Happy Friday, traders. Welcome to our weekly market wrap, where we take a look back at these last five trading days with a focus on the market news, economic data and headlines that had the most impact on gold prices—and may continue to into the future—as well as the charts for silver, the US Dollar and other key correlated assets.

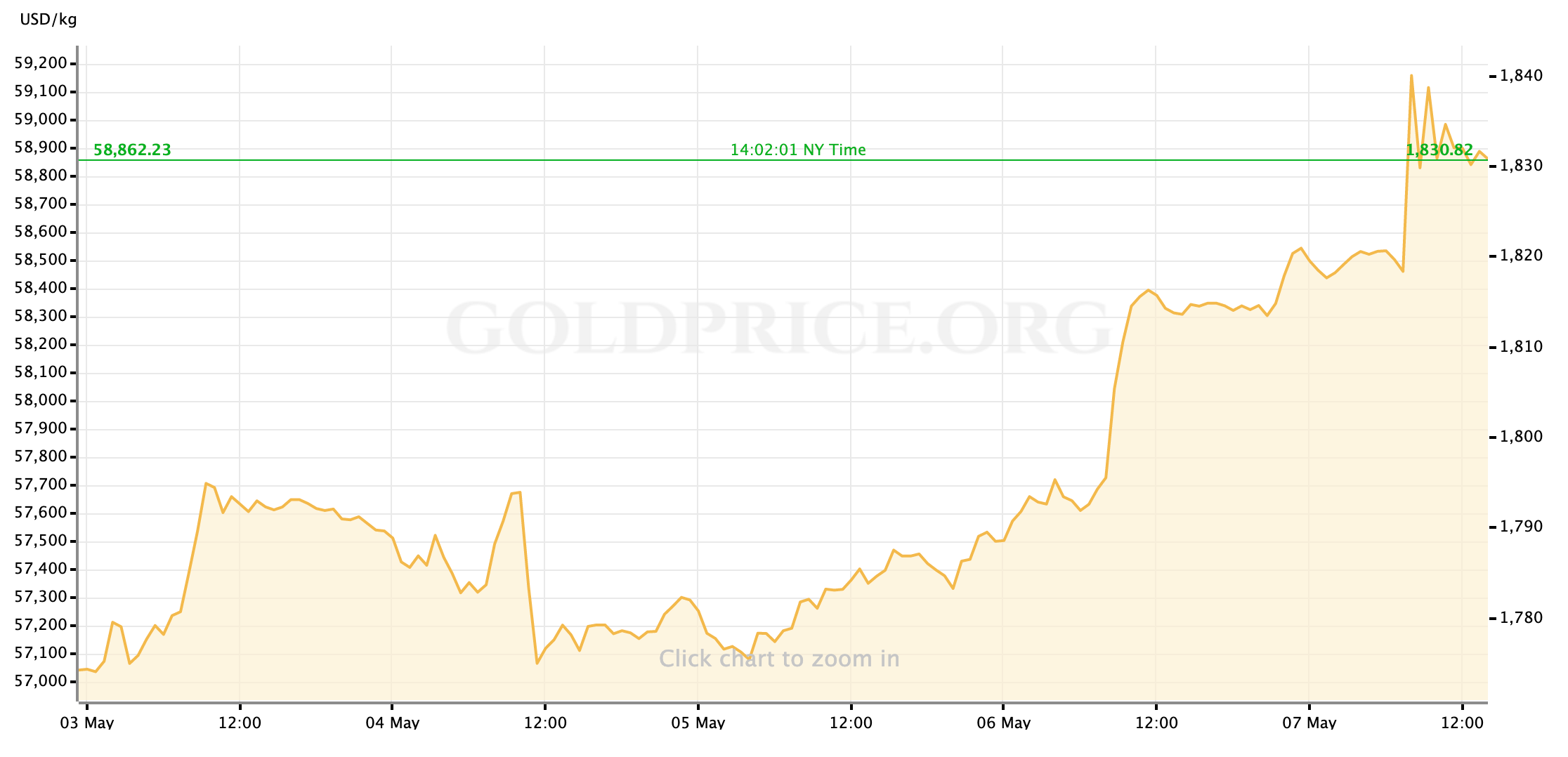

Gold prices are closing out the week at a massive premium to where they began Sunday evening’s trading.

The yellow metal was able to ride the reflation trade higher through most of the week alongside other key commodities, on a trajectory that, while choppy at times, ultimately drove spot prices well above $1800/oz and its 10-week highs. After consolidating strength above $1815 in the back half of the week, gold’s strongest tailwind kicked in on Friday morning as financial markets grappled with a deeply disappointing set of US economic data.

So, what kind of week has it been?

It seemed like our usual market wrap would be reviewing a pretty uneventful week in terms of market news and macro data, until this morning when April’s Jobs Report was a historic disappointment relative to investor and analyst expectations; The reported Non-Farm Payrolls number was the biggest downside miss on record.

- Analysts’ consensus projection for the number of jobs added to the US economy in April was for a massive 950K or higher, although several desks said they expected a number north of 1 Million.

- In reality, the BLS’ tally counted only 266,000 new hires last month. In another blow to recent recovery confidence, March’s NFP number was revised lower by nearly 150K.

- The headline unemployment rate also unexpected rose to 6.1%.

