Good morning, traders; Welcome to our market week preview, where we take a look at the economic data, market news and headlines likely to have the biggest impact the price of gold this week and beyond, as well as market prices for silver, the US Dollar, and other key correlated assets.

Gold prices are moving strongly higher this morning, having retaken the important psychological price level of $1800/oz in the spot market shortly after US equity markets opened the week on the back foot.

The yellow metal’s Monday rally has been driven in large part by a market-wide effort to position for meaningfully higher inflation in the long- (or possibly medium-term.) Last week’s bond sell-off has continued, with the benchmark 10-year still finding momentum above 1.3% and, at times, threatening a move to 1.4%. Even as the start of cash trading in the US has seen a slight rebound in bonds, gold prices have continued to benefit from the prevailing market mood while equities and the US Dollar have weakened.

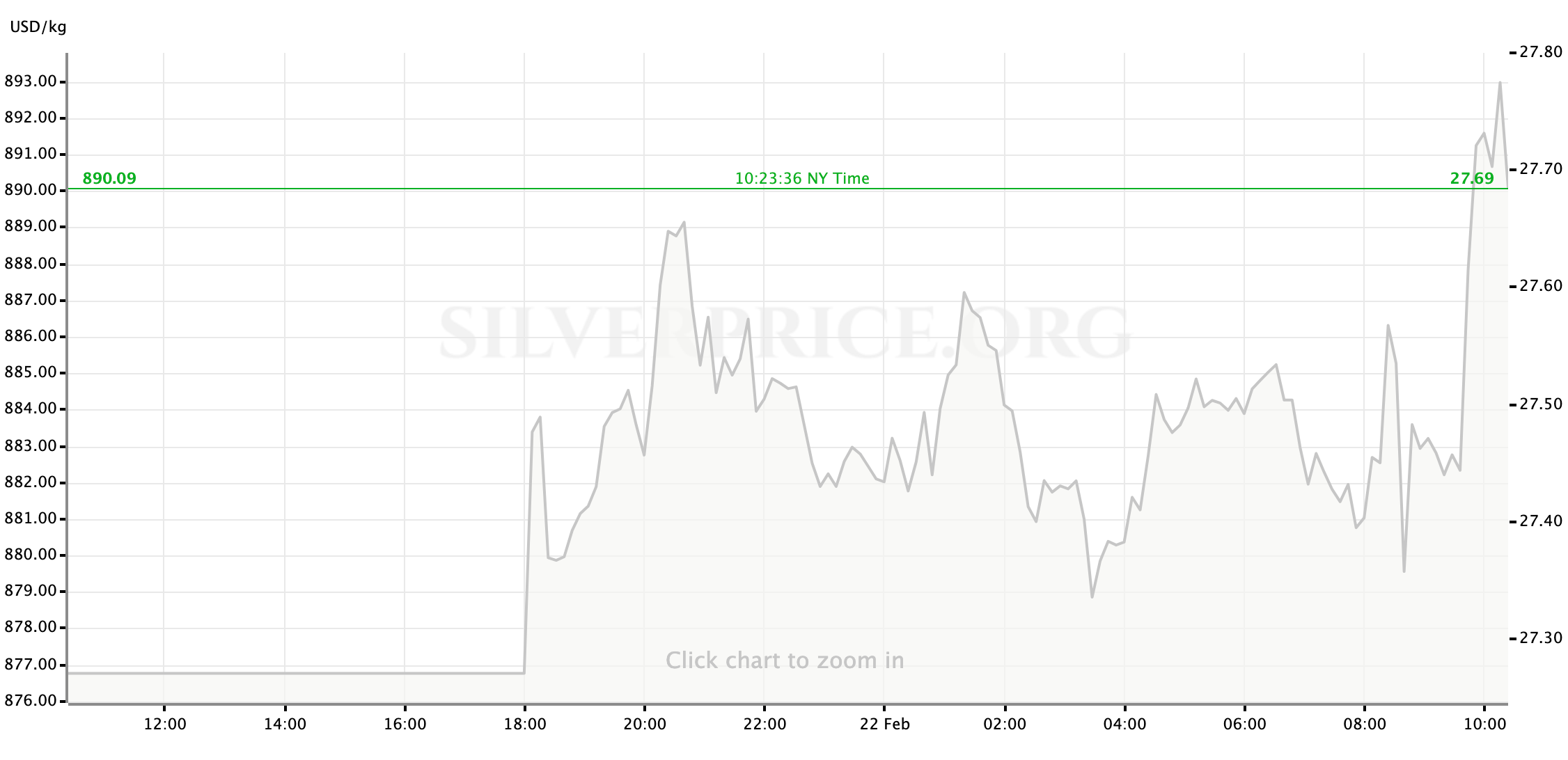

Silver is of course starting the week strong as well, consolidating above $27.50/oz at the time of writing

This week’s data calendar is fairly light, and weighted on Thursday and Friday. Our main focus for the first half of the week (really, most likely, the whole) will be the path towards passage of the Biden Administration’s covid relief bill and wrangling about what size and shape it will ultimately take.

