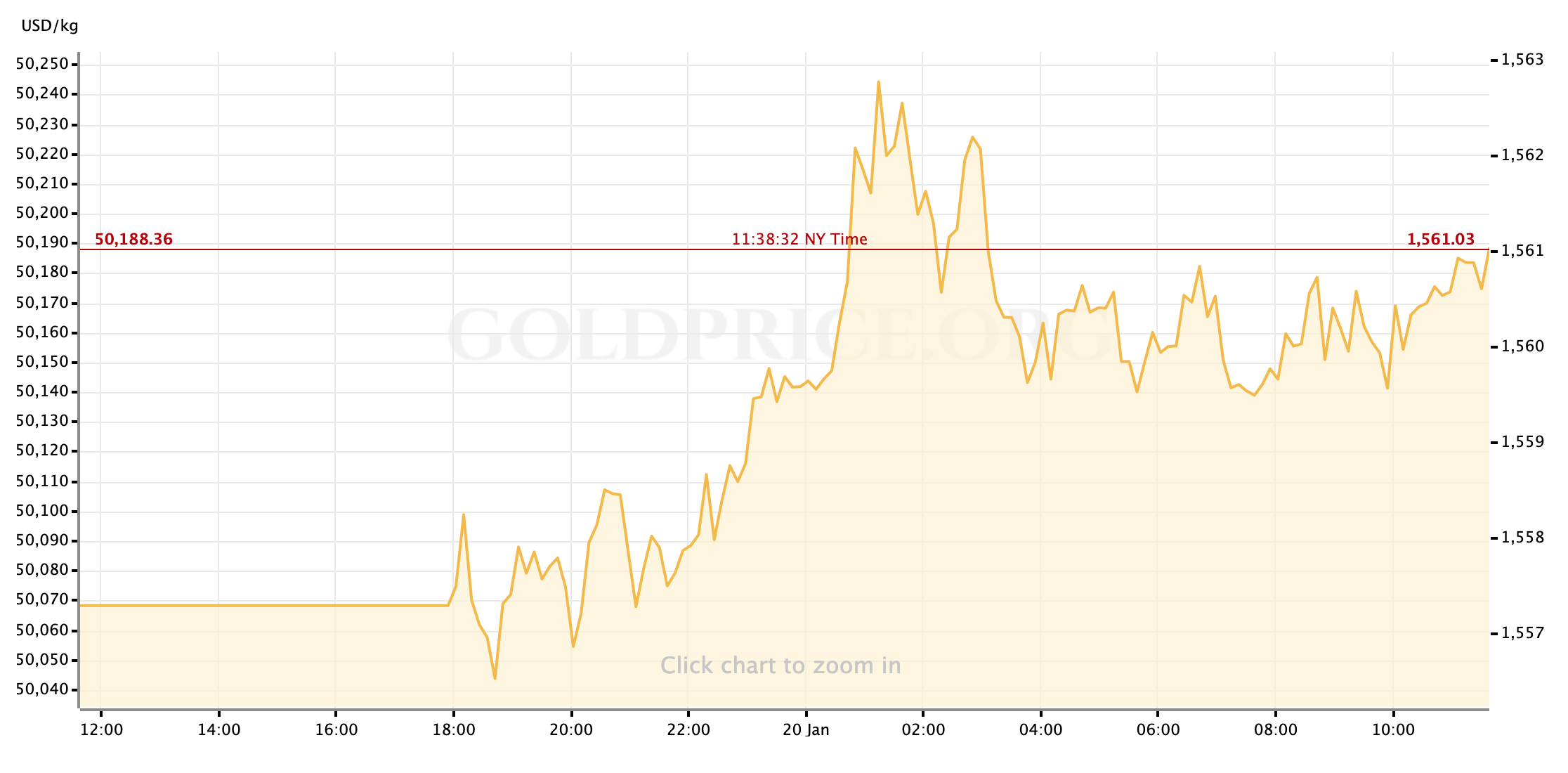

Hello, traders; welcome back to our weekly preview of the next five trading days, with a focus on the macro data and developing stories that could matter most of precious metals and Dollar trading. Gold prices have traded lightly this morning in the shallow market but have moved slightly higher to recover $1560/oz after Friday afternoon’s profit-taking saw the yellow metal weaken slightly.

