Good morning, traders; Welcome to our market week preview, where we take a look at the economic data, market news and headlines likely to have the biggest impact the price of gold this week and beyond, as well as market prices for silver, the US Dollar, and other key correlated assets.

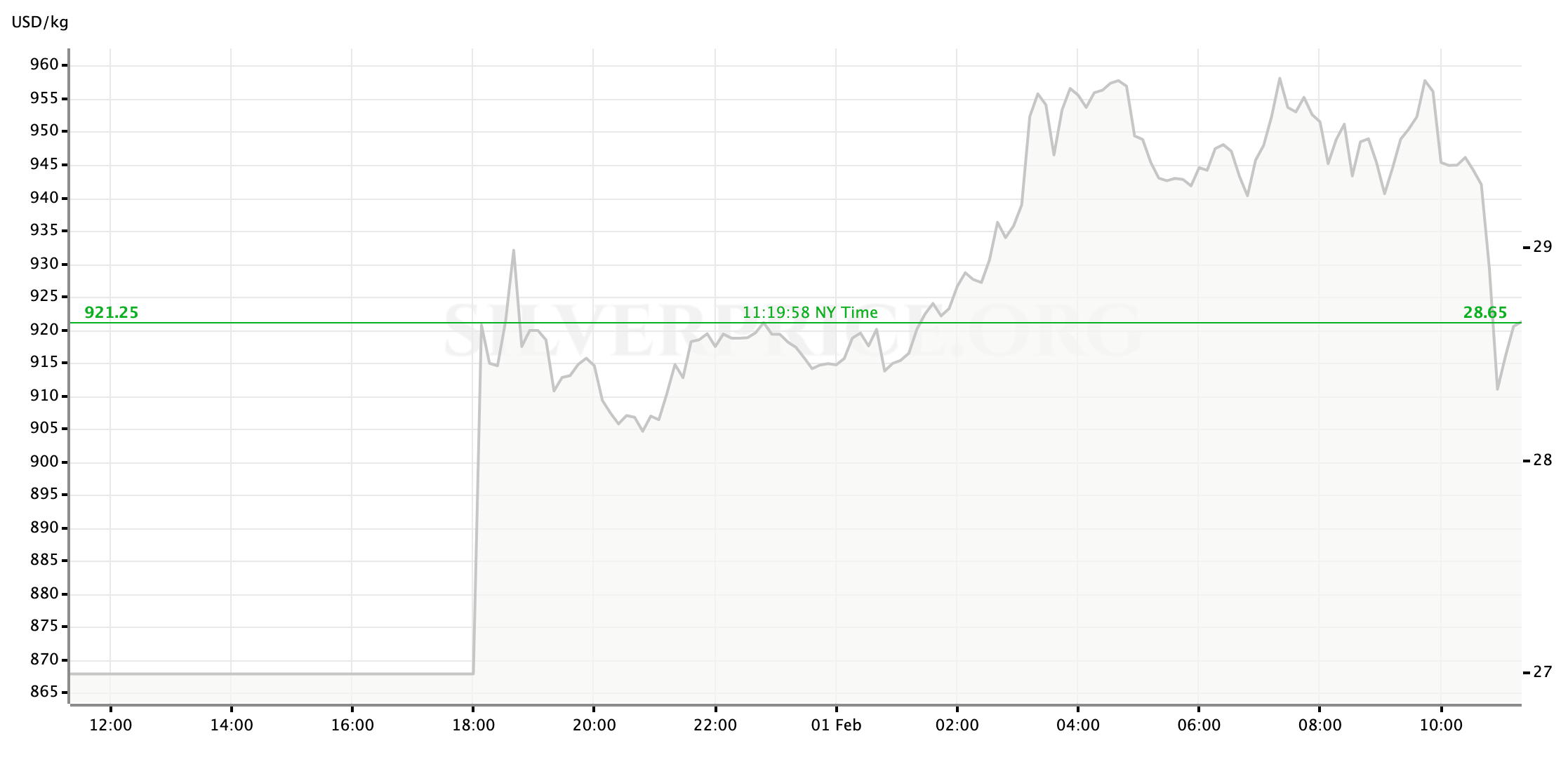

Gold prices are solidly higher this morning, dragged higher on the coat tails of an unstable surge in silver prices that saw volatile gaps higher for both precious metals. The Reddit-based, crowd sourced run on targeted financial assets appears to have moved over the weekend, from a handful of stock ticker symbols with extraordinarily high short interest to a play on silver, which the mass of pseudo-activist retail investors believe is being over-shorted by Wall Street’s biggest banks. The fleury of silver buying over the weekend, with markets closed (and futures contracts being tougher to access for at-home traders anyway,) was focused in physical bullion but the resulting implied shortfall in supply has been driving the spot and futures markets higher since the Sunday evening reopen. Silver rocketed higher in a gap at the start of trading, to just below $28.40/oz—a premium of more than 5% above last week’s close. Momentum carried the white metal on higher during overseas trading before eventually meeting resistance at $30. In the hour since US cash trading has begun, a heavier flow of trading has corrected the price down closer the initial pop at $28.60.

