Good morning traders, and welcome back to another week in the metals and currency markets.

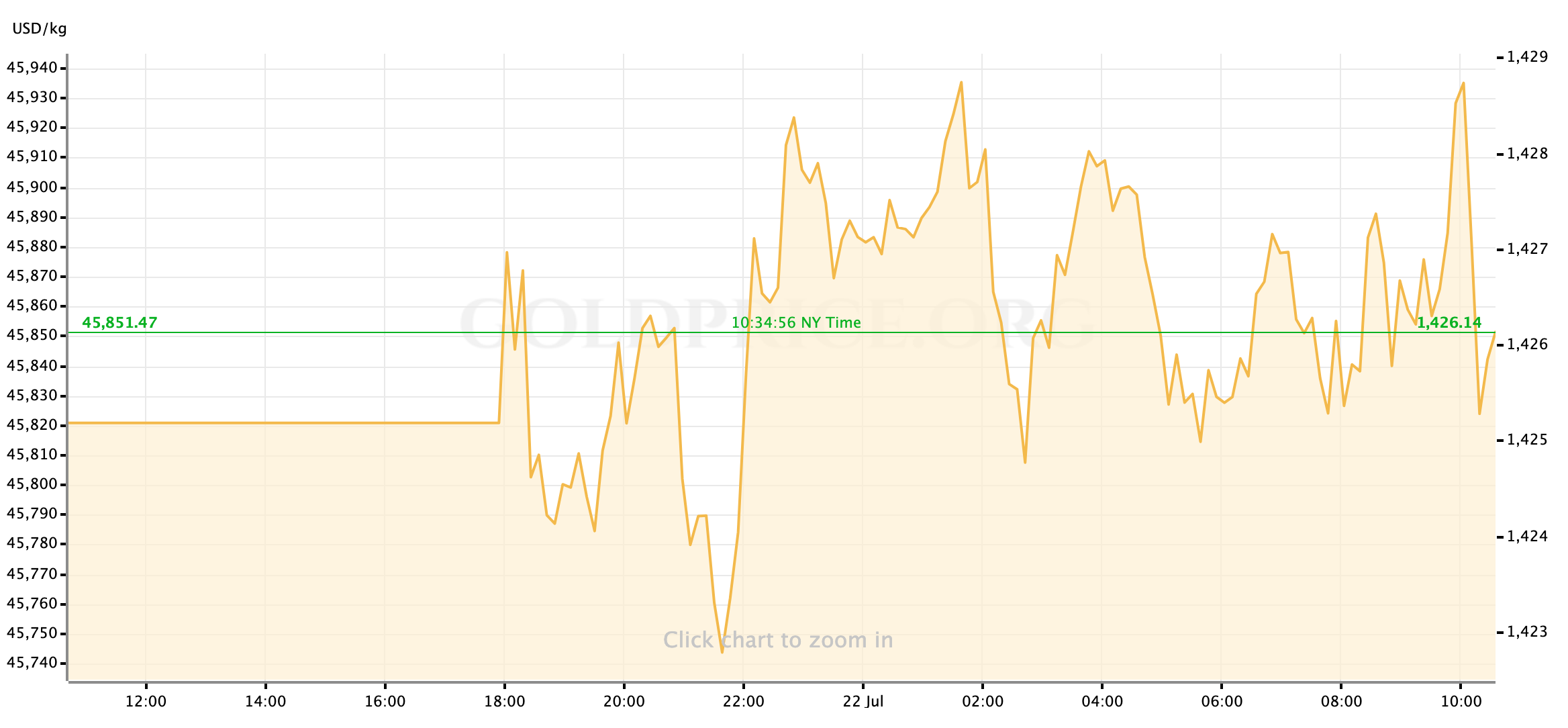

This morning gold prices are trading sideways and consolidating after an energetic few weeks in a market environment that has some strong bullish-gold potential. At the time of writing this morning, gold spot prices are trading at $1426/oz, effectively flat to Friday’s close. Silver spot prices, which topped a 13-month high in a frenetic week of growth last week that no doubt added to gold’s momentum, are off to another impressive morning at $16.34/oz.

