Happy Friday the 13th, traders. Welcome back to our weekly recap of the data and headlines with the biggest impact on the gold and Dollar markets, both this week and as we move ahead. Gold prices are higher following a milestone week that included the final FOMC meeting of 2019 and the announcement of an initial trade agreement between the US and China.

Regular readers will know that I typically recap the market week chronologically, but since the most important news of the week has only happened in the last 24 hours or so, let’s start with the latest trade news. Then we’ll touch on the Fed’s week, and briefly look at other notable news for the week before sending you on your way for the weekend.

So, what kind of week has it been?

US and China Agree That They Have Come to an Agreement-- But Gold Prices Continue to Rise

At the start of the week, a new round of punitive tariffs on Chinese goods was still scheduled to go into effect on December 15. So, we knew that some kind of trade headlines would be driving gold prices: either the two sides would reach an agreement on an initial deal and cool the tensions a bit heading into year-end, or else Washington would move forward with its threats and tie another anchor to global trade growth.

As it turns out, a “phase one” agreement has been made, although Its announcement feels more like a comma than a full-stop. After all, despite a steady march of ostensibly positive trade narrative—first Trump Tweets, then reports, and this morning’s confirmation from both sides—gold prices are higher for the week as a safe haven asset while equities seem to be on rockier terrain. What gives? I don’t think there’s any great mystery, it just requires a closer look.

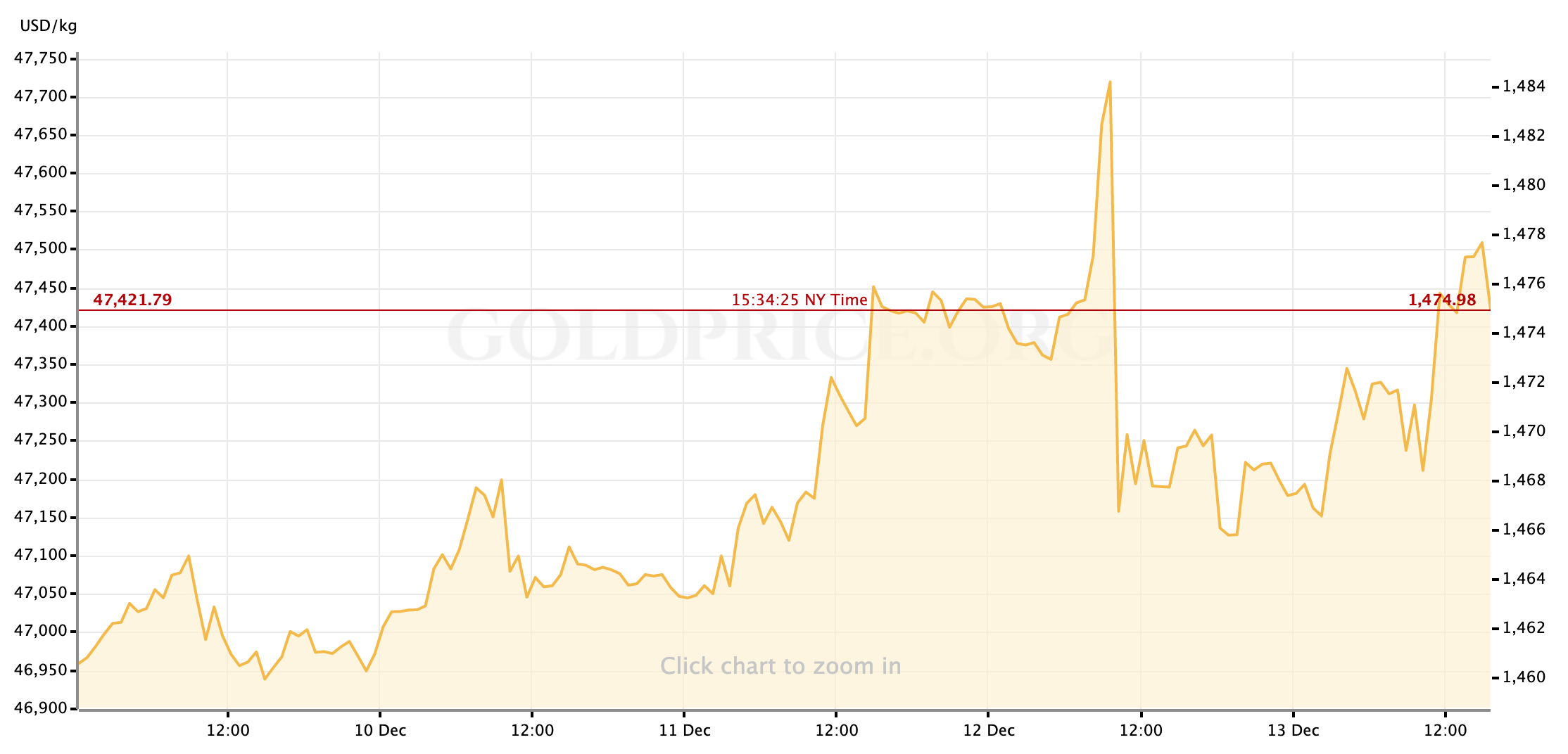

If we go back to the start of US trading on Thursday, risk markets seemed to be feeling considerably more pessimistic. With Donald Trump expected to issue some kind of announcement or decision with regards to the planned tariffs after meeting with his trade negotiators, the mood was tense and traders preparing for a negative outcome had the Dollar shifting lower while gold prices moved to $1485/oz—a 5-week high—just before the market open.

