Now that we’ve all awoken from our turkey and nog-laden comas and started getting those trading legs back under us to start the year, it’s time to have a look ahead at what macroeconomic stories are most likely to have in impact on precious metals markets in 2019. What follows is a list of macro drivers and events that, in my estimation, are the most likely to have the biggest impact on gold pricing in 2019 (and possibly moving forward.) Under each heading I’ve elaborated a bit on the set-pieces in each narrative as well as how I believe gold markets would react.

To get started, the gold-correlated market I will pay the most attention to in 2019 is, without question, the health of the US economy and the US Dollar.

Here is my breakdown of the four macroeconomic stories most likely to impact gold prices in 2019:

1.) The Shine Comes Off of The US Economy

One of the strongest headwinds against gold and silver prices has been a strong—at times, unreasonably strong—US Dollar.

While this has been the case (in the current cycle) going back as far as 2014, for today’s purpose we’re more interested in discussing the greenback’s strength over the last year. Heading into 2018, growth in the US economy was healthy and moving at a good clip just as was the case in many other developed economies. Still, the Dollar was particularly strong against its G7 partners at time due in large part to the expanding divergence in monetary policy. While the central banks of the Japan, the UK, and the EuroZone economy were still hip-deep in measuring of quantitative easing, in America the Federal Reserve had not only exited QE but was already on the path to actively tightening monetary policy. This results in the US currency not only strengthening it its own right, but also increasing in value in direct comparison to it’s major trading partners in the developed world; as the flagship of an economy that was not only improving, but was already healthy, the US Dollar was easily the more valuable currency to hold.

As we moved forward through 2018 and the Fed continued hiking short-term interest rates, growth in the American economy began to slow down a bit even if the buoyant equities market did not (now comes another great opportunity to ring the large bell with “The Stock Market Is Not The Economy” stenciled onto it forwards and backwards.) Nonetheless USD maintained a steady upward trend through the majority of the year, this time not just because of divergent monetary policy (although that gulf remains wide,) but because of an increasing gap in economic growth—while other economies in the developed world were starting to stumble and slow (and emerging market economies continued to struggle) the US economy was slowing to a much lesser degree and so the Dollar’s value remained high relative to its classmates even as it was becoming more and more evident that things were being graded on a curve.

As we ended 2018 and began this year the prospects for the US economy and its Dollar have begun to dim. US equities spent December in turmoil to deliver an historically poor performance for the year as a whole, while even most of the economic data that had remained resilient throughout the year began to “catch-down” to the more pessimistic mean. As a result, it looks more and more likely that we have move to, and through, “peak Dollar” over the last few months.

This turn downward in the value of the dollar, should it occur, will be driven largely by the inversion of the very same factors that fueled it’s rise: US growth continuing to slow and catching-down to the rest of the word; the FOMC pausing its interest rate hikes, if not beginning to lower them outright. Other drivers of a decline in the broad US Dollar could include: the creeping inversion of the US yield curve signaling a potential recession on the horizon, the fading “sugar rush” of the White House’s tax cuts, and the further deterioration of US-China trade.

In an environment where the dollar is a considerably weaker investment government debt no longer offers the promise of increasing yield, gold becomes a much more enticing investment not only for savers and traders, but large institutions and sovereign.

This is why I believe that the possibility of a lower-trending US Dollar is potentially the biggest story for gold prices in 2019.

Important Dates Ahead:

- FOMC meetings: (all of which are now followed by a statement and Q&A, and as such need to be considered “live.”) January 29; March 20; May 1; June 19; July 31; September 18; October 30; December 11.

- February 17: deadline for Commerce Dept. to report on the impact of potential auto tariffs (after which the President will have 90 days to make a final decision on implementation.)

- March 1: the 90-day trade truce agreed to between the US and China officially expires.

- March 2: Federal debt ceiling reinstated.

- June 28-29: G20 summit

- August: Projected at the month the US government could potentially reach the federal debt ceiling if it has not been raised.

