Good morning, traders; Welcome to our market week preview, where we take a look at the economic data, market news and headlines likely to have the biggest impact the price of gold this week and beyond, as well as market prices for silver, the US Dollar, and other key correlated assets.

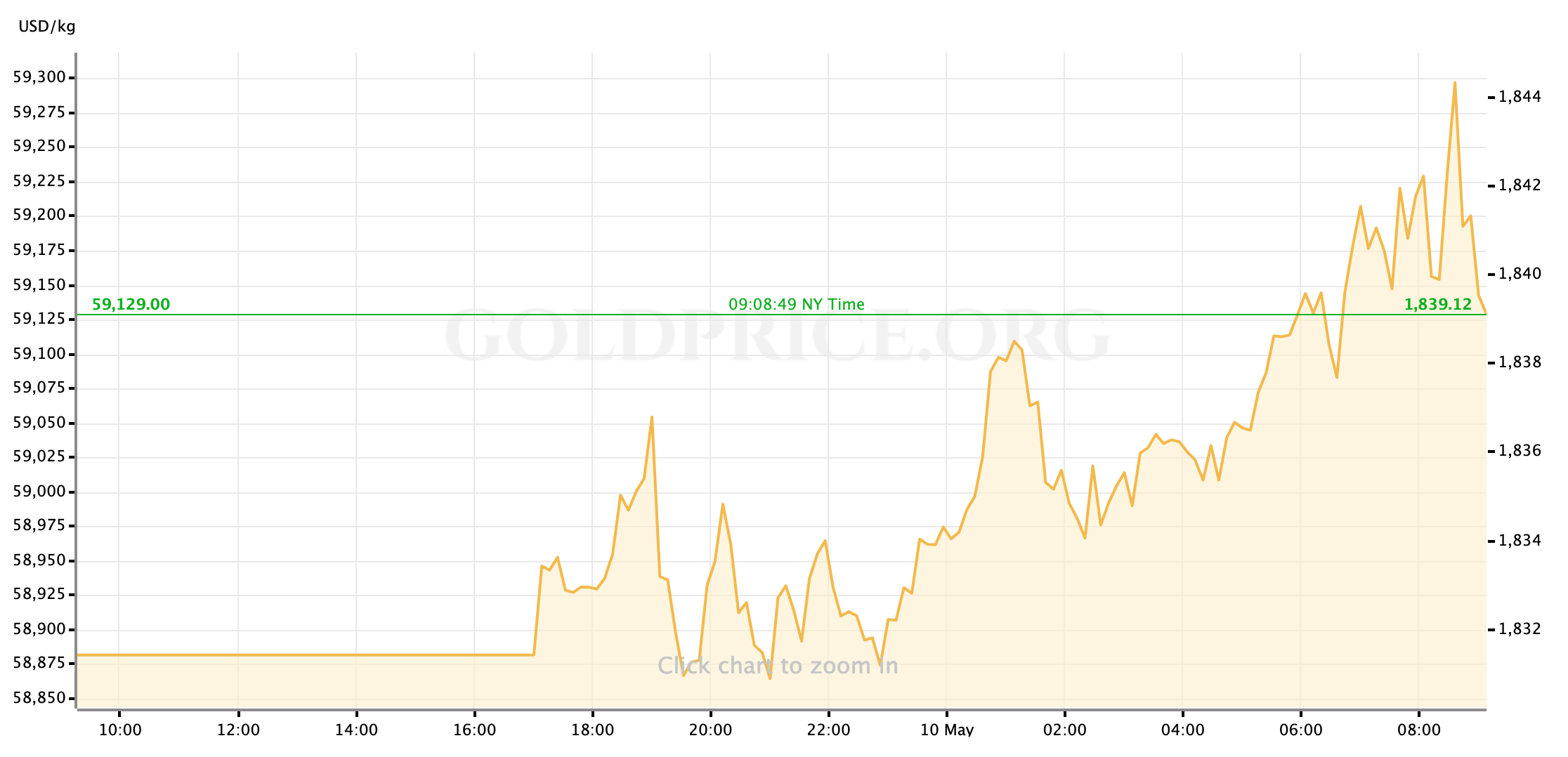

Gold prices are starting the week on the front foot again, trading at a premium of roughly $10/oz to Sunday night’s opening bids. The yellow metal is likely getting some extra momentum from hand-wringing about raw material price inflation, which is seeing most major players in the global commodities basket pushed higher by projected demand, also providing some lift to gold (and silver) prices.

