Good morning, traders; Welcome to our market week preview, where we take a look at the economic data, market news and headlines likely to have the biggest impact the price of gold this week and beyond, as well as market prices for silver, the US Dollar, and other key correlated assets.

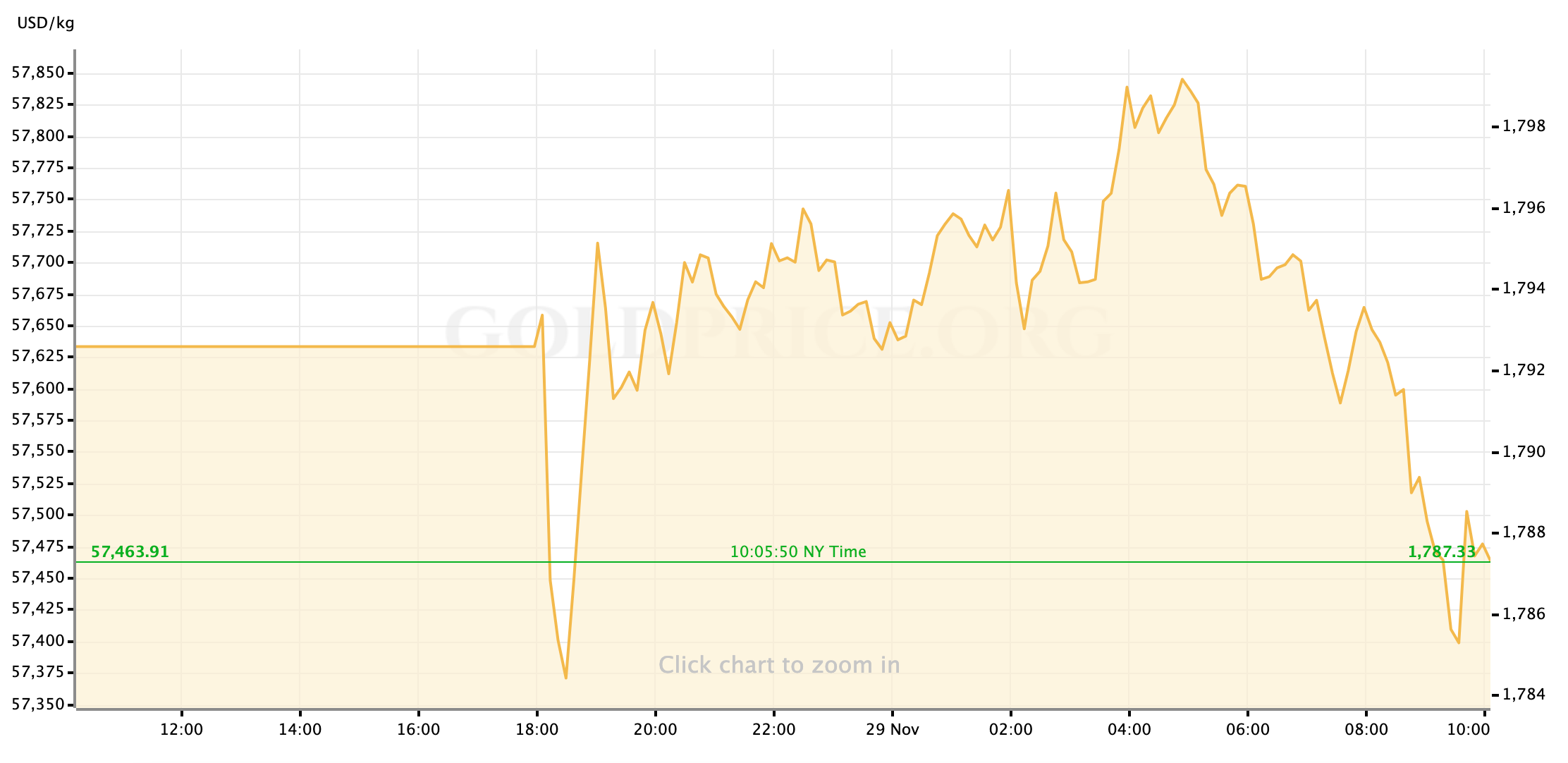

Gold prices are down slightly from Sunday evening’s start, after a somewhat volatile overnight session. Global markets have started the weak by cautiously unwinding some of the risk-off swing that roiled financial markets so thoroughly on Friday. The strongest tailwind for gold prices as been the resulting rebound in Treasury yields.

Despite the weak start to trading, there will be plenty of opportunities for gold to find some legs this week, with a major monthly Jobs Report due Friday and a strong slate of FedSpeak. Of course, financial markets will also be closely watching developments in the narrative around the new “omicron variant” of Covid; specifically, how quickly it might spread and how effective current vaccine protocols may or may not be against it.

