Happy Friday, traders. Welcome to our weekly market wrap, where we take a look back at these last five trading days with a focus on the market news, economic data and headlines that had the most impact on gold prices—and may continue to into the future—as well as the charts for silver, the US Dollar and other key correlated assets.

Gold and silver prices are wrapping up an exuberant week of gains. Both metals’ have been driven higher—alongside other key components of the raw commodities class—as a blockbuster week of US macroeconomic data has accelerated the “reflation trade” in US markets, driving equities and even US Treasury bonds consistently higher.

So, what kind of week has it been?

Projections for a blowout on consumer inflation in March were already so strong ahead of Tuesday’s report, that even a beat of +0.1% (YoY) was enough to send markets into reveries. The less-volatile “core” component of price inflation came in at 1.6% for last month, while a surge in gas prices in particular drove the headline number to 2.6%.

- Experts and investors are in broad agreement that this surge in prices is a direct result of two things, both pillars of your high school econ class: a huge spike in demand (and spending) driven by the reopening of large parts of the US economy post-lockdown, timed with a massive influx of capital and cash thanks to the most recent fiscal stimulus measures; and tightening supply resulting from manufacturing/supply chain shortages and slowdowns throughout the pandemic (and even more acute shocks, like last month’s Suez Canal quagmire.)

- What market participants have been less harmonious about (as evidenced by 2021’s sovereign bond markets) is what comes next: Is this sharp tick higher in CPI (as the Fed and the White House believe) primarily in reaction/relative to a torpid 2020, and therefore will ultimately be “transitory” as the US economy takes a longer time to fully recover? Or is it the first sign of a powerful, immediate overheating of inflation that will put a damaging drag on growth?

- Regular readers will know that I’ve come down firmly on the side of the former; The impact that we can see March’s outsized spike in gasoline prices had on the overall inflation function, I think, is evidence of the argument that any surge in inflation this year will be temporary is the most correct.

Investors now seem to finally be more receptive and/or accepting of this narrative— the one that says the FOMC will not be pushed by these numbers towards raising interest rates anytime in the near- to medium-term—as evidenced by the market’s reaction to Tuesday’s CPI report.

- US Treasuries, which were already rallying in the earlier pre-market, rallied sharply; The benchmark 10-year’s yield collapsed well below 1.65% and the US Dollar weakened alongside it, kicking off a downtrend that would characterize the Greenback’s trading week. US stock markets, unsurprisingly, had a very strong day with the S&P and NASDAQ both setting records.

- Each of these moves signal a fading of hawkish expectations for higher interest rates coming before the FOMC is saying to expect them.

With the headwinds of a strengthening Dollar and higher implied yields taken away, gold prices punched higher on Tuesday morning, from a morning base near to $1730/oz to a peak just below $1750. After a mild pullback from resistance, the yellow metal held its strong gains and closed the session as good as $1745.

- Silver participated in the run as well, consolidating strength above $25/oz.

Thursday morning brought another raft of macro data that’s driven another surge in investors’ confidence in a US economic recovery. Even though the individual data points may not bring as much attention as Tuesday’s inflation read, they indicate that the American economic engine may finally be kicking into the next gear after a lost pandemic year.

