Happy Friday, traders. Welcome to our weekly market wrap, where we look back at these last five trading days with a focus on the market news, economic data and headlines that had the most impact on gold prices—and may continue to into the future—as well as the charts for silver, the US Dollar and other key correlated assets.

Despite a sudden turn in market sentiment late Thursday night that pared much of the yellow metal’s gains for the week, gold prices on Friday morning are trading at a strong premium to Monday’s session as the precious metal attempts to consolidate some strength in a higher-rate environment and join in on the reflation trade.

So, what kind of week has it been?

Gold Started the Week Off on the Back Foot Again; Meanwhile, Equity Investors Rotate Away from Tech Giants

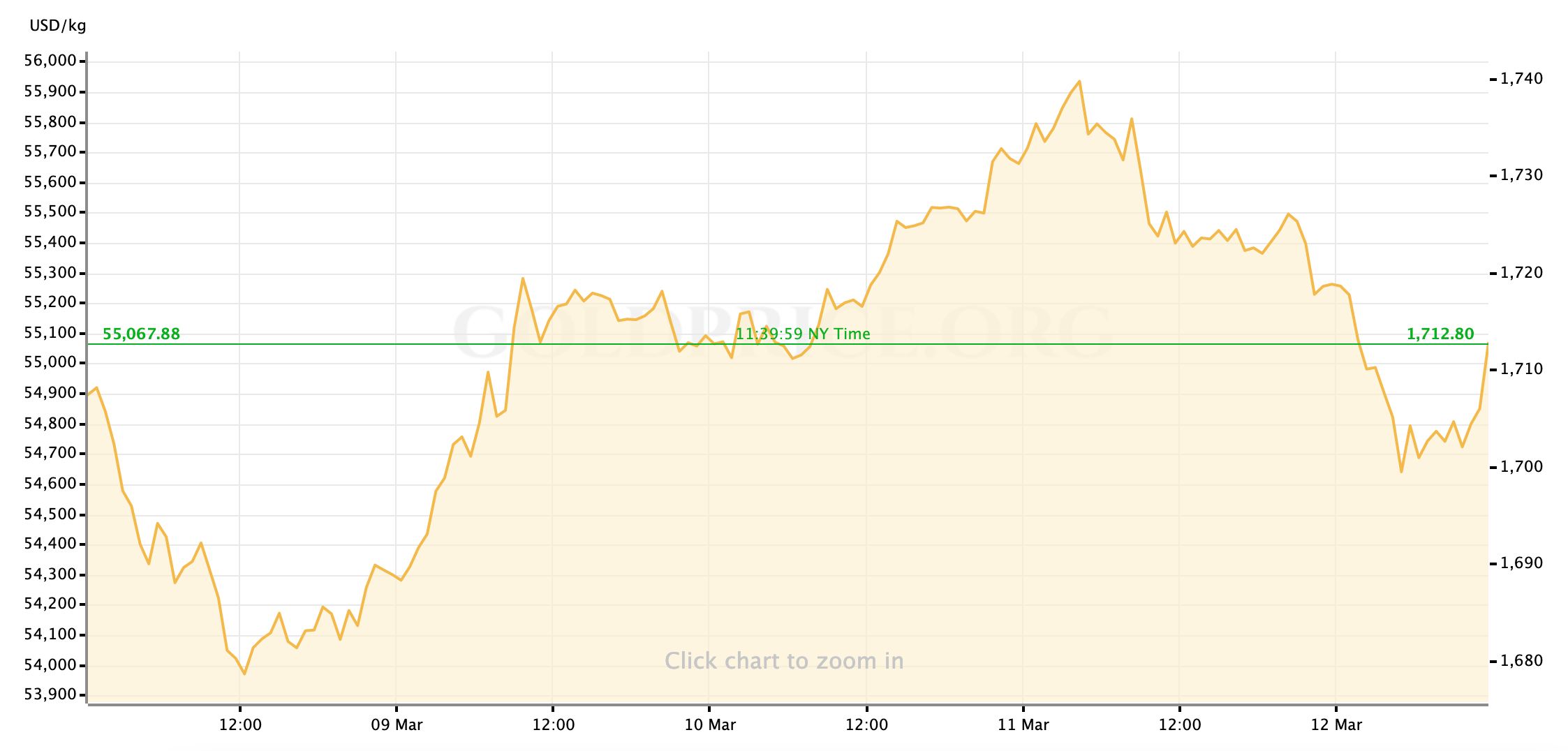

Last week’s trading patterns, specifically in metals and rates markets as the two continue(d) to be closely correlated, cast a long shadow over the first two sessions of this week as the charts’ shapes looked similar to the Monday and Tuesday gone which would feed into a steep collapse of gold spot prices while US Treasury yields ripped higher. Upward momentum that had returned to metals prices on Sunday evening (and even allowed the yellow metal to trade through and well above $1700/oz) was snuffed out in the earliest hours of Monday morning as another rush of selling in sovereign bond markets pushed the yield of the benchmark US 10-year Treasury note as high as 1.6% once again. As we’ve seen several times over the last few weeks, the flight from Sovereign debt correlated to similar rotations away from gold positions as the US Dollar continued last week’s rally. Gold spent the morning hours before and after cash trading began for the US session sliding as far as 10-month lows, before finally finding supportive buyers around the $1680/oz level. The velocity of the move in rates markets slowed during the Monday’s New York session, but didn’t reverse; Metals prices spent the better part of the day under pressure and nailed to the lows.

In stocks, the mega-cap tech darlings of the last year potentially had as rough a day as precious metals did. With Tesla’s drop seeming to grab the majority of headline attention, the tech-heavy NASDAQ 100 slid far enough to notch another technical correction in the session; The pervasive plunge in the tech sector added serious drag to the S&P 500 as well. Looking one level deeper, Monday’s equity action began drawing attention to a move that would become more prominent as the week went on and could be an important factor in the weeks ahead: Although the faltering tech giants made of a bad day for the S&P and NASDAQ, the more “traditional” sectors like financials and fossil fuel energy performed well on the day and lifted the stalwart Dow into the green. Equity traders had clearly come to favor the staples that would fare well in an inflationary cycle, in place of possibly-overextended growth stocks: To be sure, those same financials and commodity producers spared the S&P from an uglier day more akin to the NASDAQ’s plummet.

