Happy Friday, traders! Welcome back to you recap of the week in metals and currency markets.

At the time of writing, gold is settling in for the close of a monumental August that has seen spot prices reach and surpass six-year highs on our way into the more tumultuous months of September and October.

So, what kind of week has it been?

Gold & Silver Prices Rebounded Sharply on Tuesday as Trade-War Worries Persistently Persist

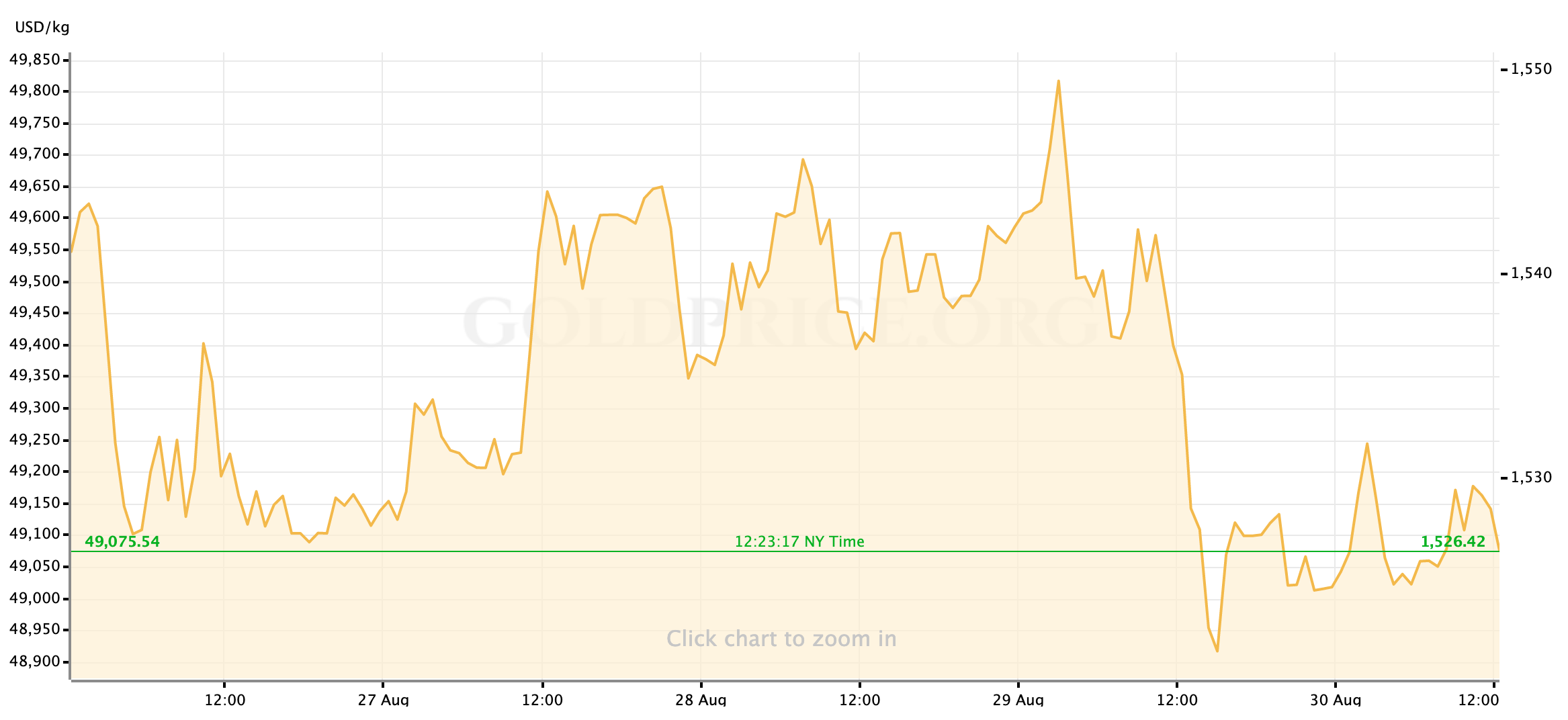

The gold market remained largely unchanged after our weekly preview post through to the end of Monday’s trading: the risk-off wave that was unleashed after the weekend’s headlines tempered by a combination of the Chinese government signaling that they still wanted a “calm” resolution to the trade war and Donald Trump claiming that they (China) were on the phone and desperate to talk again, gold prices had come down roughly halfway from their overnight high-ticks. From there, through to the commodities’ market close and then up to the start of European trading, prices were steady around the $1528/oz level. Remarkably, the feeling of economic confidence that lifted the US stock markets to start the week in the black managed to survive a whole trading day’s worth of time for the market and analysts to consider the veracity of the US president’s claims—it even made it through a live press conference that required Donald Trump to interact with foreign press.

