Happy Friday, traders. Welcome to our weekly market wrap, where we take a look back at these last five trading days with a focus on the market news, economic data and headlines that had the most impact on gold prices—and may continue to into the future—as well as the charts for silver, the US Dollar and other key correlated assets.

Gold prices are looking calm and stable, as they have more most of this week. In part, this is a result of generally calm markets over these five trading days. At the same time, it’s certainly due in some part to investors sitting on their hands ahead of the Fed next week.

So, what kind of week has it been?

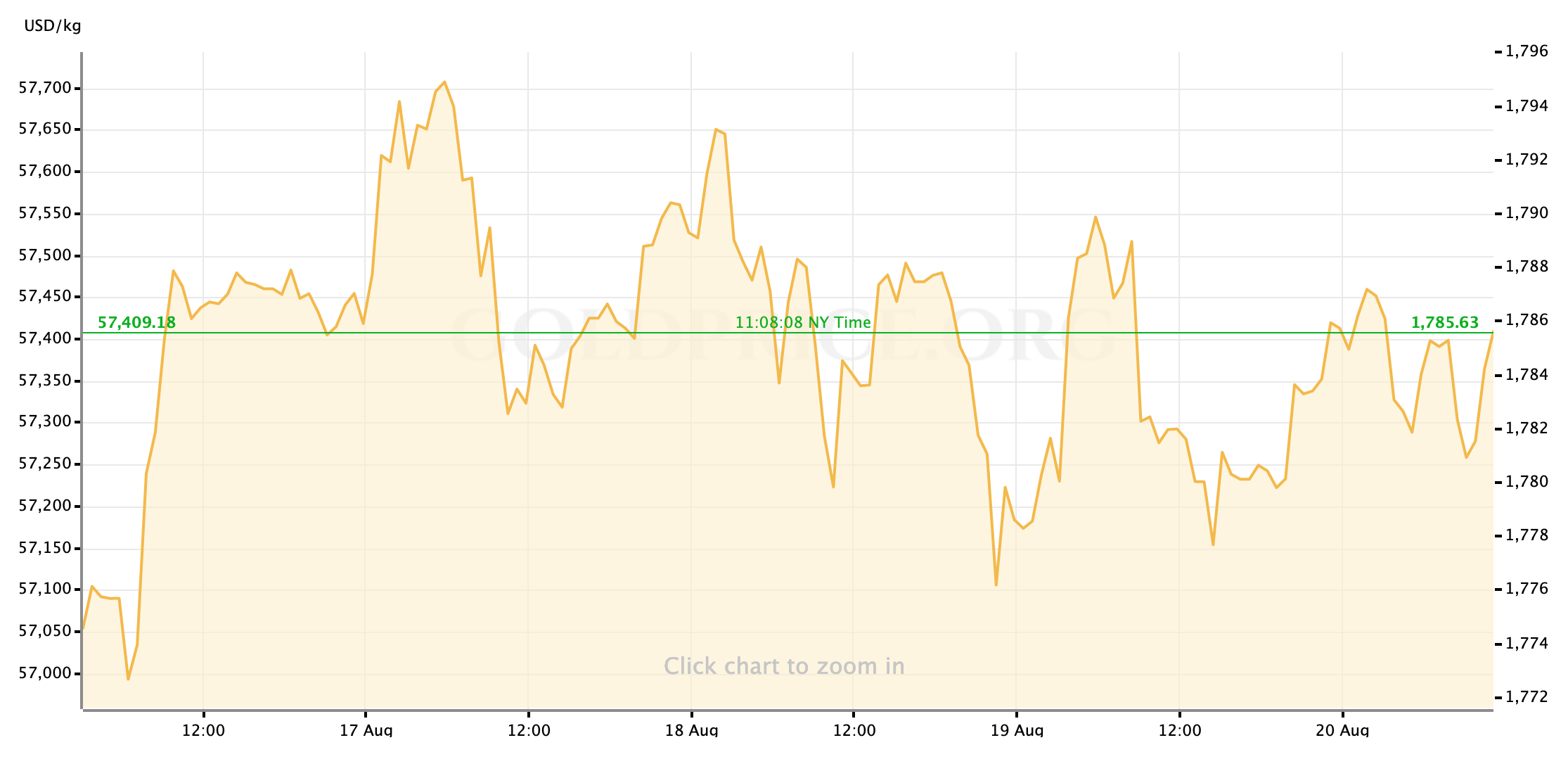

With hindsight and the distance of a month, probably less, we’ll certainly see that this was a relatively uneventful week for our key markets. US equities, although performing well so far on Friday, have been on the backfoot for most of the week under the pressure of global pandemic concerns; But even the roughest trading waters for stocks this week were mostly contained. Gold prices, meanwhile, (and their surly counterpart in US Treasury yields) have been well bounded since the yellow metal’s sharper rally on Monday morning. Since that climb to start the week, gold has stayed within the gravity of $1785/oz. Occasionally making noticeable reaches above or below that level, but always reeling back towards it.