Let’s look at the data ahead.

US Economic Data to Watch

Thursday, February 25 at 830am EST // Initial Jobless Claims

[consensus exp.: +840K // prev.: +861K]

Economists seem to have given up on calling for a much-needed drop below a weekly pace of 800,000 new unemployment claims within the American labor market, after much of February has seen even those weekly reads that fell below 800K later revised worryingly higher. It’s hard to say if the market’s risk-appetite has any sensitivity to this after the jobs recovery has been stagnant at best since the start of the year, but another historically high rate of job losses will certainly point to a very ugly number on next week’s February Jobs Report which likely will push traders away from the table and into safe havens.

Thursday, February 25 at 830am EST // Durable Goods Orders (Jan)

[consensus exp.: +1.1% MoM // prev.: +1.3%]

At this point in the path between pandemic and recovery, monthly Durable Goods data is becoming an important marker for the health of the US manufacturing sector. During this “third wave” of the Coivd-19 pandemic that has recently crossed the 1-year mark (or is about to, depending on your signpost,) industrial activity has remained more resilient than before; January’s data set is expected to confirm that view. Significantly, analysts expect to see the steady pace of growth buoyed mostly by strength in the core groups.

Friday, February 26 at 830am EST // PCE Price Index (Jan)

[(core) consensus exp.: +1.4% YoY // prev.: +1.45%]

[(headline) consensus exp.: +1.4% YoY // prev.: +1.28%]

The Federal Reserve’s own tracker for consumer prices in the US is expected to estimate the same annual rate of inflation as the CPI did two weeks back, roughly 1.4% for both the headline number and the less-volatile “core” number. So, teams, though, perhaps in light of last week’s data showing that the most recent round of direct stimulus checks to US consumers made a sizeable impact on January’s Retail Sales, are projecting a slight acceleration in inflation. If this morning’s heavily favored “reflation” trade is still moving at the same pace on Friday, I’m not sure that even concrete numbers showing that price growth isn’t getting “hot” anytime soon will slow the flight to assets expected to perform well alongside rising inflation (which, for now, seems to include gold and silver) as the CPI data certainly doesn’t appear to have had that effect.

Friday, February 26 at 830am EST // Personal Income & Spending (Jan)

[(income) consensus exp.: +9.5% MoM // prev.: +0.6%]

[(spending) consensus exp.: +2.4% MoM // prev.: -0.2%]

The same thrust that propelled Retail Sales last month to one of the biggest month-to-month jumps on record—the “helicopter money” dispersed to US consumers at the start of the year—should be felt similarly in the month’s Income & Spending data. Given how much of the stimulus cash was injected right back into the economy rather than being saved, as suggested by the Retail Sales data, I wouldn’t be surprised to see a higher Personal/Household Spending number. Either way, if the signal isn’t muddled by an unexpected dip in the PCE inflation data, I expect at least a brief spike in risk-appetite when these numbers hit the wire.

FedSpeak This Week

Chairman Jerome Powell will be the main draw this week on the FOMC participants’ public schedule, as he delivers his regular Congressional testimony to the Senate Banking Committee (on Tuesday) and then it’s counterpart in the House (on Wednesday.) Powell has proven adept over the years at offering well-crafted and patient responses to most representatives’ questions, and we’re already very clear on Powell (and the FOMC’s as a whole) position on the next steps that are needed to drive a US economic recovery; So we know not to expect any fireworks that will really shift any market valuations beyond a few algo trades. However, this will be Powell’s first time offering testimony to a newly configured congress so we could be in for some grandstanding from new committee members which would at least provide some entertainment. Alongside Powell’s appointments at the Capitol, here are some other FOMC appearances this week worth noting.

Tuesday: Fed Chair Powell (FOMC voter) (10am EST)

Wednesday: Fed Chair Powell (10am); Fed Governor Lael Brainard (FOMC voter) (1030am); Fed Vice Chair Richard Clarida (FOMC voter) (1pm)

Thursday: Atlanta Fed President Raphael Bostic (FOMC voter) (830am); St. Louis Fed President James Bullard (non-voter) (1030am)

And that’s how the week lays out ahead of us, traders. As always, I wish you all the very best of luck in your markets in the coming days, and I’ll look forward to seeing you all back here on Friday for our market-week wrap up.

Gold Price Chart

More articles from John Moncrief