- August 24: G7 meeting

There are of course other facets to the market environment of course, and other things than can go beautifully right or shockingly wrong—depending entirely on your positions and point of view.

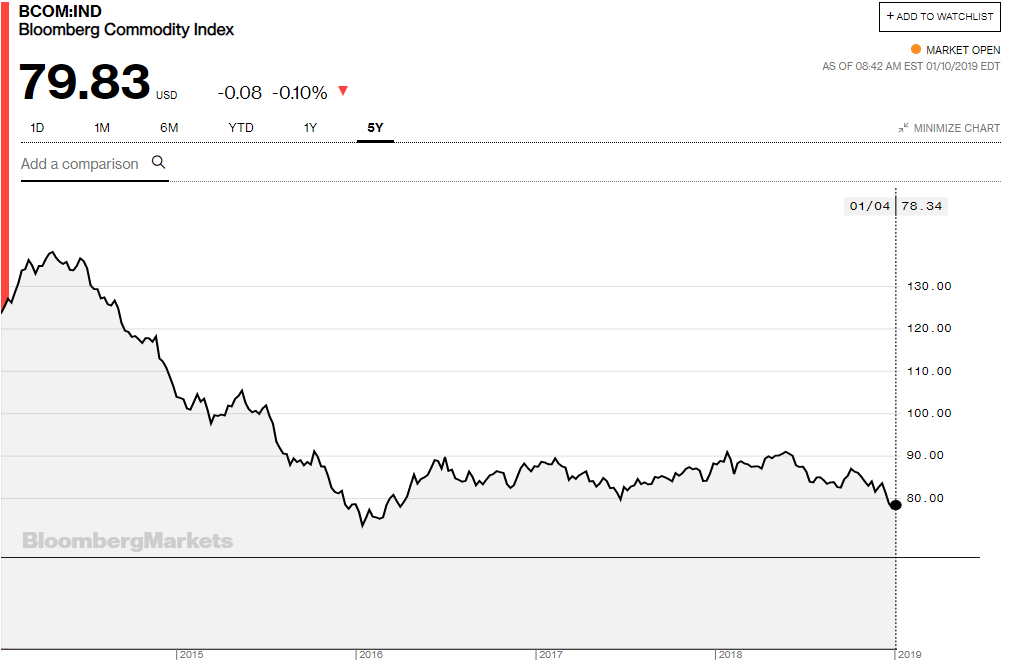

2.) Commodities Prices Rebound

There were a few spiky outliers (crude oil, natural gas, palladium) over the last 12 months, but 2018 was a year of fairly low volatility in most major commodities. The broad complex remained nailed to ground while the economic landscape around it began to shift.

While bargain basement commodity prices seemed to make sense from 2015-2017 as the global recovery was in impressive swing, as growth began to slow in developed markets many observers began pointing out that commodities like precious metals were still historically cheap as an asset given the macroeconomic environment. If a strong US Dollar was the last major impediment to commodities getting off of the floor, we did start to see the paradigm shifting in Q4 of 2018, as the Dollar sagged along with Treasury yields amid a concerns about the falling equity markets and volatility returned to many commodity classes like precious metals. Even crude oil, since the start of the year, has risen as much as 5% in a short amount of time to now trade above the $50 line of support that energy analysts predict will be crude’s pivot-point for 2019.

Other factors could influence overall commodity pricing and volatility this year. Goldman Sachs’ commodity team expects higher commodities prices 2019 as discretionary investors finally return to commodities, saying:

“Either discretionary money will come into the markets should US/Chinese policymakers create market confidence in the coming weeks or the physical market will ultimately discipline the paper markets sometime during 2019.”

On that note, we can’t ignore China when it comes to examining any group of commodities, as the second largest economy in the world swings its weight around in these assets unlike any other. Continuing weakness in the Chinese economy could noticeably change their investments in commodities like energy, agriculture, and especially gold.

The price-per-ounce of gold can rarely be markedly raised (or lowered) solely because the commodities asset complex is getting richer (or cheaper,) but an environment of sustained strength across the broad commodities space is highly supportive of lower bottoms as gold prices become more volatile.