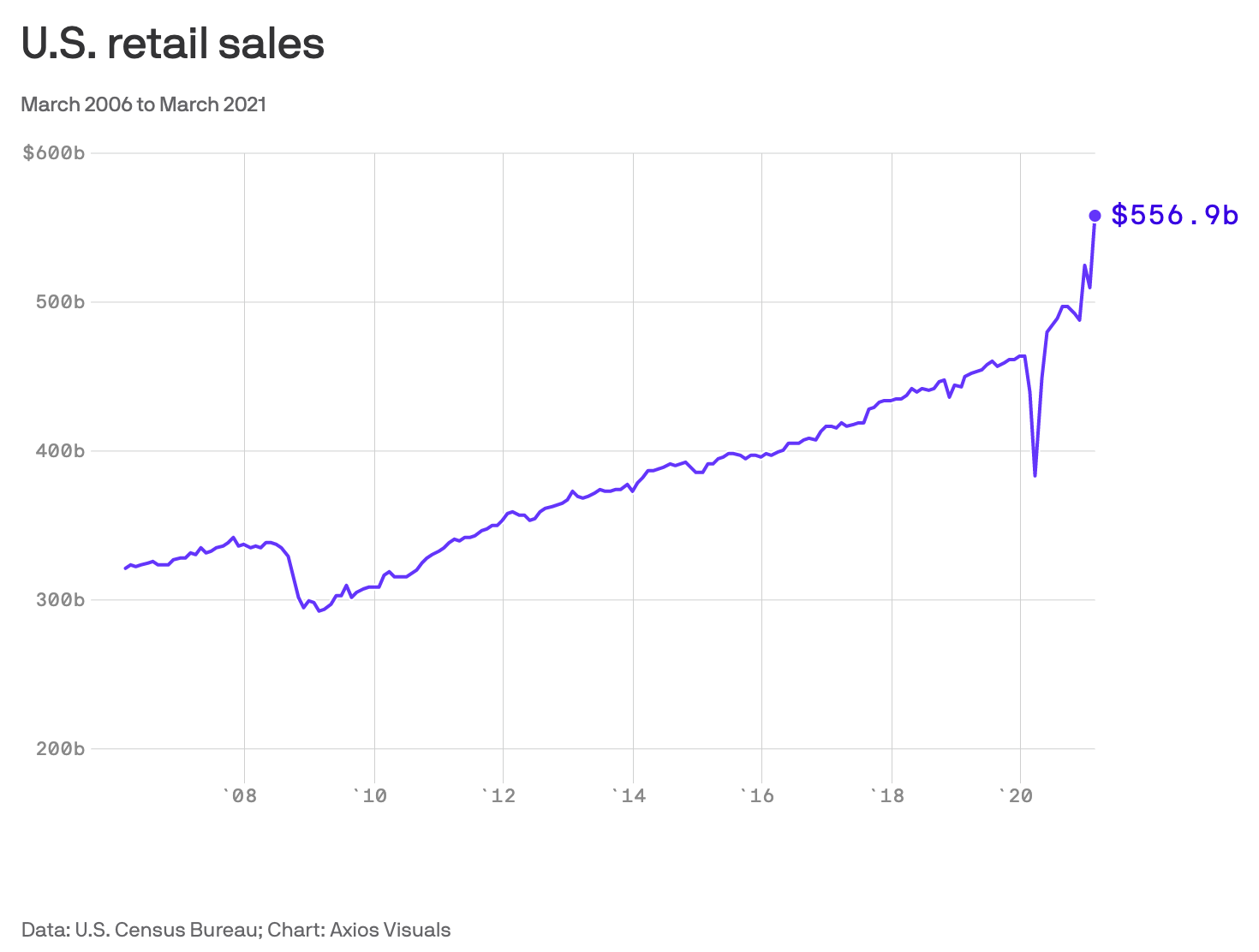

- The same factors that, from the demand side, had driven consumer price inflation to new levels in March also contributed to a massive monthly jump in retail sales just shy of 10%. Americans’ spending in restaurants and bars, in particular, surged last month.

- While some observers (ed. note: Yours truly) have been concerned that initial jobless claims might oscillate around the 700,000 level for several weeks as it had done with stubbornness at 800K, this week’s report counted “just” 576,000 new unemployment claims. Historically speaking, the rate of new job-losses each week remains horrifically high. But Thursday’s number is the lowest that the US economy has seen in over a year.

- If regional surveys are any indicator—and they, by definition, literally are—the US manufacturing sector continues to lead the way towards broad economic recovery. Sure, in a week (on a single day, even) that’s offered such strong outperformance in economic data an index on manufacturing activity in New York state hitting at 3+ year high might seem quaint; But can I interest you in this week’s Philly Fed Manufacturing Index, which reached a 48-year high?

- These indicators from the industrial sector also inform, I think, the growing acceptance by investors that pops in inflation like we’re seeing this week (as well as inflation in producer prices which have been creeping higher in recent weeks) are transient: With US manufacturing accelerating at this rate, I expect production to catch up with at least a large chunk of the current supply imbalances and remove that upward pressure on prices for the time being.

Propelled by the week’s macroeconomic green lights, stocks and bond prices have continued to surge since Thursday morning. All three benchmark equity indexes have continued make new highs through the week, including the Dow Jones Industrial Average, which closed Thursday’s session above 34,000 for the first time ever. At the same time, the assumption by some investors that recent data would shanghai the Fed into hiking rates “early” continued to fade, as did the selling pressure on bond markets: Overall investors optimism pushed the 10-year yield well below 1.6% on Thursday and the indicator fell as far as 1.53% before stabilizing to end the week. The US Dollar’s nearly week-long slide accelerated as well

And, once again, gold prices immediately benefited from market momentum into the reflation trade. The yellow metal strengthened by $20+ following Thursday’s macro data, and the momentum as carried on through Friday. As of Friday afternoon, gold spot prices are beyond the 6-week highs at nearly $1780/oz.

- With the markets full of “feel good”, the reflation trade has to potential to carry precious metals prices further and higher in the weeks ahead as it’s (traditionally) a play that benefits raw material commodities—evidenced by the strong week that other commodities like crude oil have enjoyed.

- That said, for gold’s outlook in particular we’ll need to keep an eye on just how high and hot the stock market runs. While crude oil, other industrial commodities, and even silver can see their spot values appreciate alongside accelerating equities, gold might get outpaced if investors’ risk appetite continues to surge.

- With a sparse schedule in terms of economic data, that relationship will be where we focus to begin next week’s trading.

For now, traders, I hope you can get out and safely enjoy your weekend for the next couple of days. After that, I’ll see everyone back here on Monday for our preview of the week ahead.

Gold Price Chart

More articles from John Moncrief