Hello traders, welcome back to our weekly preview of the relevant macroeconomic data for those active in the gold, silver, and currency markets.

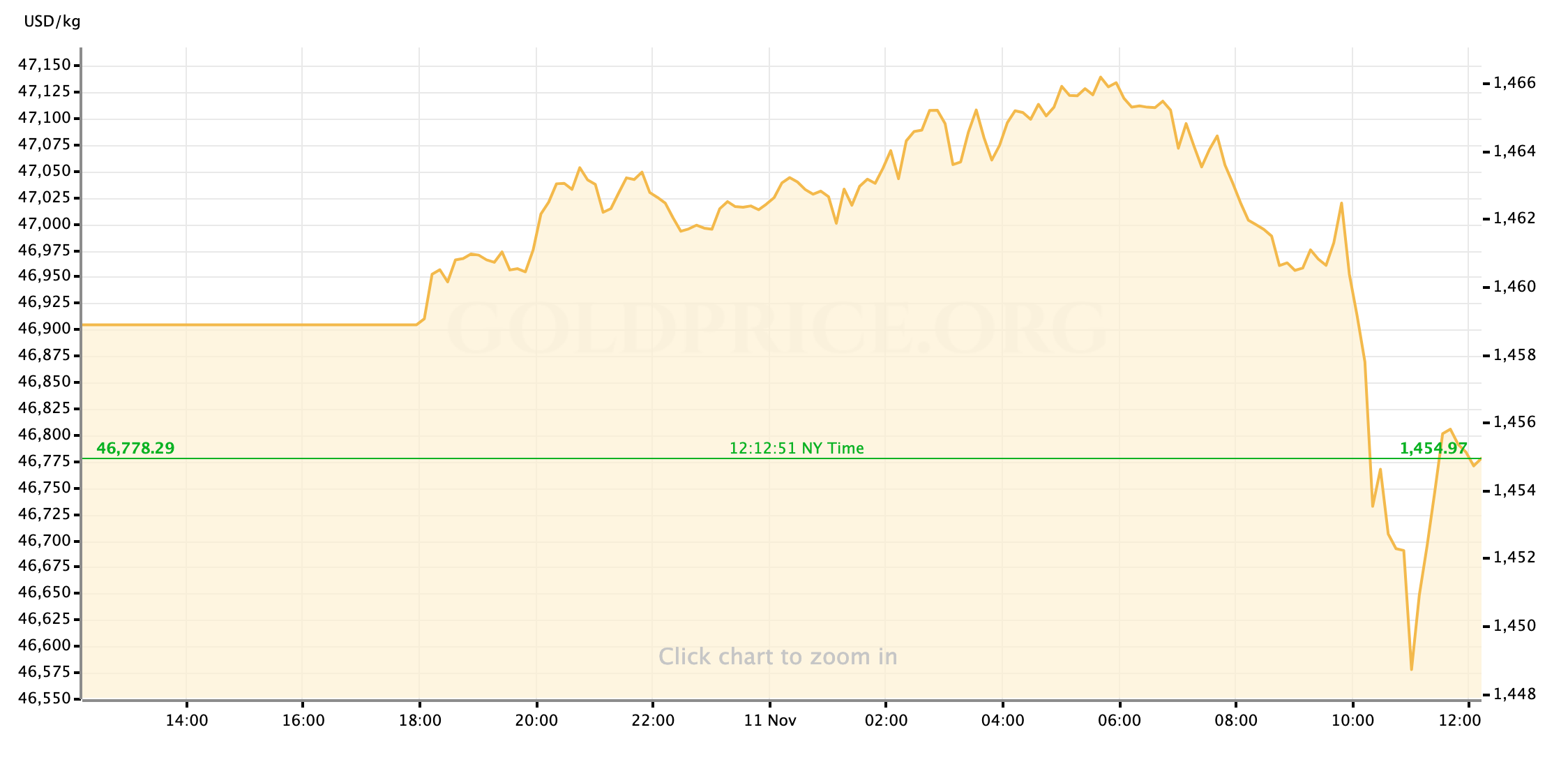

Gold prices are lower this morning but recovering following some aggressive selling at the start of US cash trading that saw the yellow metal falling past three-month lows and silver briefly dipping below $16.75/oz as well.

Based on the timing, pace, and subsequent recovery from the sell-off it seems like a reliable assessment to say this was the result of an initial round of selling in the futures market that triggered stop orders on the way down and accelerated the move.

Gold futures tumbled to a three-month low as contracts equal to over 3 million ounces changed hands in half an hour https://t.co/5jmXUpEBhG pic.twitter.com/ECddH1ulFD

— Bloomberg Markets (@markets) November 11, 2019

This isn’t uncommon on holidays like today, Veterans Day, in which bond markets are closed. It’s unlikely that we would see a repeat of the same move again today, but there are always some odd trades on days with low liquidity.

With that in mind, let’s have a look at our relatively light economic calendar for the week.

US Economic Data to Watch

Wednesday, November 13 at 8:30am ET // Consumer Price Inflation (Oct)

[(core CPI) consensus expectations: +2.4% YoY // previous: +2.4%]

[(headline CPI) consensus exp.: +1.7% YoY // prev.: +1.7%]

In what could become a consistent theme for economic data this week, markets appear prepared for a fairly uneventful reading of consumer inflation for the month of October, with core inflation (as well as the more volatile, inclusive of food an energy prices, headline number) expected to deliver the same annualized rate as the prior month. Peripheral price gauges support this view, as do anecdotal observations that overall economic conditions are little changed month-to-month.

