’s pull-back.

Wednesday, September 18 at 2pm EDT // FOMC Interest Rate Decision

[FOMC is expected to cut short-term rates by 25bp.]

As “important” as this FOMC meeting is, the general consensus among traders and analysts doesn’t reflect a great deal of change beyond the headline. Regardless of “Fed futures” or what the US stock market (thinks it) wants, most observers anticipate a repeat of July’s 0.25% rate cut rather than a more aggressive 50bp. Beyond that, the committee’s statement isn’t expected to include many revisions and the quarterly economic projections aren’t expected to reflect major changes to the outlook.

Of course, the smart money will have learned a valuable lesson from July’s Fed Week. Namely, that the market may not shift on the announcement of a fully priced-in rate cut from the FOMC, but it very well could be roiled by the White House’s reaction to Jerome Powell & Co.’s decisions.

Thursday, September 19 at 8:30am EDT // Philadelphia Fed Manufacturing Index (Sep)

[consensus exp.: +10.8 // prev.: +16.8]

With the Philly Fed’s manufacturing survey expected to continue reverting lower from a blowout report in July, a deeper drop than expected could be a point of concern. Likely as not, though, this data point will be overshadowed by the after-effects of Wednesday’s FOMC. Unless there’s some language from the Fed that puts a great deal of dependence on how growth in the manufacturing sector is doing, anything other than a major upside/downside surprise shouldn’t move metals or Dollar markets a whole lot this time around.

Thursday, September 19 at 8:30am EDT // Initial Jobless Claims

[consensus exp.: +214k // prev.: +204k]

Friday FedSpeak

The FOMC members’ commentary rounds look like they’re beginning a little early this month, with these three scheduled appearances all on Friday:

- 8:15am EDT: New York Fed President John Williams (FOMC voter)

- 11:20am: Boston Fed President Eric Rosengren (FOMC voter)

- 1pm: Dallas Fed President Robert Kaplan (non-voter)

Typically, I would point out the NY Fed chief Williams’ comments as those with the most potential to be relevant to markets, but it’s an oddly closed-door appearance which is expected to be closed to the press so it may be next week before we see anything from it. In that light, Rosengren’s remarks on the credit cycle look the most worthy of attention.

Global Economic Data to Watch

Wednesday, September 18 at 11pm EDT // Bank of Japan Interest Rate Decision

[no change to monetary policy is expected.]

Thursday, September 19 at 7am EDT // Bank of England Interest Rate Decision

[no change to monetary policy is expected.]

As has been the case all summer, we’re not expecting any material changes to policy to be announced (or even really alluded to) from these two central banks this week. Aside from traders focused on their constituent currencies, the market’s attention will be on the banks’ statements and projections; with the Bank of England’s turn on Thursday morning we’ll have gotten through a full cycle of major central bank meetings and from there begin doing our best to determine what effect these new rounds of monetary easing will do to the global economy, as well as envision what the next moves may be.

And that, traders, is how the big week lays out ahead of us. I wish you the best of luck in the metals and currency markets this week. I’ll see you all mid-week for a recap of Wednesday’s FOMC meeting, and then for our usual Friday breakdown of the week’s events.

Gold Price Chart

More articles from John Moncrief