As you’ll see, the data calendar is a bit light this week as the FOMC moves into its pre-meeting quiet period. In terms of more narrative drivers, we’ll be tracking the drama between the US and China trade delegations which this morning got some faint signs of improvement (that we’ll nonetheless try not to be fooled by) and the tense situation in the Persian Gulf following Iran’s capture of a British oil tanker this weekend.

US Economic Data to Watch

Tuesday, July 23 at 10am EDT // Richmond Fed Manufacturing Index (July)

[consensus exp.: +5 // prev.: +3]

Last week we saw a hearty rebound in the NY Empire State and Philly Fed surveys of the US manufacturing sector, so the consensus expectations for +5.0 this time around might be a light guess. As with last week’s data, expect some dollar strength on this one and the correlating headwinds for gold prices.

Tuesday, July 23 at 10am EDT // Existing Home Sales (June)

[consensus expectations: -0.2% MoM // previous: 2.5%]

Existing Home Sales have been a pretty un-volatile data point over the last 12 months, so after a strong performance in May it would be reasonable and certainly not alarming to see a mild pullback in June’s numbers.

Wednesday, July 24 at 10am EDT // New Home Sales (June)

[consensus exp.: +5.4% MoM // prev.: -7.8%]

Like with the Existing Home Sales data, New Home Sales have been fairly stable of late. May’s slowdown was a deep one however, so a downside surprise again for June has the potential to put a dent in the Greenback.

Thursday, July 25 at 8:30am EDT // Durable Goods Orders (June)

[consensus exp: +0.7% MoM // prev.: -1.3%]

The dominant input for Durable Goods Orders, it appears, will continue to be the meaningful decline in purchases of commercial aircraft, driven primarily by the Boeing’s ongoing 737 MAX boondoggle. Because that’s been the story for a while now, I wouldn’t expect a low month-over-month increase (as anticipated) to roil risk markets to any degree. Still, global manufacturing has been struggling even if last week indicated that here at home it remains strong, so there may be some underlying pressures on the core Durable Goods data. A disappointment along the lines of a consecutive negative print could be enough to spook more risk-off positioning into gold.

Thursday, July 25 at 8:30am EDT // Initial Jobless Claims

[consensus exp.: +219k // prev.: +216k]

Friday, July 26 at 8:30am EDT // GDP Growth Rate (Q2)

[consensus exp.: +1.8% QoQ // prev.: +3.1%]

In my experience, the initial look at quarterly growth in the US economy often has a noticeable (if brief) effect on major assets, but that impact in mostly as a result of the where the headline number comes in relative to expectations, rather than notional number itself; so it’s best to be a live observer, and able to adjust your positions as necessary when the date comes out. For a refresher: a poor performance, especially given what a decline the market’s consensus number is versus Q1 growth, will hit the US Dollar hard and spur a tailwind for gold prices; meanwhile, an outperformance would have the opposite effect across risk markets.

All this is likely to be amplified by the market’s current fixation on predicting the path of Fed policy, the view of which would certainly be altered by an upside- or downside-shock in headline growth.

Global Economic Data to Watch

Thursday, July 25 at 7:45am EDT // ECB Interest Rate Decisions & Press Conference

[no change to monetary policy is expected]

We’re looking for further (and more “official”) dovishness in the statement language as well as ECB President Mario Draghi’s comments in the press conference. More specifically, markets expect more indications of an interest rate cut and the resumption of QE at the September meeting. There also may be some allusion to (so far) unofficial discussions about adjusting the central bank’s inflations target.

All of these markers should lead to a weakened Euro currency, and as a result, a temporarily strengthened US Dollar that will suppress gold prices a bit. That impulse is almost certain to be temporary of course, and wouldn’t persist past the Fed’s July 31 meeting which, it’s assumed, will involve a rate cut of its own. There is, of course, some risk that markets could overreact on Thursday not to the ECB’s actions, but to tweets that will almost certainly come from the White House about the supposed unfairness of it all; in that case I would expect gold’s already slight downside to be lessened. Really, there’s not concrete reason for the market to react to that kind of input, but it has certainly happened before.

And that’s how the week looks for us, traders. I wish you all the very best of luck in the markets this week, and I’ll see you back here on Friday for a closer recap of the week’s trading.

Gold Price Chart

More articles from John Moncrief