Happy Friday, traders. Welcome to our weekly market wrap, where we take a look back at these last five trading days with a focus on the market news, economic data and headlines that had the most impact on gold prices—and may continue to into the future—as well as the charts for silver, the US Dollar and other key correlated assets.

Gold prices are trading at a slight premium to their opening bids to begin the week. In the face of a slowdown in other key commodities and a sudden, strong mid-week headwind created by aggressive inflation data on Wednesday, the yellow metal has overall managed to consolidate near the weekly highs.

So, what kind of week has it been?

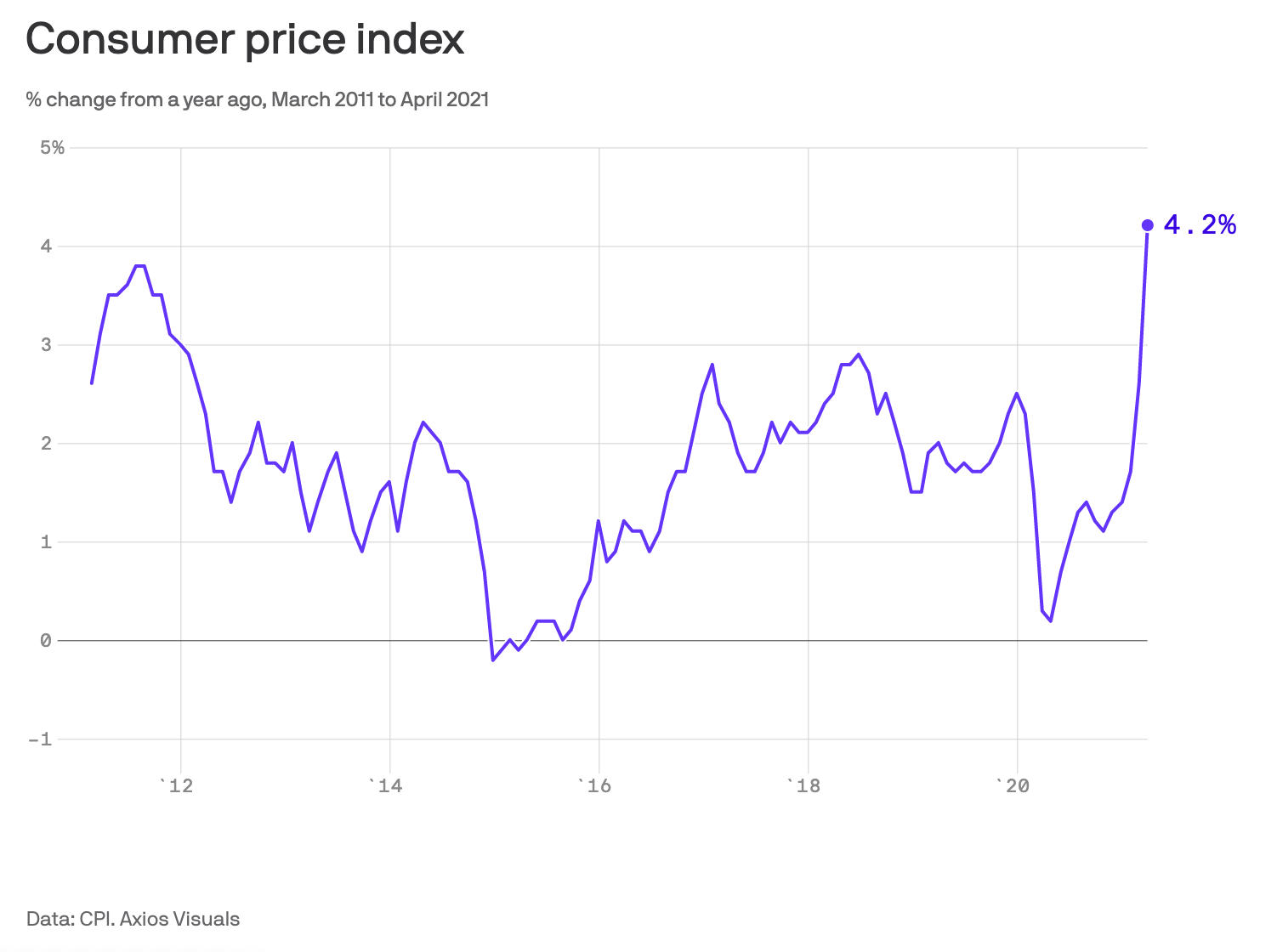

The biggest surprise of the week was the major upside surprises laced throughout Wednesday’s CPI (consumer inflation) report for April. The significant “core” inflation rate came in at a blockbuster 3% (YoY) while the more volatile headline number printed an equally surprising 4.2% (a 13-year high.) The magnitude of the surprise relative to expectations left analysts and investors reeling and confounded as to how the consensus estimates were so wide of the mark for a second major data set.

- After last week’s shockingly poor labor market data I had the hubris on Monday to predict that the release of April’s inflation data would be a relatively inert event for markets. I imagined the proof that the US economy has so much farther to go before reaching “full employment” would, for now, negate any implications that relatively high inflation pops might pressure the Fed into tightening policy (raising rates) earlier than projected. Looking at Wednesday’s trading, I was clearly wrong.

