Good morning, traders; Welcome to our market week preview, where we take a look at the economic data, market news and headlines likely to have the biggest impact the price of gold this week and beyond, as well as market prices for silver, the US Dollar, and other key correlated assets.

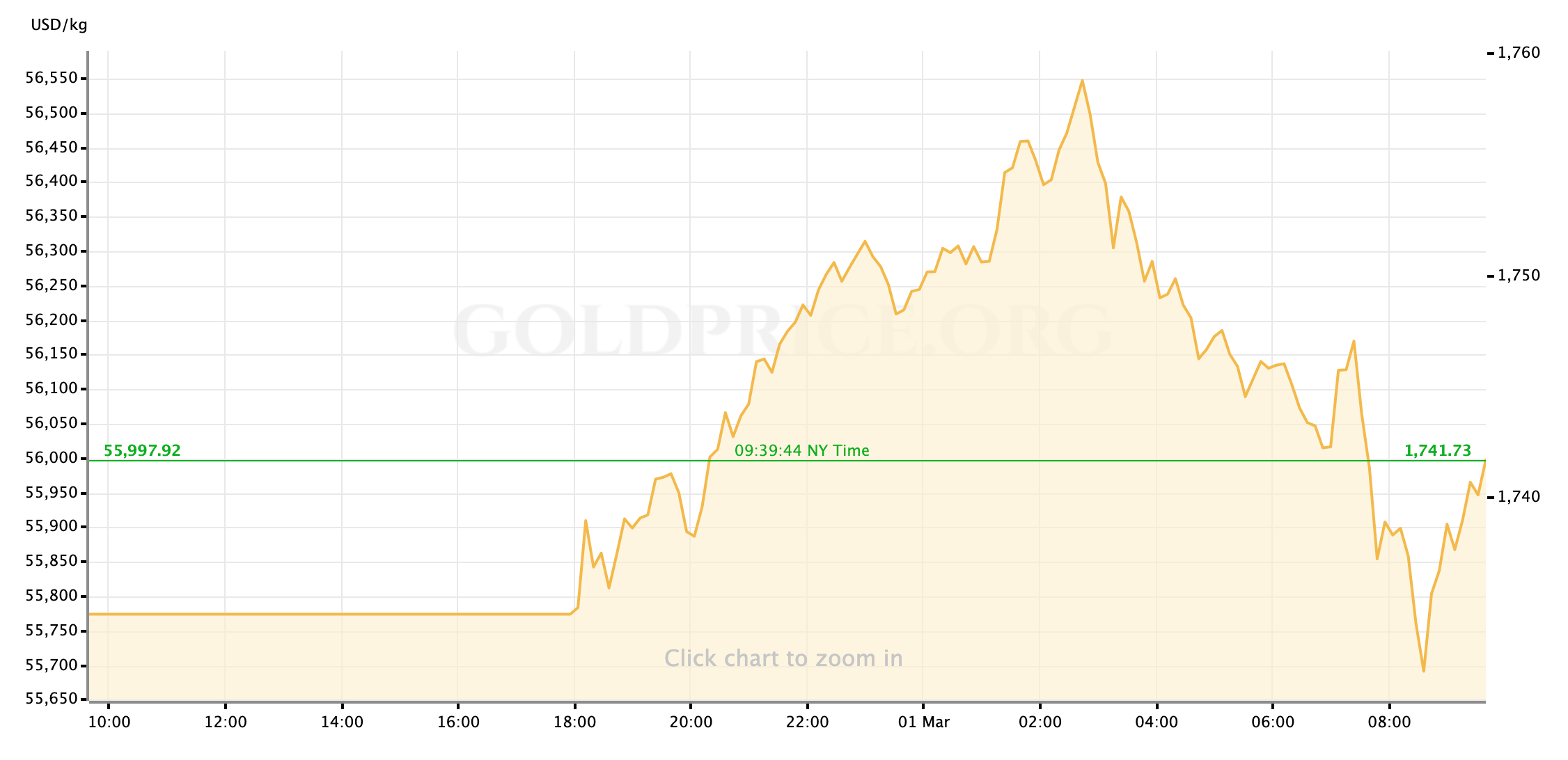

Gold prices are trading slightly higher in the spot markets just after the open of US stock markets on Monday morning. Both gold and silver were able to rally higher during overnight trading, as global bond markets have been seen to reassess the volatility of rates last week, allowing precious metals some headroom to rise along with global equities and take part in the reflation trade that is boosting the broader commodities basket.

As the US trading day has begun spinning up however, bonds markets are starting to sell with more pace again and yields on the US Treasury’s 10-year note are taking steps back towards 1.5% again. As a result, gold and silver have pared some of their overnight gains.

The action in bond markets, and it’s resulting pressure on precious metals’ efforts to participate in reflation trade as assets that may benefit from higher-inflation environments, will be closely watched this week. We’ll also be tracking the path of the Biden Administration’s covid relief package, which has passed the House and is due this week for a vote in the Senate. Passage would not only have a considerable impact in supporting the more optimistic investor forecasts for the US economy this year and next, but should also directly influence the inflation projections that have been the key driver in the recent bond market volatility.