MASSIVE miss for April payrolls, +266k vs. +1M est. … notably, last month revised down to +770k vs. +916k initially pic.twitter.com/zXLOvbAMyi

— Liz Ann Sonders (@LizAnnSonders) May 7, 2021

While economists and investors parse the subsets and details of Friday’s labor market report, there is conjecture but (so far) little consensus on how participants got the projections so wrong and what this means for the US economic recovery going forward.

- Some are pointing to issues that the NFP data set has always had accounting for “seasonality,” while others lay some of the blame for the overly optimistic projections inaccurate categorization of hiring as the US economy re-opens post-pandemic.

- As the New York Times’ Jeanna Smialek put it, it’s as if “this jobs report was tailor-made to give everybody a talking point.” Expect a lot of “debate” in the week ahead over whether Friday’s disappointing data is proof that the extraordinary fiscal stimulus of the last year must be left in place for longer in order to tip the US economy fully into recovery; Or else it is proof that social provisions like enhanced unemployment insurance are dampening the labor market.

One thing, at least, is very clear from the evidence of this morning’s Jobs Report: The Fed’s super accommodative monetary policy isn’t going anywhere.

- Inflation hawks and other market actors have, at various times since the start of the year, tried to put pressure on the Fed (mostly through selling in the Treasuries market) to accelerate their schedule for tapering bond purchases and eventually raising interest rates—Actions that the Fed, as of March’s staff projections, doesn’t expect to take before the end of 2022.

- For those who wanted to see the Fed tightening sooner (or, at least, believed that the Fed should,) the reasoning was that inflation projections were moving higher has the US economy exited the pandemic restrictions of the least year. Paired with the very strong labor market data that’s been recorded since February, concerned and/or motivated investors argued that FOMC’s insistence on waiting to actually see evidence that the US economy was meeting the Fed’s mandated targets—namely: price inflation consistently at or above 2%, and “full employment”— before taking action to tighten financial conditions would allow inflation to overheat and curtail economic growth, choking off a nascent recovery.

- In the past, the Fed was more willing to move at the point that it projected higher inflation and a labor market approaching full employment. Fed Chair Jerome Powell and the current FOMC not largely seem to acknowledge this is a key mistake over the last decade.

- As a body, the Fed has never looked like wavering from their position, even when March’s bond markets got very volatile and Treasury yields reached past 12-month highs. In defending the rightness of their stance, Powell and others often highlighted their view that, even if recent pops in inflation proved not to be transitory as expected, the US labor market was still far from reaching its pre-pandemic strength. Friday’s brutally disappointing NFP numbers have cemented that reality. Doubters will have to accept that the Fed will keep its foot on the gas pedal, and interest rates near zero, for quite a while yet.

Well put from @neelkashkari https://t.co/1HRtxZEtz7 via @AnsteyAsia pic.twitter.com/afd1K8VxZR

— Joe Weisenthal (@TheStalwart) May 7, 2021

It’s an outlook that explains why, despite objectively bad news for the US economy and the pace of its post-pandemic recovery, the re-opening/reflation trade that has animated markets since the end of Q1 is continuing forward at the end of the week, lifting US equities higher as well as gold prices.

- US stocks—particularly those in the tech sector which would be the first to feel the squeeze of a hike in the Fed’s short-term interest rates—are being boosted by what’s essentially an additional guarantee that the FOMC’s policy will remain “aggressively low for longer.”

- Gold, meanwhile, continues to participate in the reflation trade (which is helping to consolidate the yellow metal’s support well above $1800/oz,) but is also likely getting a short-term boost on Friday by some measure of risk-off positioning after the labor data debacle.

- Gold prices are also getting a boost as a counter to US Treasury yields falling in reaction to Friday’s news—the inverse correlation between yields and gold prices has remained consistent this week, with the yellow metal’s acceleration to-and-through the major level of $1800 corresponding to one of the week’s bond-market rallies.

5-year yields are crashing.

Still much higher than the beginning of the year, obviously, but a sign that traders are coming around to the idea that the Fed isn't going to be in a rush to hike. pic.twitter.com/rwdqsat87O

— Brian Chappatta (@BChappatta) May 7, 2021

While the positive-trending reflation trade remains the dominant driver in US financial markets despite the poor macroeconomic data, the “exuberance” of recent weeks has been dimmed by concerns over how much longer the American economy has left to go before a full recovery.

- Without suggesting any sharp rallies away from $1800/oz are on the horizon, this could continue to be a broadly positive environment for gold as is further forestalls any possible point where the excitement and demand of risk-on equities pulls all investor attention away from gold.

Looking ahead to next week, we’ve got some fresh inflation data and doubtless some relevant reactions from FOMC officials to the April Jobs Report.

- Wednesday’s CPI data will have lost some of its luster and it seems pretty hard to argue that even the expected spike above 2% in the core CPI number will spur the Fed into earlier action; But it nonetheless helps us model the pace of recovery through the second and third quarters of 2021.

- At the end of the week we’ll see April’s Retail Sales data. Retail has been a bright spot since the last fiscal stimulus package rolled out and vaccinations picked up the pace; I’ll be watching to see if it too made a disappointing turn for the worse in April (though I find that less likely than the labor market dramatics.)

- And, of course, we’ll want to see how the most influential FOMC participants are reacting to Friday’s labor market stumble.

For now, traders, I hope you can get out and safely enjoy your weekend for the next couple of days. After that, I’ll see everyone back here on Monday for our preview of the week ahead.

Gold Price Chart

More articles from John Moncrief