Good morning, traders; Welcome to our market week preview, where we look at the economic data, market news and headlines likely to have the biggest impact the price of gold this week and beyond, as well as market prices for silver, the US Dollar, and other key correlated assets.

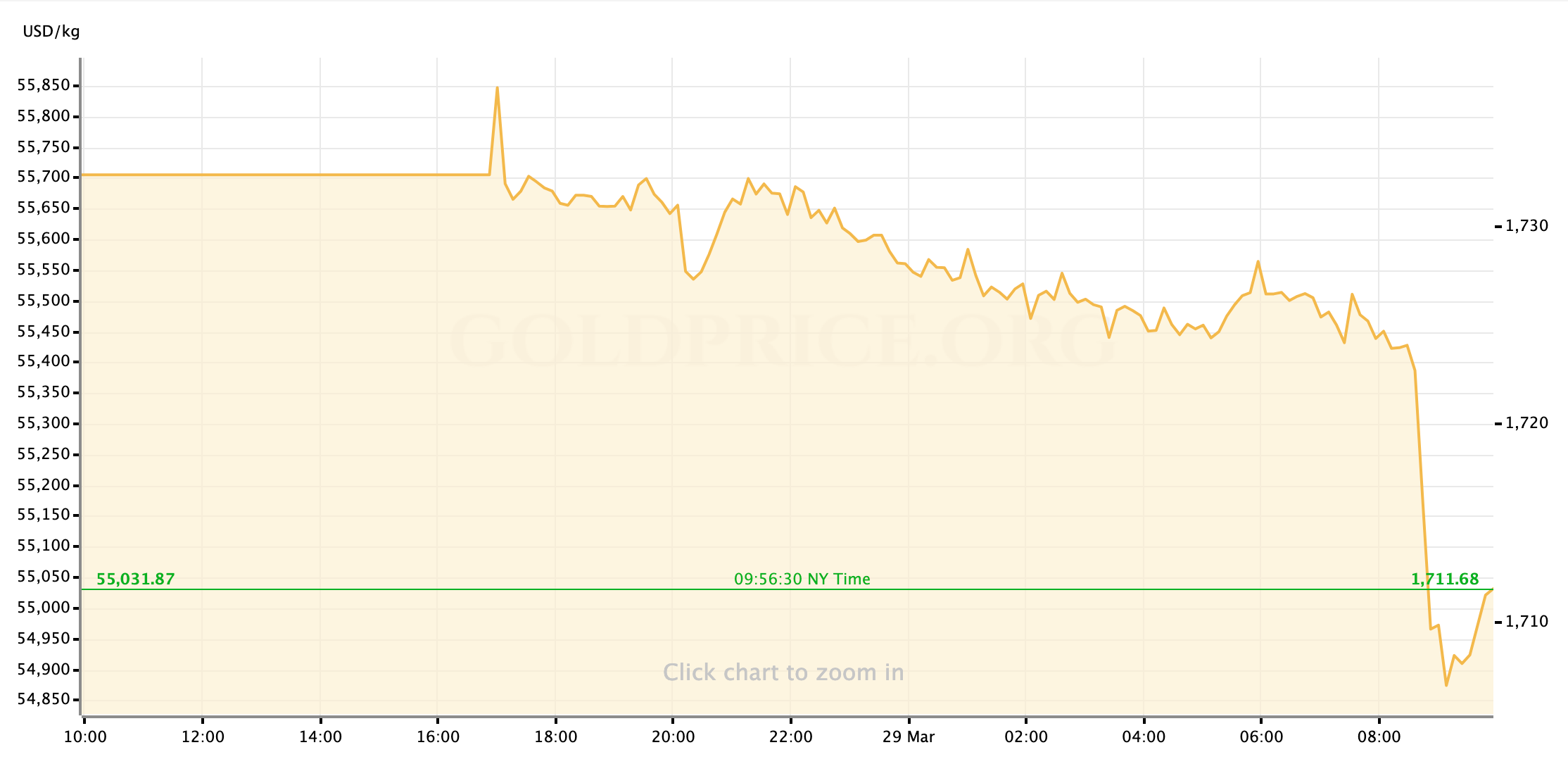

Gold prices are substantially lower on Monday morning, roughly an hour after the start of trading in the US stock market.

While the yellow metal had weakened somewhat during overnight trading, the aggressive sell-off was timed to the start of cash trading in the US. Markets have been on edge since the end of trading on Friday afternoon, when markets and observers were caught off guard by a massive run of block-selling in US stocks. While the cause was unknown at the time, it turned out to be the forced liquidation of positions held by a US hedge-fund which had failed to meet margin requirements. While it doesn’t seem, as of now, that this points to any deeper systemic risk (a la 2008,) the world’s developed markets have been uneasy to start the week. With reports over the weekend that a number of Wall Street’s biggest banks were involved with forcing the liquidation (which will translate to big losses on their own balance sheets,) financial stocks plummeted as soon as trading opened and have been leading the broader equity markets lower since. On trend with recent weeks, investors’ preference for safety this morning seems to be USD cash, as Treasuries have also sold-off along with stocks and the precious metals.

