Happy Monday, traders. Welcome back from an excellent football weekend.

Spot price for gold is back above $1290/oz this morning, showing strong resistance at that level after fading in the early New York sessions from highs north of $1295 that we reached in overnight trading. That bid in gold price has largely been attributed to another round of weak economic data coming out of China, this time focused on trade. It seems like there aren’t any other market-watchers out there who will buy my argument that risk-off assets are richer this morning because of global unease with the growing possibility of the Patriots returning to the Super Bowl.

Silver begins the weak roughly where we left it, trading around $15.60/oz.

The US economic calendar is light this week, made lighter by the now record-long government shutdown (otherwise we would have retail sales data on Wednesday.) While things are a bit quiet on American shores however, London has a real doozy for us on Tuesday.

US Economic Data to Watch

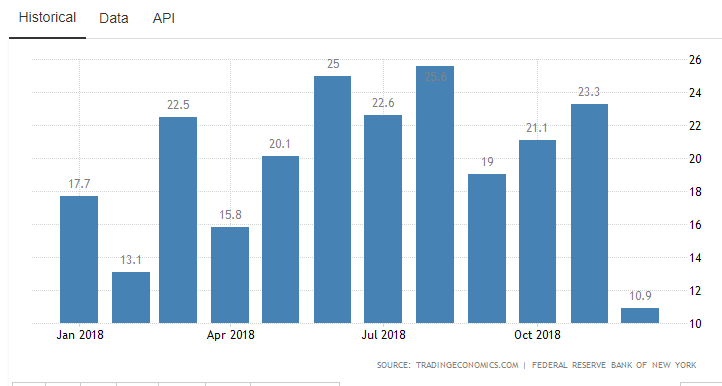

Tuesday, January 15 at 8:30am EST // Empire State Manufacturing Index

[consensus expectation: 11.3 // previous: 10.9]

The NY Empire State index is not a manufacturing read that I typically focus on, personally; but December’s data was a particularly wide disappointment to the downside based on expectations as well as trend:

Between this, the December softening in ISM manufacturing data and the general weakness of recent US economic inputs I’ll be interested to see how this month’s data shakes out and what the reaction of risk-off assets like gold will be.

Tuesday, January 15 at 8:30am EST // PPI

[consensus exp.: -0.1% // prev.: +0.1%]

Producer inflation is expected to show a month-to-month decline for December, but as long as it’s within touching distance of the -0.1% consensus there shouldn’t be much of a reaction as the analysts’ prediction is predicated on strong core prices being offset by the major decline in US energy prices.

Thursday, January 17 at 8:30am EST // Initial Jobless Claims

[consensus exp.: 220k // prev.: 216k]

Expecting the pace and trend of new unemployment claims to continue this week.

Thursday, January 17 at 8:30am EST // Housing Starts

[consensus exp.: flat // prev.: +3.2%]

The fact that we had a pretty mild December in terms of wintery weather tips the risk towards this upside of this month’s New Housing Starts number. I’m particularly interested in this, from Goldman Sachs’ note, which indicates we may be heading for some sustained weakness in housing data to start 2019:

“Over the next few quarters, we expect higher interest rates and tax reform to continue to weigh on homebuilding.”

Friday, January 18 at 8:30am EST // U. of Michigan Consumer Sentiment

[consensus exp.: 96.6 // prev.: 98.3]

As more and more US economic data that reports hard numbers (inflation, housing data, and GDP for example) begins to weaken, it will become more important to keep an eye on “softer” data like assessments of sentiment and current or forward-looking confidence in the state of things. To that point, the University of Michigan’s index is expected to decline a bit in January.

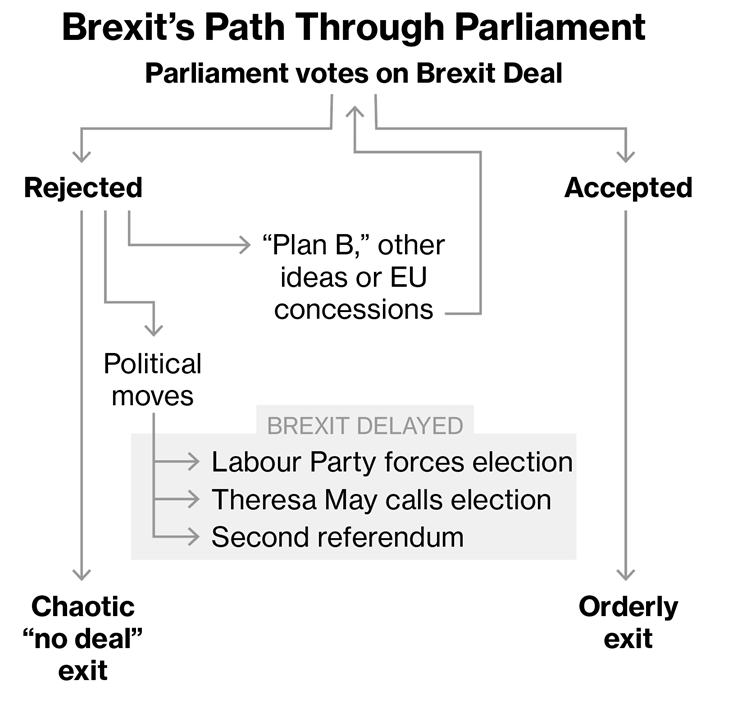

The UK’s “Meaningful” Brexit Vote – Tuesday, January 15

Yes, there is other semi-impactful economic data being released from other developed economies this week: German inflation on Wednesday, for one; Japanese inflation on Thursday night for another. But it’s very difficult to look around the looming vote on Tuesday afternoon (EST.)

If the Brexit agreement that Theresa May and her team have spent 18 months negotiating with the EU fails to pass with approval from the British House of Commons on Tuesday—and it is expected to fail, by a wide margin—we take another step into unknown territory. From that point, the possible next steps range from an extension of the March 29 Brexit deadline, to the UK leaving the union with no deal of any kind in place, to a general election in Britain and new government in power. Bloomberg’s Brexit team lays the possibilities out like this:

To editorialize a bit, I think it’s pretty generous to only characterize the “no deal” outcome as “chaotic”—I would argue that chaos is already here.

As much noise as there is in US Dollar trading at the moment, I don’t particularly expect that trade-related intricacies and GBP-based repercussions of the different possible scenarios to bear much weight on the greenback or gold markets in the near-term. At least not enough to warrant close inspection from precious metals traders. Instead, I’ve taken the time here to mention the possible outcomes because I expect there will be a noticeable move in risk appetite when the result of the final vote is announced: I believe investors will move farther into safe-haven assets—specifically gold and the Yen—if the expected defeat is dealt to Prime Minister May, or else those same risk-off positions will be markedly reduced in the event of an 11th hour rescue. Additionally, at least having an idea of the possible answers to “what’s next?” following a failed vote will allow you to interpret any market action in the near term.

And that’s where I’ll leave you for this Monday. I, for one, am always excited to see what happens. I also wish you all some happy dealing and the best of luck this week, traders. I’ll see you back here on Friday for a deeper recap of the week’s market happenings.

Gold Price Chart

More articles from John Moncrief