The Philadelphia Federal Reserve released its manufacturing index on Thursday, gauging business activity in the region. The index shot up from 2.4 to 17 in January, punching its way to an 8-month high. Economists had predicted a virtually flat reading of just 2.8, making the index’s jump away from borderline-negative territory all the more significant.

Key Takeaways

- The Philadelphia Fed manufacturing index rose from 2.4 to 17 in January vs. 2.8 expected.

- New orders, shipments, and the six-month business outlook all saw increases in the ISM in January.

- Despite ongoing contraction in the ISM manufacturing index, regional indexes are showing strength.

The Philadelphia Fed manufacturing index is based on a standalone question regarding business conditions, unlike the ISM index which combines multiple component surveys. Current general activity rose 15 points from a revised reading of 2.4 in December to 17.0 in January. 39% of firms reported increases, while 22% reported decreases. Current shipments rose 8 points, and new orders rose 7 points. Unfilled orders and delivery times sunk into negative territory in January, indicating shorter delivery times and a reduction in unfilled orders. Inventories also declined slightly.

Philadelphia Fed Manufacturing Outlook jumped 15 pts in Jan to 17. New orders and shipments both saw 7-8 point jumps. Prices also showed signs of improving. Expectations improved as well but not as robustly. https://t.co/qqM1R8eJiw pic.twitter.com/KnATeHyZfW

— MTS Insights (@MTSInsights) January 16, 2020

Employment reportedly increased from 3 points to 19.3, with 28% of firms reporting higher employment vs. 9% reporting lower. The average workweek dipped 3 points. Prices paid rose overall, although 78% of firms reported no increase for their particular business. In terms of outlook, 49% of firms anticipate increased activity this year vs. just 11% expecting reduced activity. Future new orders and shipments rose by 8 and 4 points respectively, although future employment dropped 3 points.

The ISM saw new orders rise 7 points to 18.2 in January. Shipments rose 8 points to 23.4, and the six-month outlook rose from 34.4 to 38.4. However, the ISM overall has been contracting for 5 months in a row, while regional indexes like the Empire State and Philly Fed manufacturing indexes are performing better. It’s possible that the data shows that the East Coast is less reliant on Chinese trade than other regions, The ISM factory reading fell to the lowest point since the last recession in December, falling to 47.2.

Market Reaction

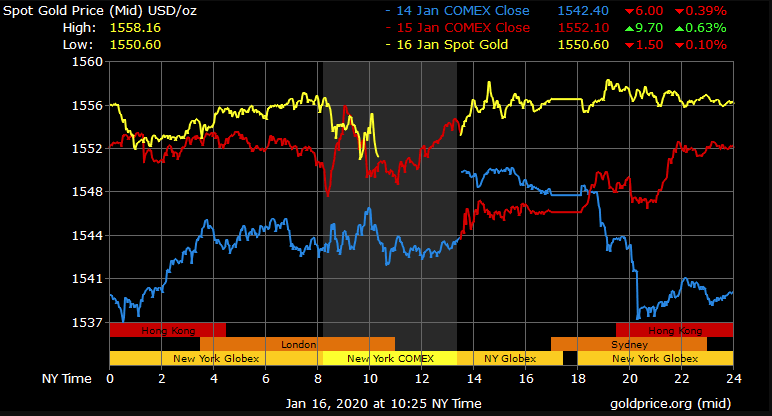

Gold prices have seen downward momentum since the release of the report, although continue to trade toward the higher end of today’s range. Spot gold last traded at $1,550.60/oz, down 0.10% with a high of $1,558.16/oz and a low of $1,550.60/oz. With unexpectedly strong retail sales and a reduction in initial jobless claims, the upbeat economic data released today is likely resulting in increased risk appetite throughout the stock and precious metals markets.

Gold Price Chart

More articles from Conor Maloney