- Having recovered from some acute profit-taking the day before, gold prices fell sharply on Wednesday following the CPI print. The yellow metal closed its trading session at the bottom, near $1815/oz; Wednesday-to-Thursday overnight markets allowed the trend to run a bit farther to a weekly nadir just above $1810.

- The counterweight to gold’s fall was, of course, a corresponding surge in Treasury yields as the entire “reflation trade” that has steered market trends for weeks decompensated.

Though it would prove to be temporary, US stocks panicked for fear of hyperinflation choking off the 2021 recovery. All three major indexes shed at least 2% on Wednesday, with the tech-dominant NASDAQ falling closer to 3%.

- My error—and learning opportunity—was not accounting for the kneejerk reaction that quick-on-the-draw human traders and computer algorithms might have to a sudden, multi-year high in the primary gauge for inflation, entirely (or mostly) independent of how it might adjust the Fed’s policy path.

With the initial surprise worn off, when we look into the actual data presented on Wednesday on its own, it actually should change very little about the economic outlook for the rest of the year: It’s still more than reasonable to assume that what we’re seeing in April’s numbers is a ‘transitory’ (to use the Fed’s favorite adjective for current inflation pressure) unwinding of the damage done to 2020’s economy by the Covid-19 pandemic.

- The components of CPI that most drove April’s surge bear this out: Used vehicle sales (which jumped the most on record going back more than 65 years) and travel components (like vacation lodging airfares) were driven acutely higher, respectively, by supply chain issues and vaccinated Americans’ rush to get away from the homes they’ve been sheltering in for over a year. Both inputs should start to smooth out over the summer as the global supply chain works out the kinks created by the return of mass-demand and last spring’s shutdown-crippled economic data gets phased out of the year-over-year comparisons.

What was true on Monday remains true here at the end of the week: We expected a surge in inflation in April, even if the one that came was some order of magnitude bigger than anticipated; But the CPI report that really matters now is the next one, which will give us the points of comparison we need to be able to say with more confidence that these price pressures on the economy are only passing—or else grapple with the possible reality that things may be getting too hot in the US economy.

- I’m still far more inclined to side with the Fed in saying that this will pass. That said, it’s worth noting that this week’s raft of public comments by FOMC officials included at least one prominent participant admitting to being caught off guard by the strength of this week’s inflation data.

However US stock markets might’ve characterized their fears of inflation that had seemed to weigh on stock prices all week before dropping them sharply lower following Wednesday’s macro data, on Thursday they seemed to have shrugged them off completely. Yields on US Treasuries pared back roughly half of the gains from the day before, and all three equity benchmarks finally closed a trading session in the green.

- As US-based traders took over the market early Thursday morning, gold prices rose steadily from their trough, and continued to strengthen through the day. Overseas traders would continue on the positive trend for both gold and global equities during their Friday sessions. As Asian and European stock markets made gains to close the week, gold spot prices by Friday morning (in New York) had more than erased the midweek loses.

- Thursday’s abrupt pivot, as Bloomberg points out, suggests that we may be in for some push-and-pull in the equity markets over the next month as investors and economists alike do battle over weather rising inflation (at this exact moment in time) is a boon or a bother for stocks.

Further suggesting that Wednesday’s inflation-panic was more than a bit premature, Friday’s Retail Sales data for April was, on its face, a bit of a disappointment, reporting 0% growth month-to-month. In reality, the +1% pick up that analysts had projected could be found in a revision higher in last month’s very strong headline number.

- The reflation/re-opening trade appears to be back in full-swing on Friday, with the Dow and the S&P 500 well on their way to gains of more than 1% to close the week while the NASDAQ, making up for its lagging performance this week, is up more than 2%.

- Gold trading has been a little bit more muted since the Retail Sales report, but the yellow metal has continued to move higher on the day. At the time of writing, gold is making a challenge to retake the highs of the week above $1841/oz.

Looking ahead to next week: From a macro data perspective things are pretty light; But when it comes to the next moves in the gold market I’ll be tracking some other factors that have become relevant over the last several trading sessions.

- Although the reflation trade looks to be back at a strong pace going into next week, many of the globes primary raw commodities which had been participating in the rally since February have slowed over the last few trading days. Base metals in particular, like iron ore and copper, are down considerably from recent highs. Likewise, crude oil and recently-ripping lumber prices are off the pace on Friday. Gold, so far, has maintained strength in the face of this, although silver is (as can be expected) appearing weaker. I’ll be watching next week, should this pullback in the broader commodities complex persist, when or if it might become a headwind that gold traders need to reckon with.

- With spot prices for gold looking likely to close Friday’s session at or above the weekly high, I’ve got an eye out for profit-taking and other signs of significant resistance around this level on the yellow metal’s chart. In Tuesday’s trading, we saw an oddly sudden rush of selling to gold that, because it doesn’t seem to have aligned with movement in other correlated assets, I (and others) generally wrote off as profit-takers cashing-out. Whether it’s at the end of this week’s trading, or sometime early next week, if the same pattern repeats near $1840 then I’ll have to wonder if gold’s recent rally might be topping out without any new catalysts.

For now, traders, I hope you can get out and safely enjoy your weekend for the next couple of days. After that, I’ll see everyone back here on Monday for our preview of the week ahead.

Gold Price Chart

More articles from John Moncrief