Gold and silver prices are considerably higher this afternoon following the final FOMC meeting of the year, from which the Federal Reserve left rates unchanged following three consecutive rate cuts while also updating their Staff Economic Projections.

Interest Rate Decision: Rates Hold in Place

The Fed, in its first unanimous vote since May, said it will continue to monitor the implications of data for the economic outlook “including global developments and muted inflation pressures.” https://t.co/9cTm6DrAax

— Bloomberg (@business) December 11, 2019

For the first time in several months. It’s pretty simple to recap that moves made by Jerome Powell & Co following this month’s FOMC meeting: they didn’t make any. As was widely expected following November’s final piece of the “mid-cycle adjustment” triptych—and solidified by last week’s knockout Jobs Report among other recent data—the Fed has decided to leave short-term interest rates where they are to close out a tumultuous 2019; said the committee in the published statement,

“The committee judges that the current stance of monetary policy is appropriate to support sustained expansion of economic activity, strong labor market conditions, and inflation near the committee’s symmetric 2% objective,’’

The rest of the FOMC’s statement reflected the committee’s view of current monetary policy as “appropriate,” with the removal of language about specific risks to economic growth (which had spurred the 0.75% total reduction in policy rates) accounting for most of the changes. Even so, the group is committed to monitoring developments around “global developments and muted inflation pressures” going forward.

Economic Projections: Most FOMC Participants See Rates on Hold Through 2020

With the market as a whole anticipating a no-action Fed decision, the focus this month was firmly on the updated Staff Economic Projections and, in particular, the anonymous dot plot of participants’ projections of the policy rate path. The median of those projections now shows short-term rates remaining unchanged through the entirety of 2020, with a single 0.25% rate hike in both 2021 and 2022. Importantly for our medium-term outlook for monetary policy, while there are some FOMC members who feel a hike in 2020 will be appropriate they are decided in the minority.

MORE: Just 4 Fed officials project rate hikes in 2020 now, but several still see hikes as being appropriate in 2021 and 2022, according to the latest dot plot.

The latest on today's decision ➡️https://t.co/Lfv48WScl0 pic.twitter.com/olj7sWFdhJ

— Bloomberg Economics (@economics) December 11, 2019

The market appears to agree—for now—with the futures market currently pricing in the next adjustment as a rate hike in the first half of 2021. This is unchanged from earlier today, before the Fed announcements, which contributed to the relatively muted initial reaction in rates, stocks, and gold charts.

Other projections included in the Fed’s update forecasting included:

- Unemployment expected to remain at the current 3.5% through late 2020, while long-run unemployment has been adjusted down to 4.1%.

- Fed-measured inflation projected to reach 2% in 2021 (unchanged from previous projections.)

- US GDP growth projected to +2% next year and +1.9% in 2021 (also unchanged from September)

Chairman Powell’s Press Conference: The Bar for Rate Hikes is High

While the reaction across most major markets to the FOMC announcement was relatively calm, most of the velocity around asset prices came in response to Chairman Powell’s press conference, and his comments that unofficially set the bar for a return to Fed-tightening:

Powell: "We think our policy rate is appropriate and will remain appropriate as long as incoming data are keeping in with our outlook.

In order to move rates up, i would want to see inflation as persistent."

— Brian Cheung (@bcheungz) December 11, 2019

While Powell made it clear that this was an expression of his own views, it’s unlikely he would make such a clear statement if he were in the minority within the committee; so, not only would it take elevated inflation to warrant a rate hike, but persistently elevated inflation. That’s a pretty high standard to meet and solidifies the projection for lower rates for longer.

Market Reaction

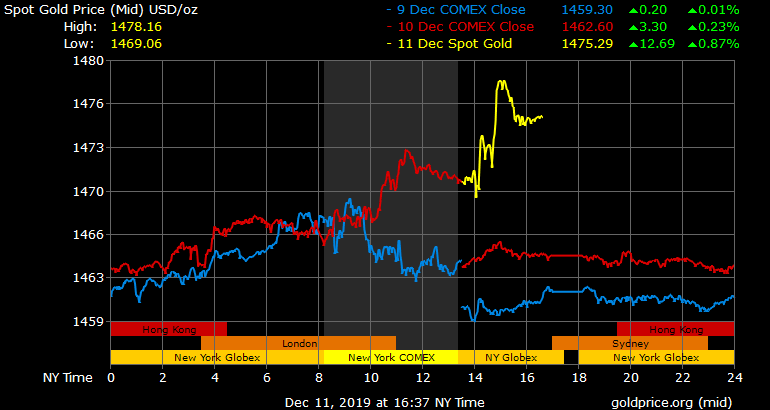

With the strong odds that we’re going to remain in this lower-rate environment for a while the stocks are trading higher as equity markets celebrate the promise of easy money; meanwhile bond yields are dipping while gold continues its run higher. Despite some short-term profit-taking that has pulled the yellow metal down from its highs during Powell’s presser, sport prices are heading into the close with a solid grip on $1475/oz. The US Dollar looks to be the big loser for the day.

With US-China trade tension far from settled (and an update on plans for the next scheduled round of tariffs expected tomorrow,) we’ll be looking to see if gold prices can build for another move higher before financial markets wind down ahead the holidays.

Gold Price Chart

More articles from John Moncrief