Happy Friday, traders. Welcome to our weekly market wrap, where we take a look back at these last five trading days with a focus on the market news, economic data and headlines that had the most impact on gold prices—and may continue to into the future—as well as the charts for silver, the US Dollar and other key correlated assets.

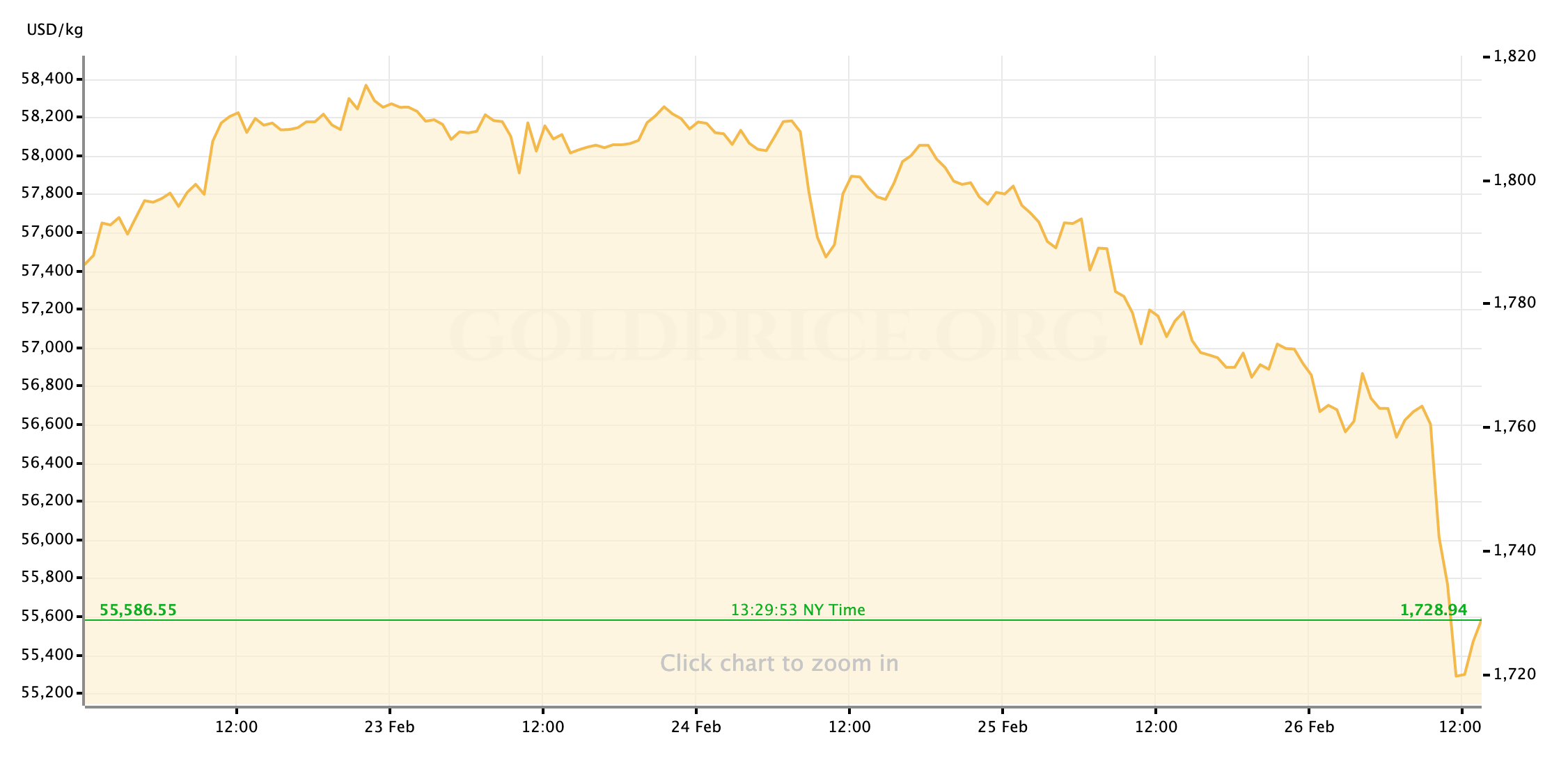

Gold prices are ending the week sharply lower than Monday’s opening marks. Despite appearing to benefit at the start of the week from the reflation trade that is commandeering financial markets, the precious metals have failed to hold any consistent support in the face of aggressive liquidating of US Treasury debt that is weighing on any asset primarily traded as a safe-haven against risk.