By Tuesday morning in New York, of course, the jig was up. In the early hours of the day, Chinese government officials made it known through one channel or another that they had asked around and, hey, nobody really knew anything about these plaintive phone calls that Donald Trump (and Donald Trump alone) was talking about. That blow to market hopes for positive steps in the trade talks (or even just, you know, trade talks) combined with once again renewed concerns about the stability of Italy’s government, and really worrying growth data from Germany led to buyers stepping back into the gold charts. As US equities began (and would ultimately end) the day with loses the yellow metal trade back above $1530 an ounce, near to the mid-August highs for spot price.

As risk and safe-haven markets gave some attention to sorting out the opposing impulses provided by Tuesday’s US macro data—tepid data from the housing market; stronger than expected reporting on the manufacturing sector-- the day’s real price gains for precious metals would come later in the US morning as those loses on the Dow and S&P solidified, and the market’s news cycle for the day came into focus: not only was it becoming impossible to verify the president’s claims, but that dubiousness was being blamed for the stock market weakness.

U.S. stocks turn lower, S&P 500 Index gives up session gains https://t.co/gv9QNl4KZv pic.twitter.com/WQVylhyzqg

— Bloomberg Markets (@markets) August 27, 2019

Equities remained soft throughout the day (while avoiding a complete freefall,) as the US-10yr’s yield collapsed below 1.5%; at the same time, gold prices reached back towards $1545.oz on the spot charts while silver prices remained on an absolute tear, surging well past $18.

Gold prices would lose a bit of momentum towards the end of Tuesday’s session, and drift down from what started to look like a top just below $1545, but buyers would step back in ahead of the commodities close. From there, $1535/oz looked to be the new level of support going ahead.

As Markets Calmed on Wednesday, Gold and Silver Prices Drifted Lower

Wednesday’s trading as firmly banded within the $10 range that firmed up after Tuesday morning’s market anxiety, with nearly every tick of the gold chart from the Asian market open to the evening’s global commodities close falling between $1535-45/oz. The day’s most active gold trading occurred around the cash open for US equites, which initially saw an uptick in buying but quickly became a brief test of the support at $1535 as stocks leapt onto the good foot—each major US exchange would end the day in the green after Tuesday’s rough-go. Once our yellow metal rebounded from that support, there wasn’t much to talk about in terms of price action for the remainder of the session as most spot trades executed within touching distance of $1540/oz.

There was some headline action, of course. The most dramatic sounding of which was (new) British Prime Minister Boris Johnson’s government announcing that they would suspend parliament for a large portion of the time remaining between the end of summer recess (next week) and the current drop-dead date for Brexit (Oct. 31.) While this BoJo power move seemingly narrows the number of possible outcomes to three (Britain crashes out of the EU on Halloween; Boris manages minor renegotiations of the divorce agreement with the EU mid-October and then bullies it through Parliament; or, Boris’ growing opposition wins a no confidence vote in early October and forces a general election…which revives a multitude of possible outcomes,) exactly what this means for major assets like gold and the US Dollar is still a little hard to pin down. Except, of course, to say that volatility in the British Pound is way up, with Sterling dropping nearly 1% against the Greenback on Wednesday.

The British pound plunged on Wednesday morning after PM Boris Johnson sought to suspend Parliament.