My outlook is that, while it may take the better part of today, if there are no other negative headlines from Archegos margin default to contend with then markets should eventually settle back down with ease. (And we’ve already gotten the ostensibly positive news that the blockage of the Suez Canal has been resolved, allowing global supply chains to unclench, if only a bit.) From there, gold should be allowed some room to rebound; The question, of course, is how far prices may fall before the calm. This morning, $1700/oz seems to be reliable as support.

Our macroeconomic calendar doesn’t feature any relevant datapoints before midweek, so we’ll be keeping an eye on the market’s effort to find solid footing this morning. For now, let’s look at what we have coming from Wednesday on.

US Economic Data to Watch

Wednesday, March 31 at 815am EDT // ADP Employment Report (Mar)

[consensus est.: +550K // prev.: +117K]

We’ve seen a solid, and at times surprising, improvement in the high-frequency labor market data in March; Particularly in the Initial Jobless Claims numbers from the last couple of weeks. With that in mind, analysts and economists are projecting a strong performance from Friday’s Jobs Report and that positive outlook naturally filters down the expectations for ADP’s private payroll growth numbers mid-week. A few desks are noting that there could be a risk of slightly weaker than expected headline read due to some technical inefficiencies in accounting for Americans returning to work as the economy continues reopening. There’s always a chance of the market having a knee-jerk reaction to the ADP number it’s noticeably above or below expectation: An outperformance boosts risk-appetite while a miss pushes impulsive actors to safety. We’ll need to see some of this week’s trading trends before we can say for certain in investors will be most interested in gold as a safe haven or if it will continue to benefit from the “reflation trade” if economic data signals continued recovery. (On Monday morning, at least, it seems gold continues to be strongly driven by moves in the bond market.)

Thursday, April 1 at 830am EDT // Initial Jobless Claims

[consensus est.: +680K // prev.: +684K]

Last week’s drop in new unemployment filings was steep and unexpected enough that a more moderate week-to-week change is the safe call here. That said, I remain wary of the prior week’s data getting revised meaningfully higher or possibly a snap to numbers north of 700K. The data will be useful for refining outlook and modeling going into Q2, but the market tends to brush initial claims numbers aside on the week of the more impactful monthly jobs report.

Thursday, April 1 at 10am EDT // ISM Manufacturing PMI (Mar)

[consensus est.: 61.4 // prev.: 60.8]

Seeing the Manufacturing PMI—a metric for the perceived growth of the industrial sector of the US economy—registers over 60.0 is a big deal; It surprisingly cleared that level in February and economists are looking for another step higher this week. Honestly, as the US economy as a whole works to grow itself out of the pandemic’s recessionary damage, the initial tick above 60 last month probably buys a lot of good will. I don’t think any (human) investors get spooked by anything better than 56.5 this time around. More likely, this will be another healthy number as the manufacturing sector has been performing well since the fall of 2020 while the rest of the American economy faltered. That outperformance will probably be a mild headwind for gold prices, either because investors will pivot to bigger risks, or because the inflation hawks will come to push bond markets around again.

Friday, April 2 at 830am EDT // March Jobs Report

[(NFP) consensus est.: +643K // prev.: +379K]

[(unemployment) consensus est.: 6.0% // prev.: 6.2%]

The month of March brought together a host of factors that seem certain to result in a booming month of jobs growth: expansive success in vaccinating the first, most vulnerable cohorts of Americans; a massive fiscal stimulus package making it easier to put folks back to work; and the absence of February’s punishing winter weather are the prime drivers. And, as I mentioned earlier, recent Initial Jobless Claims data backs this up. Initially, gold prices may see a lot of downward pressure when the NFP number hits the transom. A surge in job-added certainly signals growth and the promise of recovery, and there will be those who misunderstand—willfully or otherwise—this to represent a big step towards the Fed’s recently enshrined objectives for lasting full employment. I won’t be at all surprised to see US Treasury yields spike again, at least initially, which has proven to be a reliable headwind for gold. That pressure should eventually ease—maybe before the start of next week, maybe not—as the “smarter” money in the market realizes that even such a large monthly gain in new American jobs leaves the US labor market woefully off the pace that it kept at the start of 2020 and far away from the Fed’s stated requirements for even considering a rate hike.

And that’s how the week lays out ahead of us, traders. As always, I wish you all the very best of luck in your markets in the coming days, and I’ll look forward to seeing you all back here on Friday for our market-week wrap up.

Gold Price Chart

More articles from John Moncrief