Good morning, traders; Welcome to our market week preview, where we take a look at the economic data, market news and headlines likely to have the biggest impact the price of gold this week and beyond, as well as market prices for silver, the US Dollar, and other key correlated assets.

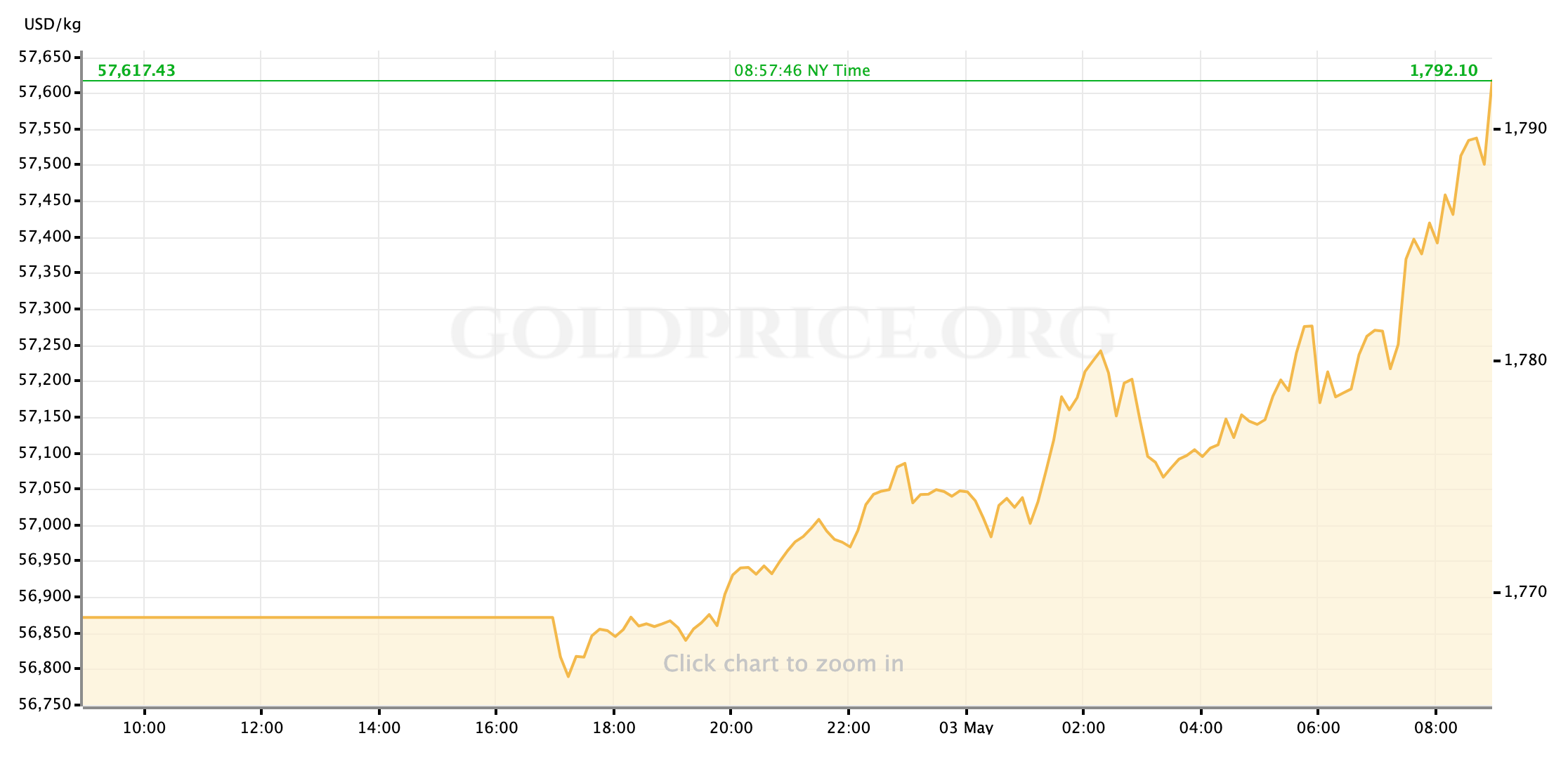

Gold prices are strongly higher this morning as the trading week begins in the US. The yellow metal has risen strongly through the overnight sessions as last week’s rally in sovereign bond yields has tapered back, removing the most dominant headwind that gold faced over the last 10 days.

With spot prices once again approaching a re-test of $1800/oz, I’ll be keeping an eye on the inverse correlation between gold and the 10-year Treasury yield. On the data calendar, we have a host of relevant macroeconomic data, all of which are expected to indicate continued acceleration towards recovery in the US economy. For much of this year, when spiking bond yields haven’t been a limiter, gold has been able to participate with other commodities rallying within the “re-opening/reflation trade.” With this week’s economic data expected to accelerate the sentiment behind those patterns, I’m interested to see if gold can continue playing along.