As the Bond Markets Calmed, Precious Metals Rode Tailwinds Higher

Again mirroring the same day from last week, Tuesday’s metals markets were characterized by strong gains in the precious metals’ spot charts. Bond markets rallied Monday night (the US 10-year’s yield fell to 1.52%) providing a strong and steady tailwind to metals’ prices. Gold and silver traded consistently higher through the Asian and European trading hours and although the momentum waned as the US session picked up the baton (and the rebound in Treasury bonds eased as well,) the yellow metal spend most of Tuesday’s New York session priced close to the highs at $1718/oz while silver looked likely to retake $26/oz and higher.

Towards the end of the US trading day, despite the strength and consolidation that gold had shown, traders would have been right to be skeptical about the chances for a more sustained rally. After all, the prior week had allowed gold a respite from selling pressures on Tuesday before pummeling the yellow metal lower for the rest of the week. This time, while rates once again moved higher Tuesday night they did so with much less volatility; Gold and silver prices weakened slightly from the afternoon’s closing prices but it became clear there wouldn’t be a major collapse lower. The charts for both gold and US Treasury rates traded calmly through the overnight sessions, and by the time markets read Wednesday’s updated CPI numbers gold had consolidated its position above $1710 and silver also appeared well supported.

Tuesday’s stock market trading saw its own reversals from Monday’s losses. To be sure, investors with slightly higher risk appetites were probably already eying new positions in in a slew of suddenly “cheaper” tech giants like Tesla and Zoom heading into Tuesday’s business. The Monday night/Tuesday morning rally in bonds and drop in the Treasury rates which seemed to have generated most of the concern about over-priced valuations may as well have forced their hands in the matter: The S&P 500 rallied nearly 1.5% on Tuesday while the battered NASDAQ made its biggest jump in four months. In another notable reversal from Monday, the US Dollar rally appeared to stall out well before Wednesday’s inflation data hit the wires. This weakening in the Greenback certainly contributed an extra boost to the stock market’s momentum and to gold’s, as it would continue to through the remainder of the week.