For now, let’s take a look at the rest of the calendar ahead.

US Economic Data to Watch

Wednesday, December 1 at 815am EST // ADP Employment Report (Nov)

[consensus est.: +525K // prev.: +571K]

The number of private payroll jobs added in the US economy, as provided by ADP, should continue to be a possible point of some market volatility for as long as traders and investors are closely tracking the labor market recovery; It may not be a reliable tool to project what Friday’s Job Report will look like, but for those managing positions in gold (or other US Dollars-sensitive assets,) there’s always a possibility that a print above or below expectation will see a knee-jerk reaction in the charts.

Wednesday, December 1 at 10am EST // ISM Mfg. Index (Nov)

[consensus est.: 61.1 // prev.: 60.8]

Survey data on manufacturing activity and retail spending from the month of October demonstrated that both producers and consumers in the broader US economy were undaunted by overall price inflation not only persisting at 2021’s elevated levels, but unexpectedly moving higher. With Wednesday’s ISM read on industrial activity nationwide we’ll get our first chance to look at November through the same lens. Expectations are that manufacturing has carried on at a similarly healthy clip, and there’s little reason to suspect a miss here. Be aware, though: with the worries of a new Covid variant and/or a winter surge in infections still on investors’ minds from late last week, a disappointing PMI number might see a more aggressive risk-off reaction that we’d otherwise expect. At that point, it would be a question of whether such a swing pushed investors into gold as a safe haven, or into cash positions at the expense of all else.

Thursday, December 2 at 830am EST // Initial Jobless Claims

[consensus est.: +250K // prev.: +199K]

Last week’s initial claims number unexpectedly fell below 200,000 to set the lowest mark in several decades. This week, markets will want to see how much of a snap-back the number experiences (revisions of last week’s print are possible as well.) The November Jobs Report due on Friday will almost certainly overshadow this weekly data, as it will most other numbers this week.

Friday, December 3 at 830am EST // November Jobs Report

[(NFP) consensus est.: +535K // prev.: +531K]

[(unemployment rate) consensus est.: 4.5% // prev.: 4.6%]

Across the board, most data we’ve seen for the month of November suggests that Friday should see another healthy number of new jobs “added” in the US economy for the month, continuing October’s trend towards improvement after the late-summer’s data had worried investors that the US labor market recovery was getting shaky. There are also signals that prior months’ numbers might be revised higher. There’s likely not much chance of a strong market reaction to a (reasonable) upside surprise on this one, but a big jump might see investors react similarly to October’s CPI lift; That is, positioning for an earlier rate hike. As with Wednesday’s manufacturing PMI, the worried mood of markets that pervaded last Friday may linger through this week and could magnify any risk-off reactions to missed expectations of major data like the NFP.

Friday, December 3 at 830am EST // ISM Services Index (Nov)

[consensus est.: 65.0 // prev.: 66.7]

Everything said above about ISM’s data on the manufacturing sector neatly applies to the service sector-focused version of the survey, too, with a couple small differences: Service sector expansion has been hotter in recent months than industrial, meaning that there’s more cushion before a lower number on Friday would be termed “disappointing”; and investors and managers may well be tired from a busy week come late Friday morning, so the overall market reaction to anything above or below expectation is likely going to be muted.

FedSpeak this Week

This week’s calendar of public appearances from FOMC officials is a crowded one, and includes a couple congressional appearances by Fed Chair Jerome Powell which will attract a little more scrutiny than usual ahead of the confirmation process now that we know the White House will nominate Powell to remain in place for another term. Analysts and Fed watchers will also be on the lookout for more color around how sensitive the FOMC may be to macroeconomic (or more global) shifts compelling adjustments to the schedule of the current taper to either move faster (in the case of strong and persistent inflation numbers) or hit the brakes (concerns around a winter Covid surge.)

Monday: Fed Chair Jerome Powell (FOMC voter) & New York Fed President John Williams (FOMC voter) (3pm EST)

Tuesday: Fed Chair Powell & Treasury Sec. Janet Yellen (10am); Fed Vice Chair Richard Clarida (FOMC voter) & Cleveland Fed President Loretta Mester (non-voter) (2pm)

Wednesday: Fed Chair Powell & Treasury Sec. Yellen (10am)

Thursday: Atlanta Fed President Raphael Bostic (FOMC voter) (830am); Fed Governor Randal Quarles (FOMC voter) (11am); Atlanta Fed President Bostic (1130am); San Francisco Fed President Mary Daly (FOMC voter) & Richmond Fed President Thomas Barkin (FOMC voter) (1130am)

And that’s how the week lays out ahead of us, traders. As always, I wish you all the very best of luck in your markets in the coming days, and I’ll look forward to seeing you all back here on Friday for our market-week wrap up.

Gold Price Chart

More articles from John Moncrief