So, what kind of week has it been?

Gold Prices Have Spent the Week at the Mercy of a Rout in Government Bonds

The market prices for precious metals this week have been commandeered by a single market force—the market-wide sell-off in “riskless” government debt—that our usual chronological look at the week’s economic data points is rendered mostly moot. Gold prices at this point in the cycle are clearly subordinate to their traditional inverse correlation to Treasury yields, and this week those yields have been on an absolute tear. The surge in bond yields—which results from massive net-selling of government debt, and which we’ll track by discussing the benchmark yield on the US Treasury’s 10-year notes—has been generated at its core by the reflation trade that is dominating financial markets. As a reminder, “reflation trade” is just a catch-all phrase for the market prioritizing assets that are usually projected to perform well as US price inflation accelerates, as many are now assuming it will in the medium-term, and shifting away from those that are not. There have been other factors that have either encouraged or muted the moves in Treasury yields this week (USD pressure, technical plays, rebalancing,) but inflation expectations appear to be at the heart of it.

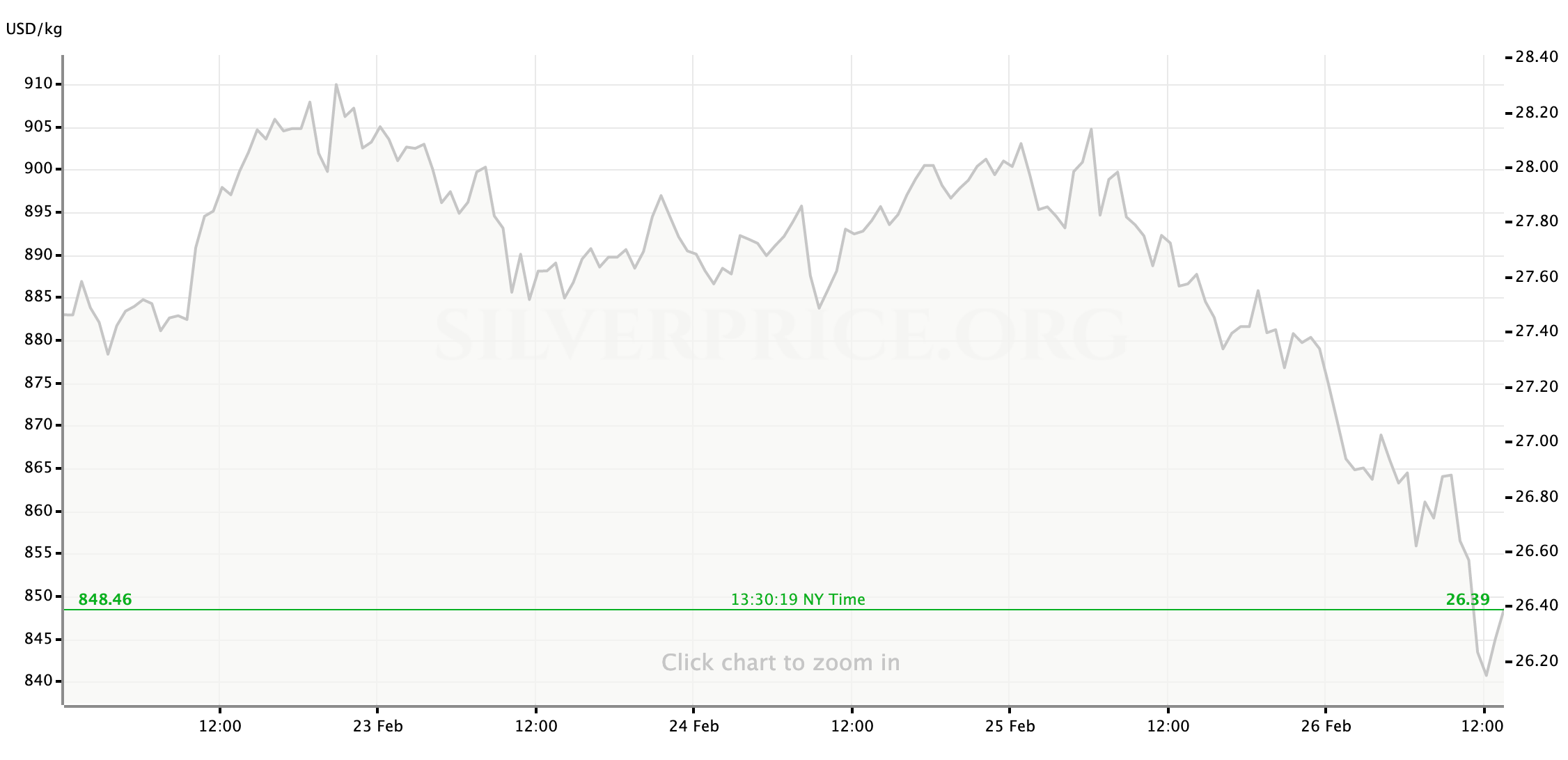

For gold traders, regardless of the specific motivations for each step along the way it’s been clear that every push higher in yields, particularly the strongest ones that have marked the start of each US trading day, has also exerted tremendous pressure on the gold market, often pushing the yellow metal’s spot prices below a significant level of previous support. The deepest drops for precious metals have come towards the end of the week as yields on the US 10-year reached new yearly highs and surpassed 1.5%: The initial move above the line on Wednesday night into Thursday morning saw any support for gold at $1800/oz wiped out; Friday morning’s sharp return to 1.5% coincided with gold’s steepest fall of the week so that the yellow metal is currently searching for buyers as low as $1720/oz. Silver has been dragged to the depths as well. Having traded above $28/oz as recently as midweek, the white metal’s spot price is ending the week with hopes to hold onto $26.25 as support.

The strong moves in yields have impacted other key asset classes as well. US equities have been under notable pressure all week and indeed only avoided a few days of major losses midweek thanks to two days of Congressional testimony from Fed Chairman Jerome Powell. In his remarks and responses, Powell characterized the recent surge in yields and interest rates (probably correctly) as a confirmation of investor optimism regarding the US economy’s projected recovery this year. The Chairman also reaffirmed the FOMC’s commitment and will to hold rates ultra-low and monetary policy ultra-loose until the committee measures inflation consistently above the 2% target and “full employment” in the labor market.