More via @business https://t.co/wozcioaBNH pic.twitter.com/nUWLAs4f8m

— Bloomberg TicToc (@tictoc) August 28, 2019

Wednesday also delivered out dose of FedSpeak for the week, with the Richmond Fed President Tom Barkin saying he doesn’t feel that the current low readings for inflation compel the central bank to cut rates further. While Barkin is a non-voter in this year’s FOMC cycle, I do think he is echoing the views of more than a few of his fellow committee members—but then, it’s not really a surprise to learn that there will be some division within the Fed about how to proceed come September. Fellow non-voter, SF Fed President Mary Daly, gave an address on managing inflation and indicated that her preference is to let an economy (or at least the US economy) run a little hot; so while it’s seemed in recent comments that she’s not in a rush to cut interest rates again, it also appears that Daly will not be arguing to adjust them higher any time soon either.

Gold Support Collapsed on Thursday as China Sought to Cool Trade Tensions

Around the time of the European open for Thursday, gold spot prices made a strong but brief and ultimately unsuccessful attempt to break above $1550/oz, and that looks to have been the yellow metal’s last attempt at reaching higher highs before we move into the typically more volatile month of September.

In the same overnight/early morning hours, the spokesman for the Chinese Ministry of Commerce brought some calm to the market-roiling trade war, saying in public remarks that his side “firmly reject an escalation of the trade war, and are willing to negotiate and collaborate in order to solve this problem,”. Gold’s upward momentum, having looked a little tired this week at the end of a wild month, finally seemed to give up the ghost as risk markets were bolstered by this idea that at least one side of the trade conflict is interested in cooling things down. The yellow metal and other more risk-off trades gave one more kick Thursday morning stateside as a second look at 2Q GDP for the US surprised us by revising the growth rate down a bit; ultimately, when this last gasp petered out gold prices collapsed through $1535 support.

There was a point in the early afternoon where it looked like gold might test $1520, but as trading has smoothed out through Thursday evening into Friday morning it does look like the new level of support lies somewhere between $1525-28/oz.

Gold Prices Settling at the End of an Audacious Month of Gains

As we wrap-up the final trading day of August, gold prices have moved broadly sideways from Thursday’s breakdown. We are, at the time of writing seeing a lift back to $1530/oz. While it’s hard to judge just how energetic this move is—it will inevitably be countered by not only end-of-week profit-taking but end-of-month as well—it seems to be spurred on by US equities slumping a bit this morning and turning into the red to wrap the month. Also giving gold a lift: silver, stretching back towards $18.40/oz at the tail end of its own very profitable month.

Friday’s economic data all arrived uneventfully: monthly measures of Personal Income are generally flat when accounting for revisions while the more important metric of Person Spending was on the rise, and the PCE view of inflation remains unmoved from recent months.

Next Up

The calendar for next week is one of those oddly back-loaded Jobs Report weeks where nothing much seems to be on the schedule (aside from IHS sector data) until the big NFP and unemployment release on Friday; I’m sure it’s only amplified by the short holiday week.

I’m a little unsure about what to think about precious metals’ prospects over the next week. While not as messy as a week ago, we certainly do have some weekend risk while the markets are closed: China has signaled that they’re committed to find a calm resolution to things, but also that they have the capacity to retaliate if they feel the need to; and a number of new punitive US tariffs on Chinese goods will still go into effect on Sunday.

But even before Thursday’s softening in gold price, it had started to feel like the major risk-off assets like gold and silver were becoming desensitized to headline risk and general market fretting. A lot of doom and gloom signaling was floating around out there this week—the “key” US Treasury spread reached its deepest inversion since 2007, the UK Parliament and it’s new government seem hell-bent on playing a game of chicken that tests the limits of its constitution, and a not-unimportant former member of the Fed openly argued for the FOMC to work against the US president. Things are…worthy of concern; but we didn’t’ commit much (or any) digital ink to these stories this week gold prices never much looked very likely to take a run above $1550.

Maybe it’s fatigue after all the ground gold prices have covered this month, or maybe the market is just seeing through the first-level effects of these headlines and figuring out that things could just as easily go back to “normal” in short order (for the record, I’m much more inclined to believe the former.) Either way, I’m not sure gold has a lot of rocket fuel left until or unless the economy takes another measurable step backwards. Barring that, the background hum of general worry will probably support gold spot around the $1515-1525/oz level but on the upside looks to be capped at $1545.

Hopefully, all this really means for the next three days is that we can take a breath and enjoy our long Labor Day weekend. That’s my hope for you at least, traders. After that, I’ll see you back next week for a look at the week ahead.

Gold Price Chart

More articles from John Moncrief