Good morning, traders; Welcome to our market week preview, where we look at the economic data, market news and headlines likely to have the biggest impact the price of gold this week and beyond, as well as market prices for silver, the US Dollar, and other key correlated assets.

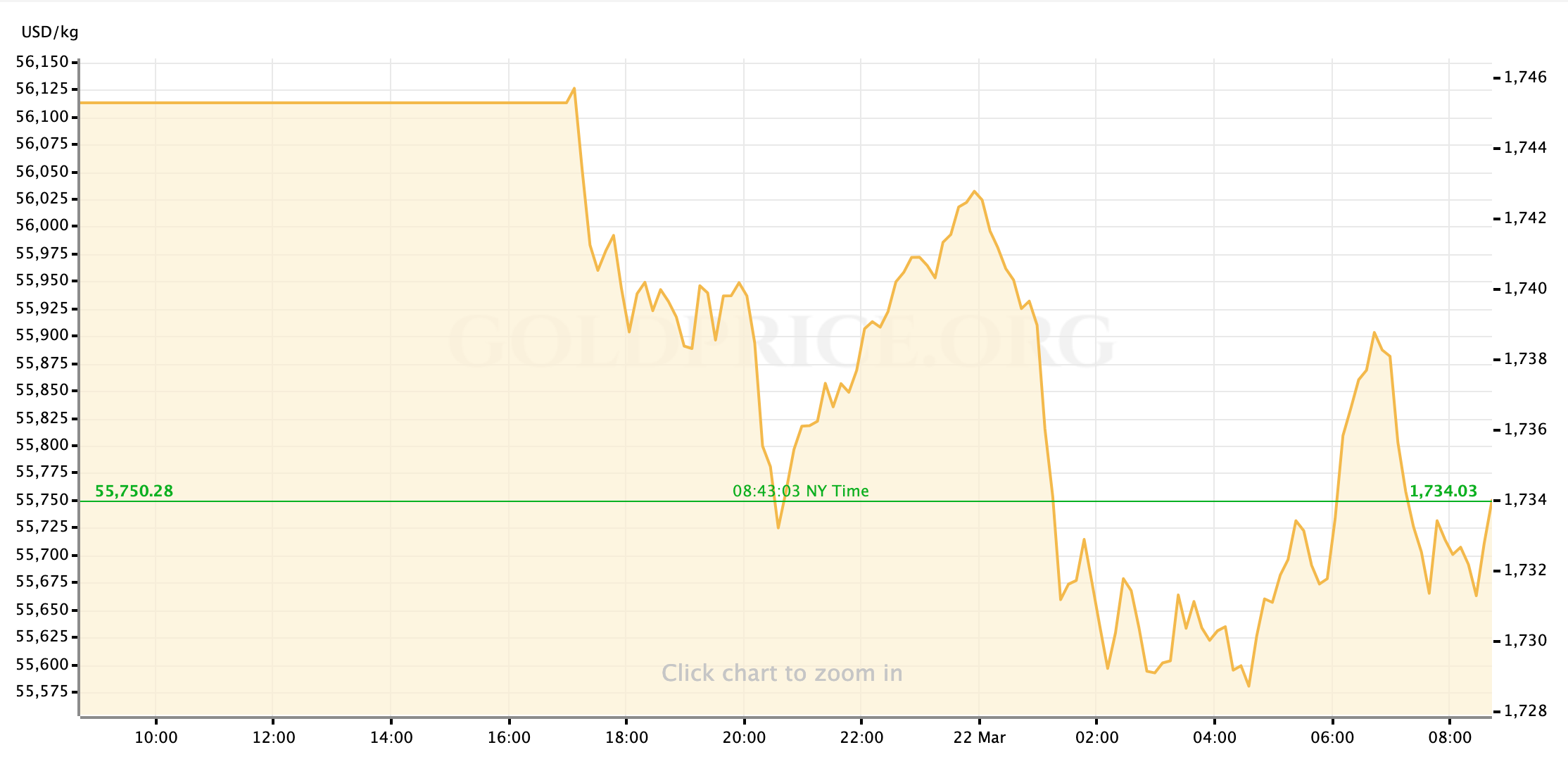

Gold prices are trading lower this morning, as sovereign bond markets have been rallying overnight at the expense of most other major assets: gold, the Dollar, and most DM stock markets have been knocked onto the back foot to begin the US trading week.

As US equity markets are opening for the day, we’re seeing the bond rally start to taper a bit as 10-year Treasury yields attempt to move back to 1.7% and the space is allowing gold and silver prices to recover somewhat. With the Dow falling at the open and the S&P and NASDAQ indices both getting out ahead, the stock market may be signaling that the overnight trade is unwinding a bit—in which case I would expect gold to target a return to $1740/oz—but it’s still too early to tell.