This week’s macroeconomic calendar is particularly light, made even more so by today’s market holiday in the US. We also have no appearances by FOMC members to mark, as we’ve entered the “quiet period” ahead of next week’s Fed meeting. With that in mind, headlines (and, potentially, rumors) are expected to continue to run the show as far as market drivers go. While the impeachment trial in the US has done little to actually rattle markets recently, I expect it to take a more prominent role in the news cycle this week so the potential for it to impact risk appetite is higher. I suspect, if only as a distraction from impeachment proceedings, there is the possibility of headlines around US-China trade relations (positive or negative) popping up.

For now, let’s take a look at what we can expect to see this week.

US Economic Data to Watch

Wednesday, January 22 at 10am ET // Existing Home Sales (Dec)

[consensus expectation: +1.5% MoM // previous: -1.7%]

Understandably, there’s not a great deal of correlation between a given month’s Housing Starts and its Existing Home Sales number. But, given the blowout starts numbers from Friday and the impact, however brief, that had on the Dollar and gold prices, there may be a few extra eyes on this week’s housing data (especially with little else to put focus on.) You know how this works by now: a strong performance in a housing number is a headwind of gold prices and vis versa; I don’t really anticipate movement on Existing Home Sales this week, but it at least deserves some attention.

Thursday, January 23 at 8:30am ET // Initial Jobless Claims

[consensus exp.: +214k // prev.: 204k]

Friday, January 24 at 9:45am ET // Markit Manufacturing PMI & Services PMI (Jan)

[(manufacturing) consensus exp: 52.8 // prev.: 52.4]

[(services) consensus exp.: 52.5 // prev.: 52.8]

Regular readers may have noticed that I don’t typically point out Markit’s version of PMI data for the manufacturing or services sectors in the US. That’s a factor, mostly, of US macro traders tending to put more focus and positioning on the ISM results. Recently though, after a few months in which Markit’s number for both categories were pinned to the growth/contraction breakeven (50.0,) the indices have been lifting off the ground (albeit slightly.) What I’m looking for this week is whether or not that uptrend continues, with an eye towards predicting the “more important” ISM data sets strengthening (or otherwise) the assessment of growth in the US.

Also, on this week’s data desert of a calendar, this second-tier data set may just pull the most attention before the end of the week, so it’s savvy for a trader of risk assets (I.e., gold) to at least have it on their radar.

Global Economic Data to Watch

Monday, January 20 at 10pm ET // Bank of Japan Interest Rate Decision

[no changes to monetary policy are expected]

While analysts and observers see any adjustment to policy this month as highly unlikely, there is some anticipation that recent performance in the Japanese economy will lead the BoJ to upgrade their outlook for 2020 and possibly push back the possibility of any lowering of short-term rates. Positive notes from Japan’s central bank would likely boost the Yen enough to add a tailwind to other non-Dollar safe havens like gold, positioning the yellow metal for further gains as the trading week gets started in earnest. I’ll also be looking to see if the BoJ offers any commentary on a changed state of play in Asia following the signing of China’s “phase one” trade deal with the US.

Thursday, January 23 at 7:45am ET // ECB Interest Rate Decision

[no change to monetary policy is expected]

Similar to BoJ this week, we don’t expect any form of policy movement from the European Central Bank but we will be looking for some rosier language in the committee statement. With the manufacturing sector (among other pressure points) showing signs of cyclical improvement recently, observers will be looking to see how ECB President Christine Lagarde and her team will walk the line between acknowledging that 2020 could be a year of strength for the Euro Area while also allaying expectations (for now) of tighter monetary policy. As such, there could be some added volatility in the Euro (passing through to DXY) on Thursday morning.

And that’s how the week ahead looks, traders. As you can tell, data flow will be very light and so I expect headlines to continue to dominate the market mood and risk appetite as we head into the end of January. I wish you all the best of luck in your markets this week, and I’ll see you back here on Friday for our usual market wrap.

Gold Price Chart

More articles from John Moncrief