Market sentiment shifted dramatically as cash trading opened, as POTUS tweeted about the desire on “both sides” to come to an agreement and avoid further escalation. For my money (so to speak,) it was a tremendously flimsy premise from which to assume that a deal would be done but risk markets ran with it: equities surged higher and gold prices collapsed back to the area of $1465/oz. Despite the strength of the initial risk-on reaction, these fluctuations and reversals rippled through markets throughout the course of the day’s trading. In fact, when more concrete headlines broke in the early afternoon that a deal had be agreed to and would await Donald Trump’s approval, there was a strong sell-signal that attempted to push gold spot prices below $1465/oz but the yellow metal bounced right back and instead returned to strength at $1470/oz. The pattern repeated itself, albeit at a slower clip, Thursday evening: gold prices gapped lower at the global market re-open (during the brief close, the White House affirmed that POTUS would sign the negotiated agreement,) but was once again trading $1470 as Asian markets spun-up for Friday.

I think the lack of a massive sigh of relief and surge of risk appetite in major assets is due to two factors: the incremental nature of tariff avoidance/relief as part of the agreement, and well-earned distrust of Washington’s commitment to a tentative trade peace. While both sides have lots of hopeful words to say about getting an initial agreement done, in terms of the tariffs that have been dragging on the global economy for 18 months all we can (maybe) count on is a cancellation of those planned for December 15 and a roadmap for removing charges that are already in place. This is not a cooling of the trade war between the world’s two largest economies. It’s a step forward, but only a handshake deal to prevent further escalation and I think risk markets are right to be skeptical of whether or not POTUS’ satisfaction with the state of trade will remain, or if the new year will bring new threats. From that point of view, it seems reasonable for traditional safe havens like gold to continue experiencing the buying that we see in gold to close out the week.

The Fed Sets the Table for 2020, and the Walks Away from It

The other major story from this week was of course the final FOMC meeting of 2019, and the first to follow three consecutive rate cuts aimed and supporting economic expansion that seemed under threat. I’ll link to our more in-depth recap here.

The primary take-away from the December statement and additional comments from Chairman Powell during his press conference is that the committee feels comfortable leaving policy rates where they are for the time being, and that the bar for a return to rate hikes is set very high. This is important to gold markets in the medium-term for two reasons:

- As we move into 2020, until we see a considerable and persistent rise in inflation pressures we can count on interest rates remaining low (relatively) which is a supportive environment for gold as a zero-yielding asset. We saw clear proof of this as Chairman Powell talked gold prices to weekly highs.

- Powell & Co. are effectively sending a signal to the White House (and the rest of us) that they will not be stepping in over the next year to nullify any negative effects of the trade war with China, should POTUS and his counselors choose to continue with it. This means that new developments in trade with China—positive or negative—should be felt even more strongly in gold and Dollar markets between now and (at least) the 2020 elections.

The Rest of the Week

There were other important headlines and data points this week of course, which lacked immediate impact on the gold market, but do set the stage for further developments as we move into next year.

- CPI inflation for November was reported on Wednesday and matched well with expectations. On Thursday, the Producer Price variant was a slight miss, matching recent shakiness in other indicators for the US manufacturing sector. The Fed acknowledged the weakness in Wednesday, saying that they are confident that the health (and spending) of the American consumer will continue boosting the services sector enough to promote expansion.

- But will it?

All but lost in the global news tornado this morning: dismal US retail sales for November. Up just 0.2%, control group up just 0.1%. Clothing stores -0.6%, Department stores -0.6%; Toys (& sporting goods, books) -0.5%. Non-store (on line) +0.8%.

1/2

— Michael McKee (@mckonomy) December 13, 2019

Trade is clearly the dominant headline today, but as soon as next week economists and investors will have to deal with a disappointing Retail Sales report for the important month of November. The bar for a Fed hike is high, but we also need to be on the lookout for the data deterioration that might force more easing.

- UK Conservatives and their leader Boris Johnson won a solid parliamentary majority in Thursday’s general elections, theoretically clearing the road for the UK to finally leave the European Union (for now, on January 31.) Meanwhile in Washington, the full House of Representatives will vote on articles of impeachment next week.

Next Up

Looking ahead, to next week, things slow down considerably on the data docket between now and 2020. Our primary focus will be on tracking the final steps of formalizing the initial trade deal between the US and China, and the market will be looking for confirmation of the Fed’s outlook when the November numbers for PCE inflation are reported along with Personal Spending on Friday.

Until then, enjoy your weekend traders. I’ll see you all back here on Monday for our preview of the last full week of trading before New Year’s.

Gold Price Chart

More articles from John Moncrief