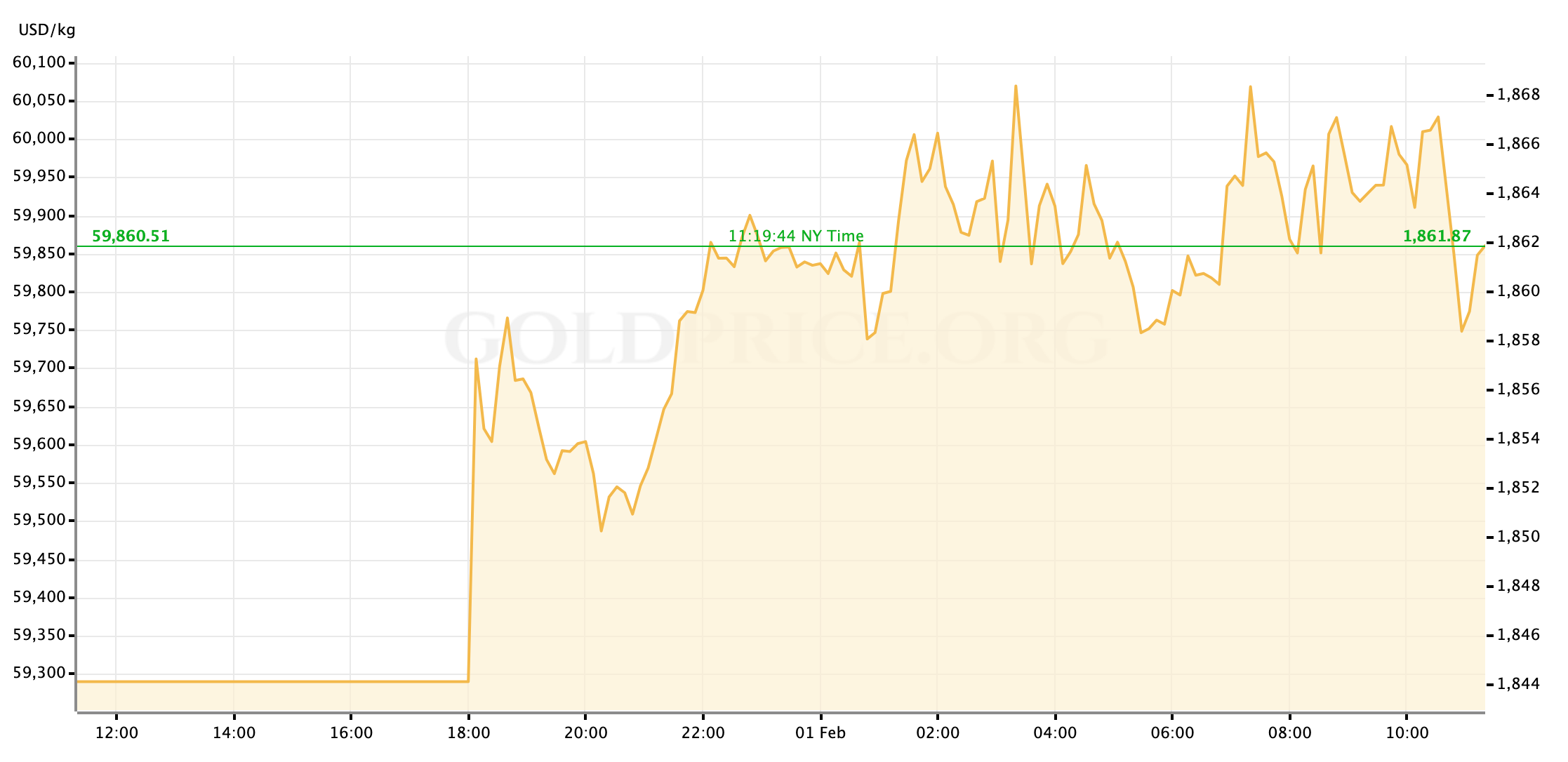

Gold has mostly been along for the ride this morning, rising in tandem with silver and correcting lower in roughly the same steps. The yellow metal marked and overnight high at $1870/oz in spot trading and has reeled back to the $1860 range under the direction of the US trading session.

This populist pivot from undervalued stocks into commodities markets is sure to run the headlines for Monday, but I suspect that WSB crowd will find it considerably more difficult to make consistent waves in a dramatically different type of market from US equities. We’ll track the story this week to be sure, but I won’t be surprised if this branch of it tails off by midweek.

In other news, the US Congress looks to be digging in for probably long-lasting negotiations around the next round of desperately needed fiscal stimulus; And with the daily pace of coronavirus hospitalizations and deaths starting to decline, investors along with the rest of the world will be watching to see if those in charge can take advantage of a break in the clouds to accelerate vaccination and containment efforts.