Anticipating unchanged numbers might increase the odds of market sensitivity to a disappointing print, or a surprise to the upside, but in the markets’ current mood I think it would need to be a pretty considerable (let’s say bigger than 0.3% in either direction) dislocation to force a marked move in Dollar or gold markets.

Wednesday, November 13 at 11am ET // Federal Reserve Chair Powell Testimony

FOMC Chairman Jerome Powell appears for his regularly scheduled testimony before the Joint Economic Committee (and then the House Budget Committee on Thursday.) Knowing how carefully spoken Powell is—and, generally speaking, how technically clumsy many of his examiners tend to be—there’s a low probability of language from the Chair that moved markets on Wednesday (this is doubly true for Thursday.) That said, as usual there will be some attention on Powell’s prepared opening remarks; those should be released in text roughly an hour before the hearing begins.

Thursday, November 14 at 8:30am ET // Producer Price Inflation (Oct)

[(headline PPI) consensus exp.: +0.3% MoM // prev.: -0.3%]

[(core PPI) consensus exp.: +0.2% MoM // prev.: -0.3%]

Analysts this month see the producer-focused read of inflation rebounding from a pull-back in September, lifted by a rebound in core prices and higher energy costs. For gold and Dollar traders, I suspect this month’s PPI will only be meaningful as an echo of Wednesday’s CPI data: if consumer price inflation prints in-line with expectation, this release can probably be slept-through; but if CPI disappoints then the market may be looking for confirmation on Thursday about broader concerns in the system.

Thursday, November 14 at 8:30am ET // Initial Jobless Claims

[consensus exp.: +215k // prev.: +211k]

I was kind of surprised by the gold market’s willingness to react, however briefly, to a 1-month low in jobless claims last week— typically, you wouldn’t see a chart move on a change of 4,000 claims. I’m interested to see if there will be the same sensitivity to this week, whether it’s a confirmation or correction.

Friday, November 15 at 8:30am ET // Empire State Manufacturing Index (Nov)

[consensus exp.: +6.0 // prev.: +4.0]

Still just keeping an eye on these higher-value surveys of regional manufacturing and will probably continue to do so for as long as Manufacturing PMI remains in contractionary territory.

Friday, November 15 at 8:30am ET // Retail Sales (Oct)

[consensus exp.: +0.2% MoM // prev.: -0.3%]

Retail numbers for the month of October should also be able to rebound from a drop in the prior month, according to most analysts, with lower sales in the automobile category presenting the only real drag. I expect there to be a lot of market attention on retail data for the next couple months—even with the US holiday season putting its thumb on the scale as usual—because of how aware most investors and traders are about the importance of the American consumer at this point in the economic cycle. Any shudder or pull-back in Retail Sales—especially during holiday shopping—could certainly send buyers flowing back into risk-off assets like gold.

Friday, November 15 at 9:15am ET // Industrial Production (Oct)

[consensus exp.: -0.4% MoM // prev.: -0.4%]

Analysts expect to see the impact of the autoworkers’ strike pass-through into the October data. With greater energy drawn into Retail Sales data earlier in the morning, Dollar and gold markets might largely ignore this release if there’s not a large up- or downside surprise to it.

Fed Speak this Week

Week Two of FedSpeak rolls on, getting started in earnest on Tuesday. Last week’s rhetoric didn’t provide much to trade on, and I think it’s possible that we see the same this week although there will be the usual run of headlines around Chairman Powell’s congressional testimony (which we touched on above.) As always, here are the public appearances this week that I feel merit a mention:

Monday, November 11: Boston Fed President Eric Rosengren (FOMC voter) (8:15am ET)

Tuesday, November 12: Federal Reserve Vice Chair Richard Clarida (FOMC voter) (5:30am ET); Minneapolis Fed President Neel Kashkari (non-voter) (6pm)

Wednesday, November 13: Minneapolis Fed President Kashkari (1:30pm ET); Philadelphia Fed President Patrick Harker (non-voter) (7:30pm)

Thursday, November 14: Federal Reserve Vice Chair Clarida (9am ET); Chicago Fed President Charles Evans (FOMC voter) (9:10am); New York Fed President John Williams (FOMC voter) (12pm); St. Louis Fed President James Bullard (FOMC voter) (12:20pm)

Global Economic Data to Watch

Wednesday, November 13 at 4:30am ET // UK Inflation (Oct)

[(headline inflation) consensus exp.: +1.6% YoY // prev.: +1.7%]

[(core inflation) consensus exp.: +1.7% YoY // prev.: 1.7%]

As I touched on in last week’s wrap-up, I find it interesting that there seems to be some growing concern within the Bank of England that rate cuts will be needed; and that it becomes a relevant narrative for gold prices, in the event that the FOMC is putting a hold on short-term rates (if not raising them, at some point) while the rest of its major trading partners (Europe, Britain, Japan—and, yes, China) are easing policy. This kind of differential would build some serious support into the US Dollar, creating a strong counterweight to gold prices. With all that in mind, I’ll be keeping an eye on UK inflation this week less as a possible immediate mover of the gold chart, and more as part of a long-term narrative.

And that’s how your week ahead looks, traders. I wish you the best of luck in your markets this week, and I’ll look forward to seeing you back here on Friday for our recap of the action and headlines.

Gold Price Chart

More articles from John Moncrief