For now, let’s have a look at the macro calendar for the week ahead.

US Economic Data to Watch

Wednesday, March 24 at 830am EDT // Durable Goods Orders (Feb)

[consensus est.: +0.7% MoM // prev.: +3.4%]

Based on analyst expectations, Durable Goods will be the next report to show some drag from the rough winter storms that pinched or shut down large parts of the US, particularly Texas, last month. Because the industrial sector has been very resilient since even before mass-vaccination plans became a reality in the US, the slide shouldn’t be too steep or concerning on its own. Looking ahead, many economists will probably chalk even a contraction up to being a transitory blip as more the of US economy reopens, building up expectations for strong growth in this and similar metrics in the spring. A disappointing print here might add some selling pressure to the raw commodities (like gold, but especially silver) and US equities briefly this week; Though expect that these assets will have regained their footing well before Wednesday morning.

Thursday, March 25 at 830am EDT // Initial Jobless Claims

[consensus est.: +730K // prev.: +770K]

Last week’s sharp rise in the reporting of new unemployment claims wasn’t all that surprising, given how sticky these historically high numbers have been since autumn. A drop this week seems reasonable, but certainly not guaranteed, but I’ll be looking at any revisions to the prior number to get a sense of how difficult (or not) it will be for the headline number to finally drop below an ugly 700,000. The Dollar and gold prices have been mostly unreactive to weekly labor data (except for big up- or downside misses,) but with a slow news week expected, there may be more investor attention on the stubborn labor market.

Friday, March 26 at 830am EDT // PCE Inflation (Feb)

[(core PCE) consensus est.: +1.5% YoY // prev.: +1.5%]

[(headline PCE) consensus est.: +1.6% YoY // prev.: +1.5%]

Friday, March 26 at 830am EDT // Personal Income & Spending (Feb)

[(income) consensus est.: -7.2% MoM // prev.: +10.0%]

[(spending) consensus est.: +-0.8% MoM // prev.: +2.4%]

Remaining well below 2% as we head into the possibly roaring spring of 2021, the Fed’s measurements of US price inflation will affirm the view, laid out by policy makers last week, that the US economy has a long way left to go before reaching escape velocity on the recovery and “overheating” inflation. While this may allow Treasury yields to remain at or around 12-month highs on the longer end of the curve, it should promote US stocks as well as the longer-term plays of the reflation trade, which ought to be a good source of support for higher gold prices. Investor tantrums like we saw last Thursday, though, are a reminder that in the current market environment there are those who will continue to insist that some version of Weimar hyperinflation is just around the corner. So, while a (mild) miss on inflation probably changes little short-term, a surprise well to the upside (let’s say above 1.8% YoY, to pick a number)—while easily outside of expectations—would probably set the inflation hawks off again, spiking Treasury yields even higher. Intuitively, you would think anything driven by inflation fears would be boon for gold investment; But such move would be so acute that, based on recent patterns, it would be more likely to see everything but the US Dollar (and possibly stock market sectors like energy and financials) taking a hit on the day.

Personal Income & Spending will almost certainly be down in the February data but, in a line, we’re becoming for familiar with in analyst notes, it’ll be pretty easily written off as a brief ‘blip’ between stimulus rounds.

FedSpeak this Week

The center piece of a crowded schedule for FOMC appearances this week will be Fed Chair Jerome Powell’s regular testimony before the Senate and House on Tuesday and Wednesday, respectively; For the first time, Powell’s neighbor joining him from the Treasury Department will be former Fed Chair Janet Yellen. There are plenty of other engagements for relevant Fed officials though, and I imagine markets will keep an eye on several of them for some added color around last week’s updated economic projections from the Fed. I expect a quiet but consistent effort over the next three months to ferret out which members represent the anonymous dots that anticipate raising interest rates before the end of 2023.

Monday: Richmond Fed President Thomas Barkin (FOMC voter) 1030am EDT); Fed Governor Michelle Bowman (FOMC voter) (715pm)

Tuesday: St. Louis Fed President James Bullard (non-voter) (9am); Fed Chair Jerome Powell (FOMC voter) (12pm); Fed Governor Lael Brainard (FOMC voter) (345pm)

Wednesday: Fed Chair Powell (10am); New York Fed President John Williams (FOMC voter) (135pm); Chicago Fed President Charles Evans (FOMC voter) (7pm)

Thursday: Atlanta Fed President Raphael Bostic (FOMC voter) (12pm); Fed Vice Chair Richard Clarida (FOMC voter) (345pm); San Francisco Fed President Mary Daly (FOMC voter) (7pm)

And that’s how the week lays out ahead of us, traders. As always, I wish you all the very best of luck in your markets in the coming days, and I’ll look forward to seeing you all back here on Friday for our market-week wrap up.

Gold Price Chart

More articles from John Moncrief