US Economic Data to Watch

Monday, May 3 at 10am EDT // ISM Manufacturing PMI (April)

[consensus est.: 65.0 // prev.: 64.7]

Regional manufacturing data and other inputs strongly suggest that the sector, on a national level, continued its recent record activity acceleration last month. Investors and analysts are likely baking this kind of performance—characteristic of the economic recovery we all hope to see this year—into their pricing models; so there’s low probability of big swings as a result of Monday’s manufacturing PMI (or for Wednesday’s service sector read.) Still, I expect this will help kick off the re-opening/reflation trades to start the week, in which gold can potentially participate in a move higher.

Wednesday, May 5 at 815am EDT // ADP Employment Report (April)

[consensus est.: +810K // prev.: +517K]

Recently—certainly over the last year or so—the monthly ADP print has become less a data point to be traded around in its own right, and more so an opportunity for traders to shift their final positions going into Friday’s Jobs Report. There’s not a particular trade or swing to lookout for on Wednesday morning, then; Even though we can pretty confidently expect a very healthy number. Instead, just be aware that trading volume will likely pick up, and to keep an eye out for any big surprises in the number that may impact the gold (or US Dollar) market’s outlook for the Non-Farm Payrolls data due at the end of the week.

Wednesday, May 5 at 10am EDT // ISM Services PMI (April)

[consensus est.: 64.1 // prev.: 63.7]

Because “services” are far and away the most dominant driver of the modern American economy, the expected continuation of Services PMI’s own record highs will probably spur even more (possibly irrational) exuberance in equities and other risk markets than will Monday morning’s manufacturing sector read. I’ve talked in recent weeks about a potential fork in the reflation trade: a point where the excitement for a ripping stock market rally leaves precious metals behind as investors loose interest in the non-yielding safe-havens. While I’m still not convinced that we’re really all that close to such an inflection, I’ll be looking to see if this week’s Services PMI pushes us closer before Friday’s NFP.

Thursday, May 6 at 830am EDT // Initial Jobless Claims

[consensus est.: +540K // prev.: prev.: +553K]

As usual in a week that concludes with a monthly Jobs Report, this week’s higher-frequency labor market data will be mostly overlooked. A sudden snap back to higher unemployment claims—say, something over 600K—would probably spook investors into risk-off (which, in the current paradigm, probably means lower gold, higher Dollar and Treasury yields); Otherwise, I expect markets to look past Initial Claims data this week.

Friday, May 7 at 830am EDT // April Jobs Report

[(NFP) consensus est.: +978K // prev.: +916K]

[(unemployment) consensus est.: 5.7% // prev.: 6.0%]

This week’s Jobs Report may, based on projections, accomplish what inflation hawks and wannabe “bond vigilantes” tried to do in the first quarter of this year: Impact the timing of the Fed’s liftoff from ultra-low interest rates and supportive monetary policy. To be clear, even a headline “NFP jobs added” number above 1 Million—which is a pretty popular call this week—won’t bring tapering or rate hikes onto the calendar before 2022; The Fed will (rightly) be able to point out that the labor market recovery is meaningful but far from complete. But improvement in the labor market data does carry with it a weight that has been absent from the recent upticks in inflation data, which can be written off as transitory and relative to 2020’s recessionary weakness. Friday’s Jobs Report will be another point where I’ll be watching to see if gold’s participation in the re-opening rally peters out, as enthusiasm for an all-out economic recovery sends investors’ cash into higher-risk for higher yield than the yellow metal can offer.

FedSpeak this Week

On the heels of last week’s FOMC meeting, we have a decent roster of public comments from Fed officials. Expect the speakers to continue toeing the party line with regards to recent inflation metrics reflecting an increase that will only be transient, meaning the Fed will remain in an ultra-accommodative stance for quite some time as planned. We may also get some commentary on how FOMC participants anticipate the Biden Administration’s proposed tax increases, officially presented last week, might impact market conditions and activity. It will feel a bit like a piece of the puzzle is missing as all of these appearances will come before Friday’s Jobs Report, so we’ll have to wait until next week to see how Powell & Co. react to revised labor market assessments. Here are the most noteworthy Fed appearances this week:

Monday: Fed Chair Jerome Powell (FOMC voter) (220pm EDT)

Tuesday: San Francisco Fed President Mary Daly (FOMC voter) (1pm)

Wednesday: Chicago Fed President Charles Evans (FOMC voter) (930am); Cleveland Fed President Loretta Mester (non-voter) (12pm)

Thursday: Dallas Fed President Robert Kaplan (non-voter) (10am)

And that’s how the week lays out ahead of us, traders. As always, I wish you all the very best of luck in your markets in the coming days, and I’ll look forward to seeing you all back here on Friday for our market-week wrap up.

Gold Price Chart

More articles from John Moncrief