The US has seen record layoffs for the second week in a row, with initial jobless claims more than double those of the previous week as well as double all expectations. The week ended March 28 saw more than ten times the number of layoffs than any other week in US history, according to the latest report from the Labor Department. Claims came in at 6.65 million vs. 3.31 million the week before and 3.3 million expected. For comparison, the week before last saw 220,000 layoffs.

Key Takeaways

- Initial jobless claims, a measure of layoffs, rose 6.65 million last week, far worse than any mainstream economic prediction.

- Claims were revised upward to 3.31 million for the week before last.

- Businesses have shut down throughout the US, which is now the global epicenter for the coronavirus pandemic.

Economists say the economy has now entered a recession, with virus containment measures closing down much of the economic infrastructure nationwide. Restaurants, offices, and many businesses deemed non-essential have implemented self-isolation measures either by choice or government mandate in different states. The longest ever period of economic expansion in US history is now over.

B OF A: The recession appears to be deeper and more prolonged than we were led to believe just 14 days ago .. We now believe that there will be three consecutive quarters of GDP contraction with the US economy shrinking 7% in 1Q, 30% in 2Q and 1% in 3Q. .."

— Carl Quintanilla (@carlquintanilla) April 2, 2020

Over 80% of Americans are now under lockdown of some kind, up from 50% in March. State governments have reported IT issues with the sites used to file for claims, as the influx of unemployed people is so high that it has been crashing the systems.

4,000 Americans have died to date from the coronavirus, with 188,000 confirmed cases and many more likely unconfirmed. US President Donald Trump made statements on Tuesday estimating that 100,000 to 240,000 Americans will die of the virus even if containment procedures are followed.

OMG. Jobless claims at 6.6 million. More than double the estimate of 3.1 million analysts expected, which in itself would be horrific. The American job market is in free fall.

— Eamon Javers (@EamonJavers) April 2, 2020

The labor market crisis has nearly matched the number of jobs lost in the Great Recession in the last two weeks alone. 8.7 million jobs were lost between the 2007 – 2007 financial crisis. Recently-introduced government policy has allowed self-employed contractors to claim unemployment, where previously this was not possible, and this has inflated the numbers and shown the true scale of the labor crisis.

12.5% Unemployment on the Cards

JP Morgan Funds chief global strategist David Kelly stated “A rough look at the most affected industries suggests a potential payroll job loss of over 16 million jobs. The loss would be enough to boost the unemployment rate from roughly 3.5% to 12.5%, which would be its highest rate since the Great Depression.”

Some economists have pointed to the disparity in the government stimulus package of $600 per week, amounting to $15 per hour for a 40-hour workweek, and the minimum wage of $7.25 per hour. “Why work when one is better off not working financially and health wise?” said a Sung Won Sohn, a business economics professor at Loyola Marymount University in Los Angeles.

“The U.S. labor market is in free-fall,” said Gregory Daco, chief U.S. economist at Oxford Economics in New York. “The prospect of more stringent lockdown measures and the fact that many states have not yet been able to process the full amount of jobless claim applications suggest the worst is still to come.”

This chart is a portrait of disaster. I have spent the last twenty years studying the labor market and have never seen anything like it. Unemployment insurance claims for the last two weeks are mind-blowing. 1/ pic.twitter.com/IoRYyraW0V

— Heidi Shierholz (@hshierholz) April 2, 2020

“Based on our read, 22 states are expecting approximately 2.5 million unemployment insurance claims, up from the prior week’s official nonseasonally adjusted figures of 1.4 million,” said Joseph Song, a U.S. economist at Bank of America Securities in New York.

“Meanwhile, several other states have given general guidance that claims will be higher in the upcoming report. A rough back-of-the-envelope calculation extrapolating out to all 50 states would imply close to 5.6 million new applications.”

Market Reaction

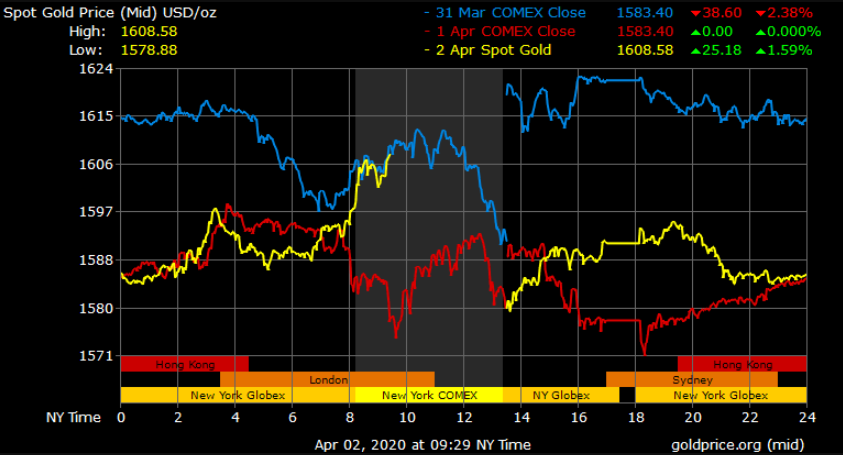

Gold prices have seen upward momentum following the release of record layoffs in the US for the second week in a row. Spot gold last traded at $1,608.58/oz, up 1.59% with a high of $1,608.58/oz and a low of $1,578.88/oz. The catastrophic labor market conditions are more than enough to create bullish sentiment in the precious metals markets. Labor underpins consumer spending, which accounts for two-thirds of the US economy.

However, while President Trump warned on Tuesday that the US was in for a “very, very painful” two weeks as the virus reaches its expected peak in mid-to-late April, it’s possible that an economic recovery can begin in May. The feasibility and success of such a recovery will depend on the efficacy of the virus containment procedures currently in place.

Gold Price Chart

More articles from Conor Maloney