Happy Friday, traders. Welcome to our weekly market wrap, where we take a look back at these last five trading days with a focus on the market news, economic data and headlines that had the most impact on gold prices—and may continue to into the future—as well as the charts for silver, the US Dollar and other key correlated assets.

Gold prices are consolidating recovered gains at the end of a relatively quiet trading week.

Although the yellow metal’s spot price hasn’t enjoyed quite as strong of rebound as analysts might expect based on the performance of risk assets this week and a somewhat weaker Dollar, it’s a constructive sign to see gold consolidating this week’s moderate gains after the Sunday evening open.

So, what kind of week has it been?

You did not, in fact, sleep through or otherwise miss any major “happenings” in financial markets this week. As we ease into the summer months, investor activity and market mechanics are slowing to a crawl. While it may feel abnormally slow already, much of that may be attributable to remembering a much more active summer of 2020, in which everyone was stuck at home and trying to chart a path forward through the Covid pandemic crisis. The calm that’s in store for most of the next two months would fit in comfortably with the doldrums of summer 2019 and most of the years before that.

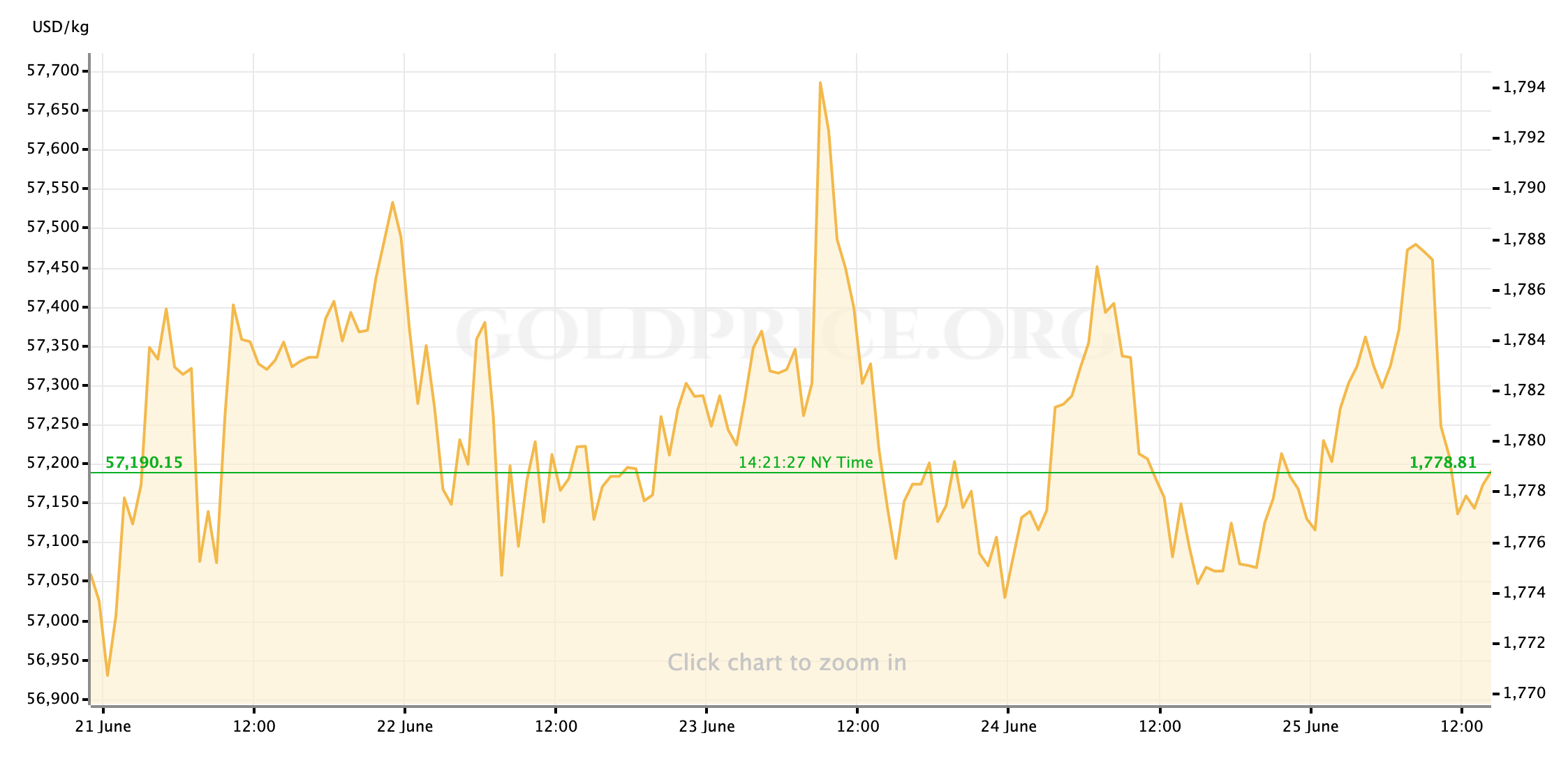

Looking at this week’s trading through the lens of last week’s “damage” post-FOMC: US stock markets have enjoyed a mostly productive week, and on Friday afternoon the S&P 500 looks poised to turn in its strongest week in over well over a month; and the surge in the US Dollar that the Fed’s slightly accelerated rate path projections sparked off last week has noticeably pulled back. Gold prices have been less corrective, however. While the yellow metal is showing solid support above the $1770/oz level in spot markets, its chart has traded in a relatively narrow band that seems to be capped by resistance at $1790.

With the benefit of a week’s time to process the specifics of the new Fed projections, market participants seem to generally agree that aggressive risk-off reaction that followed last Wednesday’s FOMC was some combination of overreactive and premature; But while investors appear comfortable buying the very moderate dip in equities there is less interest in bidding gold back up toward it’s springtime highs. To some degree this could be an effect of the overall commodities complex not getting the same boost (this week, at least) from the reflation trade that has benefited gold so much in 2021. But I think it’s a result of more specific concerns about gold: investors are hesitant to bid gold back up if, as starkly demonstrated by last week’s trading, anyone buying into the yellow metal faces the risk of another collapse (justified or not) initiated by the next steps or signals farther along the path toward rate hikes.

