Good morning, traders; Welcome to our market week preview, where we take a look at the economic data, market news and headlines likely to have the biggest impact the price of gold this week and beyond, as well as market prices for silver, the US Dollar, and other key correlated assets.

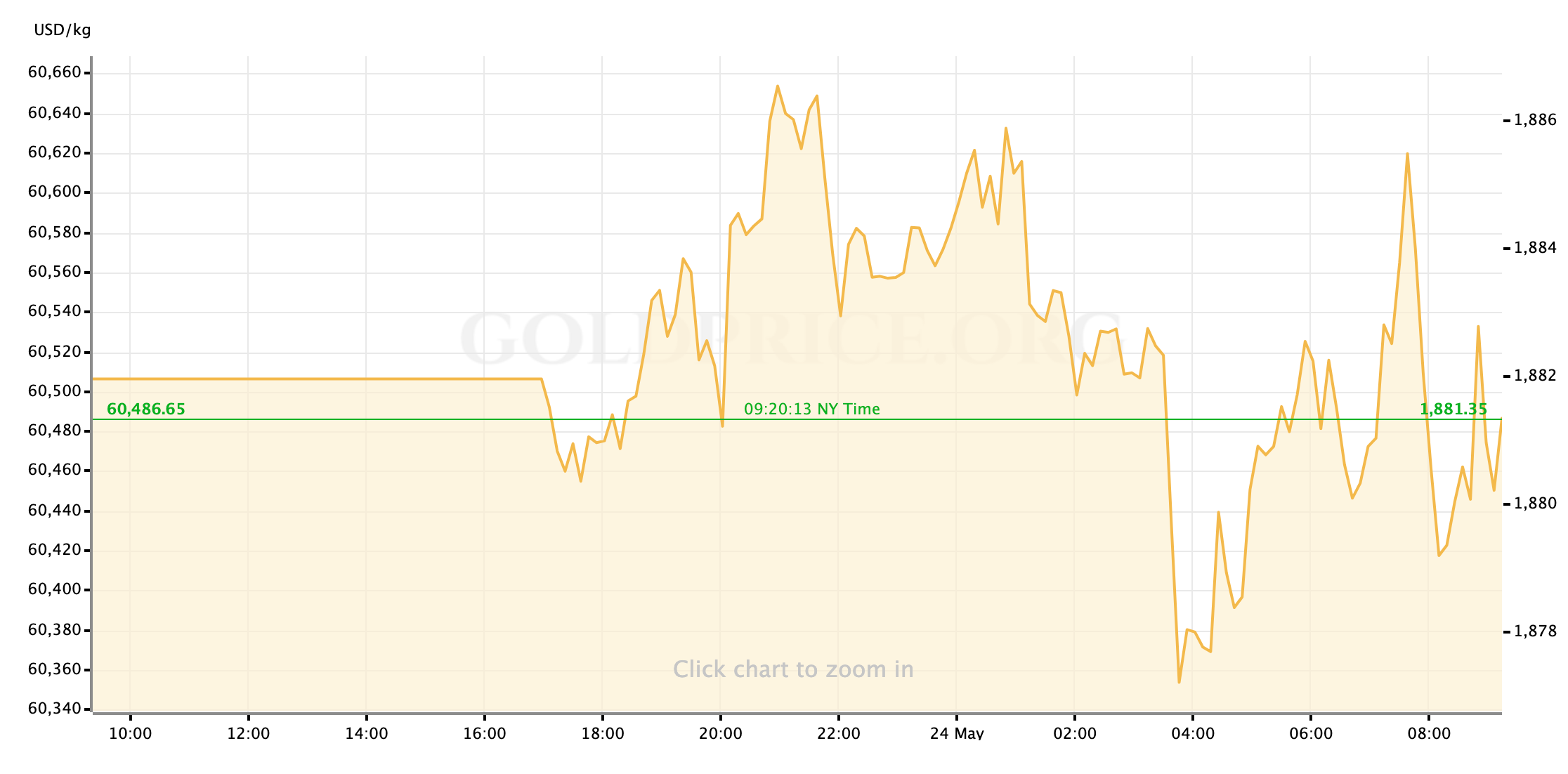

After a bit of back-and-forth during the overnight sessions, gold prices are trading relatively flat to last week’s close, having consolidated strength and support around the $1880/oz level.