Important Dates Ahead:

- Early March: The National People’s Congress in China will include the Chinese government’s economic targets and statement of intent for 2019.

- OPEC Meetings: late April; early December.

3.) The Stumble in Chinese Growth Becomes a Free Fall

As mentioned above (and in numerous other posts,) the state and trajectory of China’s economy is becoming a growing concern in global markets.

Keep your eyes on China. If they fall, they’re bringing the world down with them. They’ve been roughly 30% of global growth & 50% of investment in recent years.

Manufacturing has been waning all year, driven by trade sentiment & tightening. Data is getting worse despite easing.

— THE LONG VIEW ⚫️ (@HayekAndKeynes) January 9, 2019

The Chinese economy is so massive and linked to so many disparate asset classes and markets that it’s hard to pinpoint how any given currency or commodity would react to a version of China in free-fall, but the one thing that investors could count on—as this tweet (not subtly) points out—is fear. The flood of fear and risk-off sentiment that would flow into major assets if signs that China is at serious economic risk continue to mount would certainly be a buy-signal for safe-haven assets like gold and silver.

Important Dates Ahead:

- February 17: deadline for Commerce Dept. to report on the impact of potential auto tariffs (after which the President will have 90 days to make a final decision on implementation.)

- March 1: the 90-day trade truce agreed to between the US and China officially expires.

- Early March: The National People’s Congress in China will include the Chinese government’s economic targets and statement of intent for 2019.

4.) Crises Comes Back to Europe

In December of 2018, the European Central Bank called an end to its program of quantitative easing. While the fact of this decision is a positive indicator for the health of the shared Euro currency’s economy, nobody is quite sure what Draghi plans to do next. More importantly, with short term interest rates still near (or in some cases, below) 0% nobody is sure what the ECB would have left in its toolkit, or even if it would be effective, should another economic crisis visit the Continent.

And it’s not hard to imagine things trending that way in 2019. The budget impasse in Italy seems on its way to resolution, but unsteadily so. France, one half of the EU’s Franco-German core that rode to the rescue during the last credit crisis, seems to be spiraling towards chaos draped in luminescent yellow. Even Germany, the Chip to France’s Dale and for 20 years the bedrock of the EuroZone, looks like it’s in the early stages of its own troubles. ECB President Mario Draghi who has shepherded the recovery to this point steps down at the end of this year.

Oh, right. And we still genuinely have no idea how this whole Brexit thing is going to shake out, or how badly it might cripple both the EU and UK economies.

When it comes to predicting what gold will do if economic calamity returns to the EU, it seems a lot of the directionality would come down to timing. If the US Dollar is still riding strong, gold prices might weaken as the gap between the US economy and the rest of the developed world widens once again. Conversely, if the US (and/or China) is already in the throws of recession when Brussels stumbles, the flight to the relative safety of gold should speed up as investors struggle for other places to hide.

Important Dates Ahead:

- ECB Governing Council meetings: January 24; March 7; April 11; June 6; July 25; September 12; October 24; December 12.

- Bank of England MPC meetings: February 7; May 2; August 1; November 7.

- March 29: Brexit day.

- June 28-29: G20 summit

- August 24: G7 meeting

- October 24: ECB President Draghi’s final Governing Council Meeting

Caveat Emptor

Of course, macroeconomics like investing and much of the real world is decidedly non-binary. While giving you my view of what seems likely to happen, I’ve highlighted these four pivot-points specifically because they could go either way. Through some combination of luck, alchemy, or (hope of hopes) genuine effort and politicking for and by the American people, the US economy and its Dollar could remain the top dog and healthy throughout 2019 (gold would likely stay suppressed); commodities as a whole could remain a dull and lifeless asset class (gold flat-to-lower); China might turn this thing around and Europe could conceivably cruise through the year unphased. Or, maybe nothing changes at all—but when has that ever happened?

As always, traders: good luck out there.

Gold Price Chart

More articles from John Moncrief