Let’s take a week at what else is on our calendar this week.

US Economic Data to Watch

Monday, March 1 at 10am EST // ISM Manufacturing PMI (Jan)

[consensus exp.: 58.6 // prev.: 58.7]

Manufacturing activity has been a source of reliable stability in US economic data in recent months and we look for that trend to continue this week. It should provide a positive note for US equity markets to harmonize with at the start of the week, as America’s manufacturing sector has proved relatively resilient through what is hopefully the final major “wave” of the coronavirus pandemic.

Wednesday, March 3 at 815am EST // ADP Employment Report (Feb)

[consensus exp.: +180K // prev.: +174K]

The consensus among analysts and economists is that the US labor market added jobs in February at roughly the same pace as the prior month. I have to admit that February’s pretty brutal string of weekly job-loss data makes me skeptical of even holding January’s pace, to say nothing of the fact that some analyst desks are projecting pickups of nearly double the consensus number. We’ll see how it shakes out but, based on recent performance and the level of attention I expect on Friday’s NFP number, it would probably take a strong dislocation from expectations to see Dollar and gold markets meaningfully move on ADP this week.

Wednesday, March 3 at 10am EST // ISM Non-Manufacturing PMI (Jan)

[consensus exp.: 58.9 // prev.: 58.7]

While the strength in manufacturing sector activity in the US has been a good sign for the US economic outlook, it’s the service sector that a strong recovery depends on the most. Happily, the non-manufacturing PMI has been trending higher as well since last summer. There’s a possibility that poor winter weather may have affected the service sector components that are more sensitive to those conditions—particularly since so much of American’s are still dining outside-only in major metro areas—but that’s the kind of complication that I imagine is fairly priced into a January activity metric and so it shouldn’t cause a big miss below expectations. The other possibility of course is that we see a surprise to the upside which may well drive a burst of risk appetite into the markets. From Monday’s vantage point, unfortunately, it’s too early to say if that’s a turn that would boost gold-buying as part of the reflation trade or dampen its appeal in a reach for yield.

Thursday, March 4 at 830am EST // Initial Jobless Claims

[consensus exp.: +755K // prev.: +730K]

It’s become a real game of luck trying to predict, with any confidence, whether the number of weekly job losses in the US will come in above or below 800,000, particularly as we’ve seen so many lower numbers revised considerably higher the following week. Economists are calling (hoping, really) for a second fall away from 800K this week. What I think investors will be more swayed by is that fact that if initial claims do come in relatively close to expectation it will pull the 4-week average below 800K as well—a big step in the right direction for the floundering US labor market recovery.

Friday, March 5 at 830am EST // February Jobs Report

[(NFP) consensus exp.: +180K // prev.: +49K]

[(unemployment) consensus exp.: 6.4% // prev.: 6.4%]

Non-farm Payrolls reads at the start of the year are always a little noisy and tough to nail down: We’re dealing with complications from some of the toughest moths of the year, weather wise, as well as the rolling-off of seasonal hiring surges and the re-setting of hiring plans for many business and even technical adjustments to the measurements of labor market growth. This year, of course, the Covid-19 pandemic and the US’ still-nascent vaccination effort muddies the waters further. Analysts’ consensus anticipates a respectable NFP number just below 200K this month; As with Wednesday’s private payrolls data there are some notable teams calling for a much stronger rebound from January’s dismal number—their projections are based more on deep-data correlations and revisions being to the methods of measuring job growth themselves. I would expect that the market, in general, is better braced for disappointing numbers as the higher-frequency Initial Jobless Claims have been tough reading for the last month; So, there will probably be more sensitivity to a better-than-expected jobs report (risk-on) than a slight miss to the downside (risk-off.)

Fed Speak this Week

Last week, we saw multiple trading sessions where US equity markets were under a lot of pressure from the volatility in the interest rate benchmark bonds. And on those days, the US stock markets would have been in for some deep losses if not for the investor optimism that Fed Chairman Jerome Powell’s Congressional testimony sparked, with his cautiously positive read on the US economic trajectory for 2021. With bond markets this week still figuring out which way they might move and how smoothly, I think many investors may be looking to Fed commentary again as a potential life preserver; Although I’m not sure it will have the same impact, I expect the public commentary from Fed officials this week to strike largely the same tone as Powell did in Washington.

Monday: Fed Governor Lael Brainard (FOMC voter) (9am EST)

Tuesday: San Francisco Fed President Mary Daly (FOMC voter) (2pm)

Wednesday: Chicago Fed President Charles Evans (FOMC voter) (1pm)

Thursday: Fed Chairman Jerome Powell (FOMC voter) (12pm)

Friday: Atlanta Fed President Raphael Bostic (FOMC voter) (3pm)

And that’s how the week lays out ahead of us, traders. As always, I wish you all the very best of luck in your markets in the coming days, and I’ll look forward to seeing you all back here on Friday for our market-week wrap up.

Gold Price Chart

More articles from John Moncrief