With another relatively light economic calendar this week leading up to the Fed’s inflation reporting on Friday, we’ll be keeping an eye on headlines and moves in other correlated assets that might impact the precious metals. For now, I’m watching to see if the prior strength of the broader re-opening/reflation trade returns to boost US stock markets, which have turned in two consecutive weeks of losses. If so, there’s potential for gold to participate as well and launch higher from Monday’s position. I’m also keeping an eye on news, out this morning, that the Chinese government is preparing to directly intervene in its commodities markets. As of now it’s unclear what impact this kind of restriction would or could have on gold markets; But, as China is such a keystone for global commodities demand, I have to assume there will be repercussions.

For now, let’s have a look at the week ahead.

US Economic Data to Watch

Thursday, May 27 at 830am EDT // Q1 GDP (2nd Estimate)

[consensus est.: +6.5% QoQ // previous est.: +6.4%]

The progressive revisions of GDP after the first reading typically don’t draw a lot of attention around here, but with the recent hitch in the run of strong US economic data signaling recovery it’s possible that analysts and investors are going to be looking for any more positive inputs they can find to keep the re-opening/reflation trades from losing momentum. That shouldn’t be an issue here, as there’s rarely any extreme variations from the BEA’s first number for a given quarter (although there are more than a few analysts expecting the number to actually rise, slightly.) This should be a mostly neutral number for the gold market, but priced could see a small tailwind with a reassuring number.

Thursday, May 27 at 830m EDT // Initial Jobless Claims

[consensus est.: +425K // prev.: +444K]

Investors seem mostly content to keep absorbing the steady drop in Initial Jobless Claims without putting much of aa ripple into the markets; It’s also possible that, given the lack of tie between April’s higher-volume labor market data and the BLS’ monthly reporting, they’re just not putting a lot of weight behind the weekly readings for now. An as-expected decline for another week should pull the key four-week average below 500K for the first time since the pandemic, which may be enough to further boost the reflation trade in US equities. Gold has largely participated in that rally as well, though it’s tough to say exactly how that relationship will be balanced come Thursday.

Friday, May 28 at 830am EDT // Personal Income & Spending (April)

[(income) consensus est.: -14.8% MoM // prev.: +21.1%]

[(spending) consensus est.: +0.5% MoM // prev.: +4.2%]

The steep decline in absolute terms between Income numbers from March to April looks stark, but is well within reasonability: The majority of direct stimulus checks from the American Rescue Plan were issued in the month of March, accounting for what was an aberrant spike in that month’s data, leading to a predicted correction for April. All that said, we’ve seen the market, as a mob, liable to initially overreact to new information independent of context in recent weeks; So it can’t be ruled out that the initial release of this data might put a brief slump into the pace of equity prices and even gold. If that does happen, it should only be a brief pause.

Friday, May 28 at 830am EDT // PCE Price Index (April)

[(core PCE) consensus est.: +2.9% MoM // prev.: +1.83%]

[(headline) consensus est.: +3.5% MoM // prev.: +2.32%]

The sharp spike in consumer price inflation that the Labor Department reported earlier this month is expected to be represented in Federal Reserve’s own calculation of price stability and pressures, due Friday. In the weeks since the first pop of inflation well above the Fed’s targets, Jerome Powell & Co. have continued to defend their position that these pressures are temporary for now. That doesn’t, however, change the fact that in the immediate aftermath of the CPI release came a roiling day for markets, with US stocks and gold prices falling while the Dollar and US Treasury yields climbed just as steeply. Investors this week should be spared similar dramatics, but that can’t be taken as certain. Traders might do well to keep an eye out for a similar knee-jerk reaction in Treasuries (and, by correlation, gold prices) heading into the weekend.

FedSpeak this Week

Especially where there are Q&A sessions available, I expect most reporters and analysts will be focused on getting any commentary they can on how recent trips and stumbles in US economic data (see: April’s miss of a Jobs Report) have changed the complexion of an FOMC that, at its late-April policy meeting, included “a number” of participants who believed that the time to start discussing tightening of monetary conditions was approaching. There should be at least a few opportunities for insight, with a front-loaded schedule of appearances earlier in the week before we see the Fed’s updated measurements for inflation on Friday.

Monday: Cleveland Fed President Loretta Mester (non-voter) (11am EDT); Atlanta Fed President Raphael Bostic (FOMC voter) (12pm)

Tuesday: Chicago Fed President Charles Evans (FOMC voter) (730am); Fed Vice Chair Randal Quarles (FOMC voter) (10am)

Wednesday: Fed Vice Chair Quarles (3pm)

And that’s how the week lays out ahead of us, traders. As always, I wish you all the very best of luck in your markets in the coming days, and I’ll look forward to seeing you all back here on Friday for our market-week wrap up.

Gold Price Chart

More articles from John Moncrief