Soft Inflation Data Pushed the Dollar and UST Yields Lower, Gold Gains More Ground

When those updated CPI numbers did hit, they became the pivot-point in markets for Wednesday and, likely, the week. According to the report, overall consumer prices rose at the expected (annualized) rate of 1.7% in the month of February. The pickup in the headline number was mostly due to climbing energy price. The pace of underlying “core” inflation, however, came in slightly below projections at 1.3%. This slight decline isn’t terribly surprising given the US—the globe—is still digging itself out of a deep economic crisis, and it’s certainly not the first time in recent weeks that we’ve seen macroeconomic data that undercut the investors’ apparent fears of runaway inflation hiding right around the corner. But this report did seem to cool that recent fervor: in response the data’s release, the US Dollar dropped further and investors stepped quickly back into US Treasuries. The 10-year yield dropped roughly 20 bps and gold prices jumped. Although the yellow metal’s chart initially pulled back from the initial jump, in the first hours of the US session gold prices consolidated around $1720/oz.

As the day went on, markets and investors both seemed to enjoy the greater sense of calm now that bond markets had relaxed somewhat. The bond market rebound continued later in the morning, and gold continued to climb with silver alongside. By mid-afternoon, when the American Relief Plan—the White House-sponsored COVID-19 relief bill—officially passed a House vote on its way to President Biden’s desk, benchmark yields had slipped back to 1.51% while gold spot prices were strong and stable above $1725/oz; Silver, meanwhile, gained support above $26. Both metals held their gains through the end of Wednesday’s session, closing slightly higher.

Equities traders also enjoyed a lift from a weakening Dollar and easing inflation fears, and the dynamics in action following the softer-than-expected inflation data underlined the shift we discussed above (regarding Monday’s markets): Though the tech/growth-laden NASDAQ slipped lower on the day, the S&P 500 rose on the back of energy and bank stocks which also carried the Dow above 32,000 points for the first time. It seems clear to me that the “reflation trade” isn’t going away, as there remain many reasons to expect an uptick in inflation over the medium- to long-term; it’s just becoming less panicky and more tactical. This could provide gold and silver, should they find a long enough stretch of stability to build from, an opportunity to participate in the reflation cycle which historically lifts raw commodities higher as growth fuels demand for materials.

On Stimulus Act Signing Day, Equity Investors Cheered; Gold Gave Back Strong Overnight Gains but Appeared to Consolidate Well Above $1700

On Wednesday evening, as global trading re-opened to begin Thursday’s book of business, overseas investors and managers got their opportunity to reposition after the concern about imminent hyper-inflation had been “reevaluated” following the new CPI data. Overseas traders, particularly in Europe, took the cue to step aggressively back into the bond markets, over-buying enough to drive US Treasury yields sharply lower and even pull the 10-year yield below 1.5% for the first time all week. Gold prices responded, as we’ve come to expect, by moving with roughly the pace in the opposite direction (of yields.) The yellow metal traded steadily higher to-and-through the start of the European trading day, eventually reaching a peak just shy of $1740/oz, while silver was priced well above $26.40.

As trading moved closer to the US business day, the chart had to come back to Earth: Whether the correction was a reaction to gold’s spot prices moving to high, or (as I think more likely) benchmark yields briefly below 1.5%, or a combination of the two, the rebound in Treasury yields created a steady headwind for gold and prices began a steady roll down from the peak. When markets got into the start of New York trading hours, there was a brief reversal of gold’s slide as global bond traders reacted positively to the ECB’s announcement of an increase to the size of their asset (bond) purchases in a move that slowed the rebound in rates; 1.5% proved the line of support for bond-seller though, and the gravity on gold was just too strong and the downward trend eventually continued.

