Happy Friday, traders. Welcome to our weekly market wrap, where we take a look back at these last five trading days with a focus on the market news, economic data and headlines that had the most impact on gold prices—and may continue to into the future—as well as the charts for silver, the US Dollar and other key correlated assets.

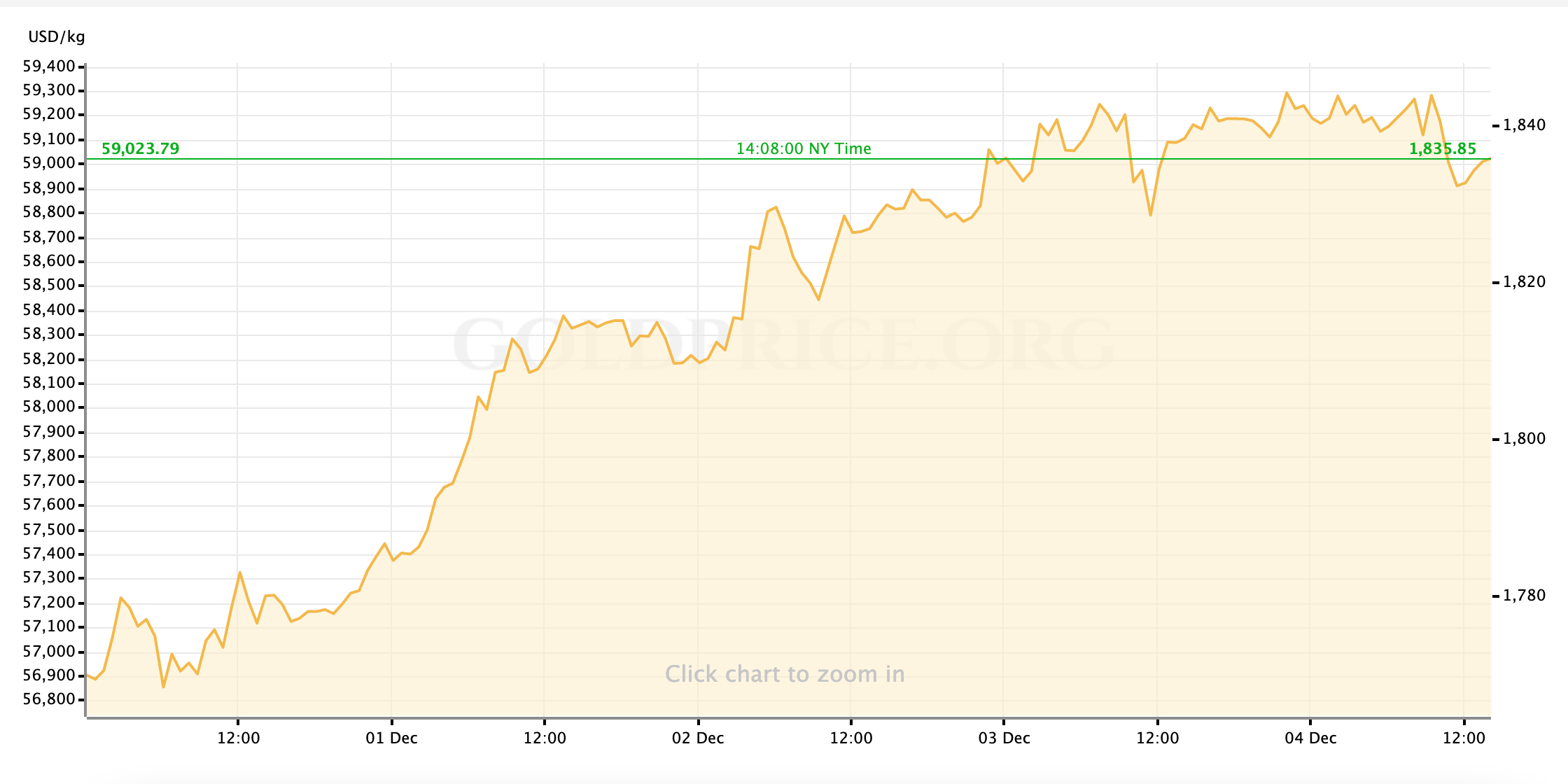

Gold prices are significantly higher and showing healthy consolidation in the spot markets at $1835/oz on Friday afternoon.

This caps of a strong week of gains for the yellow metal, as well as silver, as a general expectation of improvement and growth in the US economy in 2021 despite the current Covid-19 pandemic persisting (and, indeed, worsening) has bread a market environment in which optimists can continue to buy up the stock market while pessimists can take advantage of gold as a recently “cheap” safety play.

So, what kind of week has it been?

Gold Prices Began a Steady Climb Up from Multi-Month Lows to Begin December Trading

For a week that has seen gold’s spot price flip a major psychological level ($1800/oz) from resistance to support on the way to gaining roughly $50/oz in value, this trading week was surprisingly orderly and consistent. The yellow metal, and silver as well, had fallen a bit farther to start the week ahead of the first US trading session on Monday, but the market-wide reshuffling of positions that always takes place on the final trading day of a month saw US stocks pull back a bit, although equities still turned in a record-breaking November; The easing of pressure on “safer” assets allowed gold prices to move back off the floor and consolidate back around $1780/oz by the end of Monday’s trading, coming roughly $12/oz off of recent lows.