As I said at the top, it seems like a generally constructive sign that gold has spent a calm market week consolidating above last week’s lows rather than continuing a slide. But it does appear that we’re moving into a dull summer for precious metals, and that the only real shifts in trend or trajectory will have to come from acute, unexpected shocks to a marketplace that’s mostly interested in taking the summer off.

With that in mind, before everyone checks out for the weekend (or summer holiday,) I think it’s worth touching briefly on two possible avenues for that kind of shock between now and September: Fed signaling, or inflation and/or labor market data surprises.

- Signals from the Fed, being interpreted “correctly” or otherwise by the marketplace, seem to me the most likely source of potential volatility in gold or US Dollar markets this summer. Most near-term outlooks focus the Fed’s annular Jackson Hole symposium at the end of August, at which point it’s believed that Powell & Co. will introduce forward guidance about beginning an asset-purchases taper to start in December. But we’ll also have a regular FOMC meeting and presser a month before that, and two sets of discussion minutes.

- Announcements, commentary, or corrections from Fed officials individually or the FOMC as a body that “the markets” sees leaning farther into possibility of the central bank tightening in 2023 (or even as early as the end of next year) can be expected to pull down on gold prices. Conversely, if the Fed is perceived to be trying to walk back on last week’s (very) slightly hawkish shift then gold stands to gain new tailwinds from the reflation trade.

- An obvious roll-back in Fed language/signals towards the “lower for much longer” plan of early 2021 would probably be the direct result of negative surprises in monthly labor market data: A stark deterioration in the current jobs recovery would generally spook markets into a more risk-off mood that could benefit gold prices.

- In this case, poor data would also push back expectations for interest rate hikes, resetting market conditions to those that aided gold’s major rally through the first five months of 2021.

- On the other side of the coin is the possibility that inflation remains hot at recent highs for longer than expected, putting more pressure on the Fed’s supposition that elevated prices are “transitory.” The result in that case, even before comment from the Fed, would likely be a repeat of last week’s massive selling pressure on gold prices (and probably large parts of the stock market as well.)

- The calendar points for these lines of volatility risk are somewhat evenly spaced-out on the summer calendar. First up, next week will close with the release of the US Jobs Report for June; At the time of writing, the consensus estimate shows a moderate improvement over the pace of hiring in May.

For now, traders, I hope you can get out and safely enjoy your weekend for the next couple of days. After that, I’ll see everyone back here on Monday for our preview of the week ahead.

Gold Price Chart

More articles from John Moncrief