The start of cash trading in US stocks eventually provided the support zone for gold prices. Further encouraged by a slightly better Initial Jobless Claims number, the mood around equity trading in larger parts of the US market was all sweetness and light on Thursday thanks to plans for President Biden to sign the new coronavirus relief package into action later in the day, allowing some facets of the plan to possibly take effect as soon as this weekend. Ahead of (and certain after) the official signing, all benchmark indices for US stocks moved higher, led by a pickup of more than 2.5% in the NASDAQ 100. For gold prices, the celebratory surge in risk appetite came with a double-edge: investors’ big step into equities was enough to blunt the rise in Treasury rates, but also enough to diminish interest in safe-havens across the board. So, while gold found plenty of buyers to offer support a few steps above $1720/oz it lacked the attention needed for a rally. Precious metals and Treasuries alike traded mostly flat through the lengths of the US session.

A Suddenly Bearish Barrage of Bond-Selling is Up-Ending the Week as Gold Retreats to Support

From the perspective of a US-based trading seat, questions around the size and speed of a rise in inflation driven by the new $1.9 trillion stimulus bill appeared to be settled, at least for the week: Wednesday’s mild CPI data seemed to support the projection of the Fed and other participants that the US economy still has a long way to go before growth heats up enough to spur over-inflation; And neither the passage of the revised relief package through Congress nor its being signed into law spurred any immediate jolts in the bond market. It felt almost entirely disconnected from the reality of the previous four days, then, when the early hours of European trading (around midnight in the US) brought a sudden return of volatility and massive selling pressure to the bond markets. Yields on the US 10-year note ripped to-and-through 1.6% with little resistance; Gold prices, inversely correlated, collapsed overnight before finding support at $1700/oz. Silver shed much of its gains as well before finding buyers around $25.45.

Lacking any other reasonable explanation for the sudden bearish swing in rates that has pushed the 10-year yield its higher level in a year, analysts and observers are falling back on the assumption that it’s a delayed response to historic level of spending that the US government just formally agreed to. That’s difficult to square with the updated view of inflation that drove market sentiment for much for the week—the rosy outlook for recovery and growth for the US economy in year of fiscal spending and mass-vaccination hasn’t changed in the last 48 hours— but I suppose it may just be another nail in the coffin for arguments that markets are “rational.”

As the US trading session of the week settles into its paces on Friday, we’re seeing the expected effects of the surge in Treasury yields. The sharpest part of the move came during European trading hours when liquidity is considerably lower; So, the pace has slowed, but with rates looking sustainable above 1.6% for the first time in a year there is still a steady flow of selling by US-based investors and managers. The tech-heavy NASDAQ is down more that 1% at the time of writing, while the more “traditional” stocks that comprise the DJIA are showing green. (The S&P 500, which takes both sides, is down for the day so far but not so much as the NASDAQ.) The combination of strong psychological support at the $1700/oz level and an easing in the pace and pressure of selling in the bond market is, so far, allowing gold prices some extra room to recovery. At the time of writing (mid-morning on Friday,) gold spot prices have made a steady, consolidated rally above $1710; Silver prices have climbed back above $25.60 as well.

Given the tight (inverse) correlation between the two assets, I suspect the most closely-watched levels for precious metals trader heading into the weekend will be gold’s support at $1700/oz and the 10-year Treasury’s yield at 1.6%. If both hold course, we could finally see an opportunity for gold prices—given a decent platform and pause to consolidate, finally—to get in on the reflation rally that looks to benefit much of the commodities sector.

Next Up

With a relatively light docket in terms of macroeconomic data, our main focus next week will be Wednesday’s FOMC meeting and the press conference to follow. While Jerome Powell & Co. are not expected to make any serious changes to policy or stated forward guidance, we will see a new round of economic projections that will incorporate the massive push of fiscal stimulus that’s been signed into law this week to support and accelerate the US economic recovery.

For now, traders, I hope you can get out and safely enjoy your weekend for the next couple of days. After that, I’ll see everyone back here on Monday for our preview of the week ahead.

Gold Price Chart

More articles from John Moncrief