Gold’s breakout rolled through the Tuesday and Wednesday market sessions. The spot chart climbed above $1800/oz in the early morning hours of Tuesday and pretty quickly found new buyers and new momentum from there. Also on Tuesday morning, we saw the first big move in US Treasury yields, underlining what would be the most talked-about market dynamic of the week, one that would have a considerable impact of gold pricing on Friday. Yields on the US 10-year Treasury note ripped as high as 0.925% as investors appeared to place bets on their outlook for an eventual US recovery in 2021 as well as the concerted fiscal and monetary stimulus measures that will be needed to bring it about. Treasury yields consolidated their strong gains on Tuesday’s book, just as precious metals consolidated their rises in value; gold had pushed back t0 $1815/oz while silver arced back to resistance at $24. With the start of a new trading month, US stocks rallied ever-higher to new records as the US Dollar weakened.

It had become clear by midweek that the horror of new infections and mounting death tolls due to the coronavirus pandemic was being overshadowed by an optimistic outlook for the US and global economies which is predicated on last month’s successful vaccine trials being the key to unwinding the economic damage wrought by 2020. Tuesday’s market moves were played out again on Wednesday, although with somewhat less enthusiasm for stocks. American equity benchmarks rose mildly through the day, with most of the momentum appearing to come from comments, reports, and rumors that the US Congressional leadership is once again taking up crisis negotiations around a fiscal stimulus as many US states look to reimpose harsh pandemic lockdowns. Gold enjoyed a stronger flow of new buying, ultimately rising to $1830/oz in spot markets, while the selling in US Treasury debt persisted through a somewhat contentious joint congressional testimony from Federal Reserve Chair Jerome Powell and outgoing Treasury Secretary Steve Mnuchin. Yields on the US 10-year climbed as high as 0.95%.

Gold Peaked at $1840/oz Midweek and Consolidated, as the Market Reaction to Vaccine Distro Issues and a Dire Jobs Report Underline Investors’ Desperation for Optimism

On Thursday, momentum took a rest across the charts of most major financial assets. Gold prices demonstrated reliable support, holding on to most of the week’s gains, but was seeing strong resistance at the $1840/oz level. Silver struggled to maintain momentum above $24. US equities touched fresh new highs during morning trading, but fell and ultimately closed the session at a loss after reports that Pfizer is already encountering logistical complications in planning distribution of their Covid-19 vaccine. We’ve touched on it a couple times since this recent surge of vax-backed optimism has come to dominate the markets since mid-November, and I still think that the broader market’s risk appetite is still vulnerable to this issue: the most recent market moves are predicated almost entirely on theoretical changes to the US economy’s trajectory in a world with a vaccine against the coronavirus that has sent 2020 into the wash and cost so many lives. This leaves the feel-good market dynamic very susceptible to the bloodless limitations of reality, and the wrong “supply-chain hiccup” coming at the wrong time could easily send equity markets reeling, resetting the short- to medium-term valuations of safe havens like gold and the US Dollar. I certainly can’t predict with any certainty when—or even if—this reckoning will come, but I believe that an intelligent trader is keeping their eyes out for it.

In the meantime, Friday morning delivered the cautiously awaited Jobs Report for the US labor market in the month of November, and the headline NFP number landed with a depressing thud. Reporting a (relatively) dire 245,000 jobs added last month, the official non-farm payrolls tally just barely surpassed the 50% mark of the expected number (469K) and the labor market report also saw last month’s number revised slightly lower. The data drives home the fact that the resurgence in coronavirus across the US as many metro areas likely lifted already underwhelming preventative restrictions too early has put a damaging dent in the initial US recovery even before the reinstatement of said (still underpowered) economic restriction. While it would have been right to expect a strong move higher in gold, the US Dollar, and other key safe havens immediately following such a blow, gold only feinted higher on the news before turning lower.

Gold fakes higher, then breaks lower on that non-farms payroll miss. pic.twitter.com/7GiwDvHMdM

— Ed van der Walt (@EdVanDerWalt) December 4, 2020

The Dollar has also been weaker today, and at the time of writing the Dow Jones Industrial benchmark has picked up nearly 200 points on the day. The reason for these unexpected moves is reflected, as I mentioned before, in the sharpest move of the day: another sharp spike in US Treasury yields: Yields on the benchmark pushed as high as 0.97% just after the release of the Jobs Report, breaking to levels untested since March.

The general understanding of this dynamic is that such a concerning picture of the labor market, coming at a moment when it’s pretty clear that conditions are absolutely going to get worse before they get better, surely will force the US legislature into pushing through meaningful and effective stimulus measures to rescue small businesses and the US consumer. In the debt market, that sentiment is being expressed in a steepening yield curve and in the equity market as another day of gains. After all, if you’re certain that things will have to improve from here, why not buy in at the bottom? Right? Am I laying on enough sarcasm here?

Before we look ahead to next week, I’ll just suggest you look back about four paragraphs for an idea of what the pitfalls of this paradoxically improved market sentiment may be…

Next Up

Next week we get another look at the state of consumer inflation, and I’m expected a decent dance card in terms of Fed commentary. That said, the stage has been firmly set for “new” stimulus bill negotiations to dominate market sentiment through the headlines.

For now, traders, I hope you can get out and safely enjoy your weekend for the next couple of days. After that, I’ll see everyone back here on Monday for our preview of the week ahead.

Gold Price Chart

More articles from John Moncrief