So, lacking any meaningful swings in price over the last week, let’s spend Friday taking a quick accounting of two inputs that didn’t have any lasting impact on gold’s path this week, but do tie into narratives and/or pressure that, going forward, will be in-play for pricing gold, the US Dollar, and other related assets.

1. Wednesday’s FOMC discussion minutes: The minutes and notes form the Federal Reserve’s most recent FOMC meeting revealed little in the way of new information, but the big takeaway for and by investors has been that "most” of the committee’s participants feel that if the US economy continues growing/recovering at the current pace (“current,” now meaning a month ago,) then it will be appropriate to start tapering asset purchases by the end of 2021.

One reason, perhaps, that there wasn’t much in the way of a sustained market reaction to the Fed minutes is that, in the context of the month that has passed since these discussions were actually had, the minutes don’t do much to clarify whether investors should still expect a change to forward guidance (that is, introducing plans to taper) at next week’s Jackson Hole summit.

- Delta variant Covid-19 hospitalizations and deaths have spiked in recent weeks and, as we’ll touch on next, more than a few major market actors are growing more concerned about the extreme downside risks this might present to the US recovery—risks that the FOMC is also taking seriously, per this week’s release. So, from this point, it’s really unclear if the negative developments in the pandemic narrative will be enough to push the Fed back from new guidance next week.

- With that in mind, next week’s Jackson Hole Summit is likely to have a larger immediate impact on Treasury and gold (and Dollar) markets than some may have anticipated just a few weeks ago, for the simple reason that any attempt to price-in whether we’ll see a change to the Fed’s guidance or not seems unreliable at best. Once Powell & Co. tip their hand, we’ll be able to adjust projections through the end of the year, but the initial release of the Chairman’s address may well be a volatile flash for financial markets.

2. Worse than expected performance in Retail Sales last month: The headline number for retail sales ‘growth’ in July reported a much deeper retraction than that -0.3% consensus projection

- As we suggested it might, the broader investor reaction to the -1.1% print sent gold lower that same morning, pulling the spot price down from this week’s one solid attempt to consolidate at a level above $1790/oz.

The concern this data kicks up around investors is, as we said above, the severe (and worsening) downside risks to economic growth poised by this summer’s coronavirus surge that, as yet, doesn’t show any signs of being contained. Economists and other observers are linking the poor Retail Sales numbers to the dive that overall “consumer sentiment” recently took, as measured by the University of Michigan’s survey.

- Lurking in around the same edges is a noticeable slowdown this week in the pace of regional manufacturing activity.

Nobody is hitting the alarm just yet, especially with regards to the Retail data—there are more than a few signals that the slowdown in certain components has more to do with a shift in consumer activity away from the stay-at-home sectors that dominated 2020, towards spending more on services and “experiences” in lieu of buying stuff.

- Still, from a broader view, the worry is clearly growing. At the end of this week, we’re seeing more major analyst desks cutting their projections for economic growth in the US for Q3 and/or 2021 as a whole. Economists are making it very clear that the Delta variant surge is the reason for their gloomier outlooks.

If the Delta variant were to actually push the US economy back into lockdown and/or a recessionary swoon, it’s tough to say exactly how gold prices would react in the short- to medium-term.

- On one hand, the “reopening and reflation” trade contributed in a big way to gold’s rally through the first half of this year, and that tailwind would obviously be blocked-off in a downturn.

- But, on the other hand, we’ve already seen gold, in recent weeks, act a little bit more like the traditional safe-haven it is, historically speaking. Another bear turn for financial markets, however brief, would of course send a good many investors reaching for risk-off positions in gold. At the same time, the Fed would certainly need to communicate a pivot back to extremely dovish monetary policy in order to prop the economy up; This would dent the Dollar and lock-in the low interest rate environment that would allow gold to increase further in value.

This are all still very big “ifs,” on both counts. As markets settle in for the long weekend, the biggest pivot point for markets ahead is next week’s Jackson Hole Symposium, and the revelation of the Fed’s decisions to go ahead with tapering this year, or else wait for more data to follow this Delta summer.

For now, traders, I hope you can get out and safely enjoy your weekend for the next couple of days. After that, I’ll see everyone back here on Monday for our preview of the week ahead.

Gold Price Chart

More articles from John Moncrief