Good morning, traders; Welcome to our market week preview, where we take a look at the economic data, market news and headlines likely to have the biggest impact the price of gold this week and beyond, as well as market prices for silver, the US Dollar, and other key correlated assets.

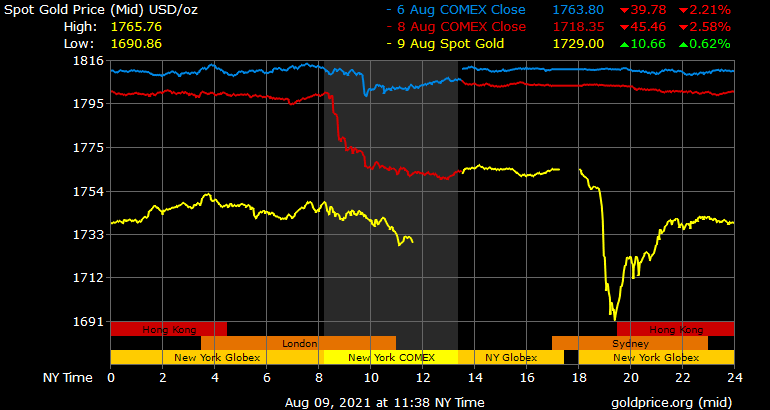

The gold market is still working to consolidate some stability this morning following a “flash crash” that rocked the yellow metal’s chart when global trading reopened on Sunday evening.

We still don’t know specifics on what initiated and/or drove the cascading sell-orders at the start of trading, and as in most cases we likely will never get a clear picture. But, given last week’s activity, we’re probably safe to assume it was some combination of very shallow liquidity (typical over a summer weekend) while investors and large managers have still been trying to sort out the recent jitters in the bond market. (The start of the selling in gold coincided again with the 10-year Treasury Note’s yield pushing back above 1.3%, a level we highlighted on Friday.)

With more traders bringing more market depth online—and, with inflation data on the docket this week, certainly at least some traders taking advantage of what they calculate to be cheaper gold-buying opportunities—prices quickly snapped-back from the lows, although at the time of writing gold prices are still sitting roughly $30/oz below last week’s close. With a relatively light data and news calendar for the second week of August, gold traders will want to keep their eyes on the bond market for the next few days (at least) and be prepared for gold spot prices to react negatively to any acute spike in Treasury yields, at least until the benchmark 10-year falls away from 1.3%.

For now, let’s take a look at the rest of the calendar ahead.

US Economic Data to Watch

Wednesday, August 11 at 830am EDT // Consumer Price Index (July)

[(core) consensus est.: +4.3% YoY // prev.: +4.5%]

[(headline CPI) consensus est.: +5.3% YoY // prev.: +5.4%]

Expectations this week are set for July’s consumer inflation to hold near the recent high-water markets on year-over-year basis but, importantly, to ease as compared month-to-month. Economists expect that some of the strongest pressures of the 2H surge in inflation—the ones that the Fed has pointed to as the most “transitory” in their argument that higher inflation will not be persistent just yet—began to slow over the last month. Key among them: Used care prices and massive crunches in the global supply chain for micro-chips. As used care prices ease their effect should fade at the same pace, while the improvement of silicon chip availability will take a little longer to filter through the global economy and other acute drivers of the reopening inflation spike (like air travel and hotel spending) will remained elevated through the end of the summer as normal. The mildness of the shift in inflation numbers, assuming they print close to expectations, could mean we see little reaction in gold or its correlated markets. But if investors and analysts as a group do decide to read the data as the first signals of recent inflation easing, gold prices may see strong support and some upward momentum as a result of strengthened conviction that the Fed will be able to hold interest rates to the floor as planned.

Thursday, August 12 at 830am EDT // Initial Jobless Claims

[consensus est.: +375K // prev.: +385K]

Last week’s release went mostly unnoticed amid Wednesday’s bond market surges and the Friday Jobs Report, but it does seem as if last month’s sudden surge in weekly new unemployment claims was just an outlier, and the steady (if slow) decent towards a more normal rate continues. As always, keeping an eye on the weekly data helps us to better anticipate the longer-form trends of the labor market recovery, and then to better anticipate any upcoming Fed decisions.

FedSpeak this Week

The reaction in financial markets to remarks from Fed Vice Chair Richard Clarida last week, reasonable or otherwise, serves a clear reminder that, at this point in the Fed’s dovish policy cycle, while most occasions of public comment from FOMC officials only nudge markets (or markets’ understanding of the Fed’s expectations) slightly, they can sometimes make a decisive impact on the trading session for a specific asset or a group of them. With that behind us—but the reverberations for gold still being felt via the Treasury market—lightening is unlikely to strike in consecutive weeks, but these are the scheduled Fed appearances worth being aware of.

Monday: Richmond Fed President Tom Barkin (FOMC voter) (12pm EDT)

Tuesday: Cleveland Fed President Loretta Mester (non-voter) (10am EDT)

Wednesday: Atlanta Fed President Raphael Bostic (FOMC voter) (1030am EDT)

And that’s how the week lays out ahead of us, traders. As always, I wish you all the very best of luck in your markets in the coming days, and I’ll look forward to seeing you all back here on Friday for our market-week wrap up.

Gold Price Chart

More articles from John Moncrief