On the data front, we’re gearing up for the January Jobs Report, due Friday. We’ll also get updates on the pace of manufacturing and service sector activity expansion. Let’s take a look ahead.

US Economic Data to Watch

Monday, February 1 at 10am EST // ISM Manufacturing PMI (Jan)

[consensus exp.: 60.0 // prev.: 60.5]

The rebound in manufacturing activity since last spring’s pandemic lockdowns seems to be leveling-off as lifted restrictions were rolled-back before the holidays, but holding pace around a PMI of 60 isn’t too shabby. In fact, it’s near enough to the highest mark we’ve seen since late 2018. Many analysts expect that US manufacturing will experience less of a slowdown from the third wave (or whichever we’re on now) of the coronavirus pandemic as economic restrictions aren’t severe enough this time to choke the demand for industrial activity; Other recent data points, including last week’s look at December manufacturing from Markit, support that outlook. An as expected print would traditionally be a buy signal for equities, but as we don’t yet know what level of volatility we’ll find in US stocks to begin the week that’s a hard one to guarantee ahead of time. I’ll also be curious to see if this morning’s speculative spike in prices has eaten up any lift that silver, whose demand is more sensitive to industrial activity, will get out of a positive report.

Wednesday, February 3 at 815am EST // ADP Employment Report (Jan)

[consensus exp.: +70K // prev.: -123K]

While some degree of rebound from last month’s disappointing contraction in private payroll jobs is fair to expect, I still think the risk is skewed to the downside of the consensus projection for January; Many other analysts are saying the same, particularly as weekly jobless claims have remained historically high. Continuing shakiness in the US labor market is probably accounted for in asset prices for the most part, but another letdown in the monthly data is still likely to push investors and managers into a risk-off position and benefit the key safe havens: the Dollar, gold, or possibly both.

Wednesday, February 3 at 10am EST // ISM Non-Manufacturing PMI (Jan)

[consensus exp.: 56.7 // prev.: 57.2]

In contrast to Monday’s read on the manufacturing sector, activity in the services sector is expected pullback a bit this month. The service sector is obviously being much harder-hit by quarantine travel bans and stay-at-home orders, but doubly unfortunately is also the more key sector to the US economy in the current cycle. Still, while a slowdown from December will be unwanted, the current level (and the consensus projection for January) remains in the mid-line of the last five years’ trend; Because of that, I don’t see a slight pullback as being a real threat to the current prevailing outlooks for an economic rebound in 2021.

Thursday, February 4 at 830am EST // Initial Jobless Claims

[consensus exp.: +830K // prev.: +847K]

Economists and analysts are looking (hoping?) for the recent slowdown in initial jobless claims to continue, uninspiring as it may be. This weekly data is usually brushed aside during the week of the big monthly Jobs Report, but Thursday’s number can impact that market reaction to Friday’s NFP: for instance, an unexpected uptick in new unemployment claims can accelerate the market’s risk-averse reaction to a weaker payrolls number.

Friday, February 5 at 830am EST // January Jobs Report

[(NFP) consensus exp.: +58K // prev.: -140K]

[(unemployment) consensus exp.: 6.7% // prev.: 6.7%]

My impression, subject to change over the next four days of trading, is that Friday’s labor market update will be a bullish signal for the US Dollar (and possibly a sell for gold) in any event, barring a truly surprising consecutive month of jobs lost in the US labor market. A muted gain in jobs for the month, which is the consensus pick,, seems likely to at least hold the Greenback steady where (again, depending on how the bulk of this week’s trading goes) it can consolidate before possibly rising higher next week; An outperformance against the consensus expectation, which some major desks like Goldman Sachs’ are projecting, probably allows the Dollar more room to run as expectations for the level of fiscal super-spending needed in the first half of 2021 may be adjusted lower. Even a mild disappointment in the data, as things currently stand, will see investors reaching for safety opt for US Dollar cash which, as we pointed out last Friday, seems to have become the dominant safe haven play once again.

FedSpeak this Week

The full schedule of Fed officials’ public appearances is pretty busy this week, as is often the case immediately following an FOMC meeting. The list of scheduled remarks that might carry some market impact however is much lighter. Officials will likely carry on as we saw them at the end of 2020: walking this line of clarifying the need for meaningful stimulus from the fiscal side to support the US economy while not injecting real uncertainty into markets.

Monday: Minneapolis Fed President Neel Kashkari (non-voter) (12pm EST)

Wednesday: St. Louis Fed President James Bullard (non-voter (1pm); Chicago Fed President Charles Evans (5pm)

And that’s how the week lays out ahead of us, traders. As always, I wish you all the very best of luck in your markets in the coming days, and I’ll look forward to seeing you all back here on Friday for our market-week wrap up.

Gold Price Chart

More articles from John Moncrief