Good morning traders, and welcome to our regular Monday preview of the trading week ahead, focusing on the economic data, news flow, and market narratives that may have the biggest impact on gold prices, as well as key correlated assets like the US Dollar.

Gold prices are trading relatively flat to last week’s close around 7.5 year highs, supported by a low bass hum of worry as the number of new coronavirus infections-- especially in the US-- continues to move higher. This week’s markets are shortened by a day due to the US Independence holiday weekend, which means that the monthly jobs report will come one day earlier. It’s also adding to a general sense of uncertainty as the week begins as traders and analysts try to get their footing in economic conditions that are starting to shift again.

Let’s look at what the week has in store for us.

US Economic Data to Watch

Tuesday, June 30 at 9am EDT // Case-Shiller Home Price Index (Apr)

[consensus exp.: +4% YoY // prev.: +3.9%]

Most economists seem to be expecting the price growth for housing in major US cities to have continued growing at pace through April despite the negative housing market data we’ve already seen for that month (and the next.) That leads me to believe there is some real downside risk to the consensus, and depending on how US equity markets get out of the gate on Monday, there may be some extra sensitivity to a downside miss; it could be another pressure point that sends investors into safer positions like gold.

Wednesday, July 1 at 8:15am EDT // ADP Employment Report (June)

[consensus exp.: +2,950k // prev.: -2,760k]

After last month’s surprising improvement in labor market data for May and following slowing (if plateauing) initial jobless claims this month, analysts are expecting to see ADP’s tally of private payrolls already showing jobs added on net in June after three months of losses. It’s not a prediction that “feels” right when you look at the real world around the data, but at the same time the unexpected resurgence in labor market data has been a steam roller that I don’t want to get caught in front of. Depending on how the week starts for markets this could be a big boost to risk appetite, pushing the equity bull run even further out onto a limb. Conversely, a miss to the downside-- specifically a negative print-- could not only disappoint investors in the immediate term but may also shake investors into believing that last month’s blue-ribbon improvement was just a fluke. Though this kind of ugly would most likely push markets into deep risk aversion from which gold prices would benefit, I think it would be a big enough shock that the yellow metal’s upside would be capped by the Dollar surging higher as investors flee directly into cash.

Wednesday, July 1 at 10am EDT // ISM Manufacturing PMI (June)

[consensus exp.: 49.5 // prev.: 43.1]

The preferred metric for manufacturing sector activity in the US economy is tipped to continue its rebound this month, possibly pulling within a single point of the 50.0 “breakeven” above which the report signals expansion in the sector rather than the contraction that has characterized 2020. Any improvement from last month is likely to be received calmly by markets, I think, but a print above 50 may put a dent in the chart for gold and other safe havens.

Wednesday, July 1 at 2pm EDT // FOMC Discussion Minutes

Because we got such a torrent of information and data from the last FOMC meeting and the updated economic projections that came with it, there’s not a lot of mystery to digging through that meeting’s minutes and notes. With a firm idea of the committee’s outlook and thresholds, the focus this time around will be on finding what kind of discussion was had around more unconventional, still unused tools in the Fed’s kit. Specifically: various forms of yield curve control, or even negative interest rates.

Thursday, July 2 at 8:30am EDT // June Jobs Report

[(non-farm payrolls) consensus exp.: +3,000k // prev.: +2,509k]

[(unemployment rate) consensus exp.: 12.4% // prev.: 13.3%]

Last month’s 2.5 million+ jobs gained was an all-time record, and one that is expected to be topped for the month of June. From that perspective the outlook for June’s NFP data and the risks to it are broadly the same as for Wednesday's ADP numbers. The table is set for equity markets to get another strong boost to their rising rally that still feels unconnected from daily economic life in America, and that means that the risk of a miss to the downside would bring along a volatile swing to risk-off positions. Again, gold would certainly stand to gain from that kind of move (just as it will be under pressure if an as-expected NFP print sends stocks to new records,) but it would likely play second fiddle to a ripping US Dollar.

As usual, the unemployment rate stands to get much less attention this month. Shifts in the wonky mechanics of calculating unemployment to different precisions means that even as the nominal number of jobs added will make a big step forward the improvement in overall unemployment will be less spectacular. Sadly, I expect that markets are going to start treating a jobless rate over 10% as par for the course through the end of 2020, so I’m not expecting markets to move much on the headline rate alone.

Thursday, July 2 at 8:30am EDT // Initial Jobless Claims

[consensus exp.: +1,336k // prev.: +1,480k]

Economists are hoping that this time we’ll see the number of new weekly jobless claims drop farther away from a pace of 1.5 million. With the Independence Day weekend pushing the Jobs Report to the same slot as jobless claims, we’re not going to see much market movement one way or the other than can be attributed to the weekly labor market numbers, but it remains useful for tracking the longer-term trends.