In US markets, this week’s macroeconomic focus will be on a new read of consumer inflation levels—from which point, moving forward, we’ll be able to see if the Fed is correct in labeling this increase in prices as “transient”—as well as economists and policy-makers attempting to grapple with the meaning (if there is any) behind last Friday’s majorly disappointing Jobs Report.

US Economic Data to Watch

Wednesday, May 12 at 830am EDT // CPI Inflation (April)

[(core CPI) consensus est.: +2.3% YoY // prev.: +1.6%]

[(headline) consensus est.: +3.6% YoY // prev.: +2.6%]

Analysts and investors are expecting an unusually strong pop in year-over-year consumer inflation, driven mainly by two recent factors: the post pandemic resurgence in components like travel (airfare, hotels, etc.) and recreation relative to April 2020 data marred by Covid lockdowns; and the recent supply chain disruptions caused by the pandemic which hadn’t been unwound before re-opening in the US and other vaccine-rich economies boosted demand. This CPI data set has lost some of the urgency that it might have had last week, before the April Jobs Report gave the Fed cover to hold interest rates and monetary policy in place for a while longer as the labor market continues recovering. Still, this is probably the sharp spike in inflation data that we’ll use to see if Chairman Jerome Powell and other Fed officials are correct in assuming that these price pressures will be transitory for now, and that the US economy also has a way to go before reaching the Fed’s mandate of price stability at 2% inflation. From a gold markets perspective, it’s possible that the yellow metal might catch a tailwind here whether the data comes in as-expected (because gold may get some play as a traditional inflation hedge, without the recent pressure of Treasury rates surging in an effort to challenge the Fed,) or whether it misses to the downside (in which case we’ll see a repeat of last week: the broader reflation trade celebrating the promise of super cheap interest rates through 2022.)

Thursday, May 13 at 830am EDT // Initial Jobless Claims

[consensus est.: +495K // prev.: +498K]

It would be an objectively positive signal for Initial Jobless Claims to hold at, or below, 500K for second week; But the reverberations of Friday’s labor market stumble will be felt here, too, as markets may be less willing to celebrate the good news after getting burned so badly by five weeks of strong weekly jobs data that culminated in a shockingly poor monthly set.

Friday, May 14 at 830am EDT // Retail Sales (April)

[consensus est.: +1.0% MoM // prev.: +9.7%]

Last month, we saw an historic spike in Retail Sales, as the first month of mass vaccinations in the US coincided with another issuance of direct stimulus payments into many American’s bank accounts. A retracement to 1% in April looks like an abrupt slowdown at first, but it is a pace of retail growth closely in line with the mathematical mode over the last decade, so it should imply that the post-pandemic recovery is continuing at pace. Non-Farm Payrolls and the unemployment rate were not the only macroeconomic indicators to slip (slightly or otherwise) last week, however: activity gauges for the manufacturing and services sectors in the US, while still performing historically well, slid unexpectedly as well. It may be worth keeping an eye out then, for pauses or pullbacks elsewhere in April’s data that could indicate a hitch in the trajectory of this US economic recovery. It seems unlikely, at this point, to dampen the pace of the re-opening/reflation trade that has lifted gold prices higher in recent weeks; But it would certainly be better to not be caught offsides by such a turn.

FedSpeak this Week

We have a busier slate of FOMC participant appearances this week, which is just as well since there’s actually something new to talk about; Namely: the dismal labor market data from last week’s Jobs Report. Fed officials have spent the last several weeks defending their plan to hold monetary policy ultra-easy for longer, often by arguing that the US labor market recovery still has a considerable way to go. Sure, most of them could use their public comments this week to just say “We told you so,” but the fact that they are highly placed officials in the Federal Reserve leads me to think they’re more likely to discuss what the stutter in US jobs growth actually suggests for the economy now and in the near term.

Monday: Chicago Fed President Charles Evans (FOMC voter) (2pm EDT)

Tuesday: New York Fed President John Williams (FOMC voter) (1030am); Fed Governor Lael Brainard (FOMC voter) (12pm); San Francisco Fed President Mary Daly (FOMC voter) (1pm); Atlanta Fed President Raphael Bostic (FOMC voter) (115pm); Minneapolis Fed President Neel Kashkari (non-voter) (230pm)

Wednesday: Fed Vice Chair Richard Clarida (FOMC voter) (9am); Atlanta Fed President Bostic (1pm)

Thursday: Fed Governor Christopher Wallace (FOMC voter) (1pm); St Louis Fed President James Bullard (non-voter) (4pm)

And that’s how the week lays out ahead of us, traders. As always, I wish you all the very best of luck in your markets in the coming days, and I’ll look forward to seeing you all back here on Friday for our market-week wrap up.

Gold Price Chart

More articles from John Moncrief