Other Correlated Markets Have Helped or Hindered Precious Metals’ Value at Times

Just as other factors have buffered or buffeted the pace of the reflation-focused moves in bond markets this, so has gold’s fate for the week been impacted in smaller ways by other correlated assets. Primary of these runners-up have been an overall rise in the raw commodities complex, and the movement of the US Dollar. The extreme sensitivity to interest rates on display to end the week was much more muted through mid-day on Wednesday in part because of weakness in the Greenback that kept some investors happy to hold gold positions. The Dollar has rallied since Thursday, and the extra weight that has anchored to gold prices is evident in the velocity of each move lower.

If Gold Can Find Price Support, There May be Upside Coming

It’s not all going to be perpetual gloom for gold traders in a race to $0, of course; Even if the line of support near $1720/oz fails on Friday. The “reflation trade,” after all, isn’t contained only to the bond markets: While it’s unattractive to hold riskless Treasury bonds right now in anticipation of rising inflation as a result of an aggressive economic recovery, the same projections have been driving a lot of investors’ money into the raw commodities this week as evidenced by crude oil’s strong performance.

The early week surge in oil prices and other commodities almost certainly helped to keep gold prices afloat at the beginning of the week before the yellow metal’s chart was overpowered by the aggressive rout in bonds. So, while the new paradigm for markets has seemed only negative for gold this week, if investors are still girding for accelerated inflation within the next two years—which, to be clear, would have to reach levels we haven’t seen in well over a decade—once the markets have found a lower bound for gold prices, gold will likely be able to participate rising tide lifting all commodities. What is currently a healthy lift for raw commodities, if it persists, may in fact carry over into what some analysts, including the Goldman Sachs commodities desk, are predicting to be the start of a new “commodities super-cycle” in 2021.

Next Up

As we move closer—in theory—to a major increase in fiscal spending on the Biden Administration’s COVID-19 relief bill (which may go to a vote in the House as early as Friday afternoon,) we can expect the market narrative to continue to be driven by inflation projections. Accordingly, that will be the main story we’ll check in on coming out of the weekend. At the tail end of the week, we’ll get February’s Jobs Report which, despite an unexpected fall below 800K in initial jobless claims this week, is probably going to show that we are a concerning distance away from the labor market recovery that the Fed is working towards.

For now, traders, I hope you can get out and safely enjoy your weekend for the next couple of days. After that, I’ll see everyone back here on Monday for our preview of the week ahead.

Gold Price Chart

More articles from John Moncrief