The manufacturing industry has sunk further as a result of the coronavirus pandemic according to the latest report from the Philadelphia Federal Reserve. The Philadelphia Fed manufacturing index came in at -43.1 vs. - 47.5 expected for May following a reading of -56.6 the month before when the index hit a 40-year low. While business conditions have improved slightly, the pace of recovery is below market expectations.

Key Takeaways

- The Philadelphia Fed manufacturing index measured business activity at -43.1 vs. 47.5 expected.

- 58% of firms reported decreases while just 15% reported increases.

- New orders rose 45 points from the all-time low seen last month to -25.7, and the six-month outlook forecasts overall improvement.

Manufacturing firms in the region reported a slight uptick in improvement, though major indexes are still well below zero. The six-month outlook remains fairly upbeat, with a record discrepancy with current activity, shown below.

Source: Philadelphia Fed

Manufacturing firms expect the current slump to last less than six months, anticipating overall growth in new orders, shipments, and employment during that time. Currently, the indicators for general activity, new orders, shipments, and employment are below zero, but all showed improvement from the lows seen in April.

The index for general activity rose 13 points to -43.1, the third negative reading in a row. 58% of firms reported decreased activity vs. 15% of firms reporting increased activity. New orders rose from -70.9, an all-time low, to -25.7, with one in four firms reporting an increase in new orders and half reporting decreases. Current shipments rose 44 points from the all-time low of -74.1 to -30.3. Unfilled orders remained flat at -13.7, and delivery times fell 11 points to -6.7, which indicates shorter delivery times and perhaps less disruption in national and international supply chains.

Philly Fed Manufacturing firms reported "continued weakness" in May https://t.co/Tpv1GdjIg8 pic.twitter.com/rWwAt5Fkx9

— Bill McBride (@calculatedrisk) May 21, 2020

Prices paid rose 13 points to 3.2, with more firms seeing higher prices than lower prices. Prices received rose 8 points but remained in negative territory at -3.1. Firms were asked this month to forecast changes in their own prices, and overall, the consensus is that prices should rise slower than inflation.

Strong Future Outlook

The index for future general activity rose 7 points to 49.7. 62% of firms forecast increased activity over the next six months compared to just 13% expecting reduced activity. New orders for the next six months are forecast to improve 18 points, with no change to future shipments. The index for future inventories rose fell 15 points to negative territory at -1.4. 35% of firms forecast increased employment in the next six months vs. 18% forecasting a reduction in payroll. Expectations for employment remained in positive territory overall, but dropped 10 points.

Market Reaction

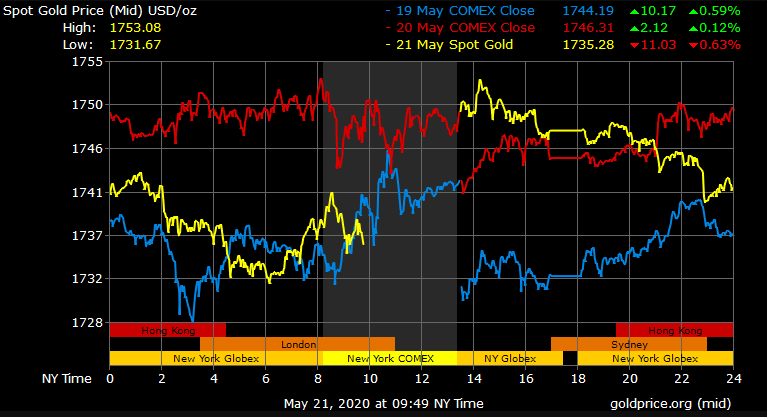

Gold prices remain in the mid $1,700s, facing mild selling pressure following the release of the report. Spot gold last traded at $1,735.28/oz, down -0.63% with a high of $1,753.08/oz and a low of $1,731.67/oz. The latest initial jobless claims report showed another 2.4 million Americans applied for claims last week, in line with expectations.

While the state of manufacturing and employment remains somewhat bleak according to the reports released on Thursday, there have been no major surprises in the financial markets today, with fewer traders turning to gold as a hedge against risk.

Gold Price Chart

More articles from Conor Maloney