FedSpeak this Week

The center of the Federal Reserve’s communication calendar for this week is Wednesday’s release of the meeting minutes for June’s FOMC, but there are also a few notable public appearances from key members including the Chairman’s joint testimony before congress, on Tuesday. Last week’s FedSpeak was characterized by warnings that continued failure to curtail the spread of Covid-19 in the US poses a dramatic risk to any economic recovery (as would Congressional unwillingness to add more fiscal stimulus measures,) mixed with assurances that the Fed is ready and able to provide the necessary monetary support. We’re generally looking for the same rhetoric this week.

Tuesday, June 30: New York Fed President John Williams (FOMC voter) (11am EDT); Federal Reserve Chairman Jerome Powell testifies before the House Financial Services Committee (FOMC voter) (12:30pm); Minneapolis Fed President Neel Kashkari (FOMC voter) (2pm)

Wednesday, July 1: Chicago Fed President Charles Evans (non-voter) (10am)

And that’s how this holiday-shortened week lays out in front of us. As always, I wish you the very best of luck in your markets this week!

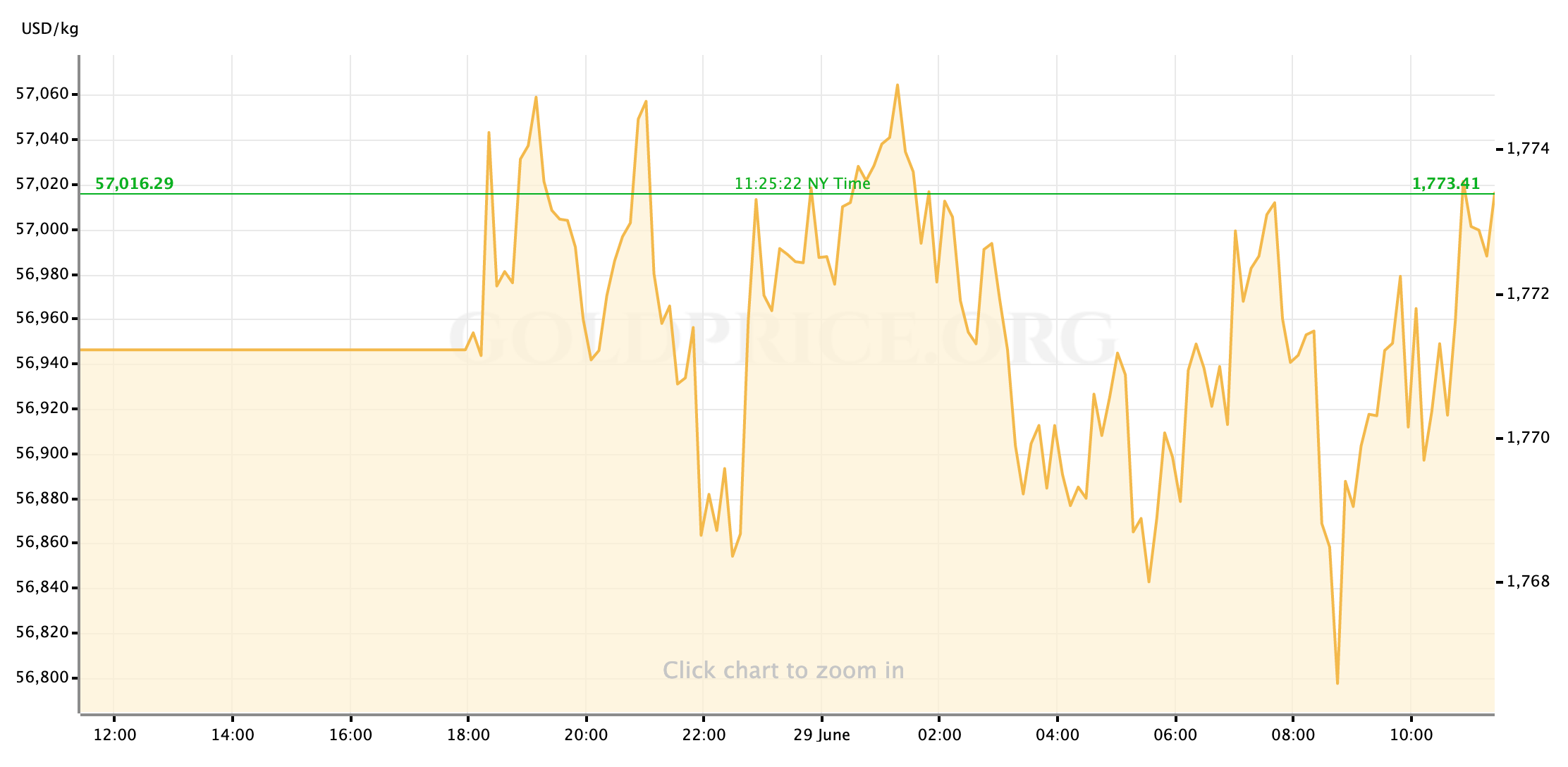

Gold Price Chart

More articles from John Moncrief