Happy Friday traders, and welcome to our recap of the week in gold markets.

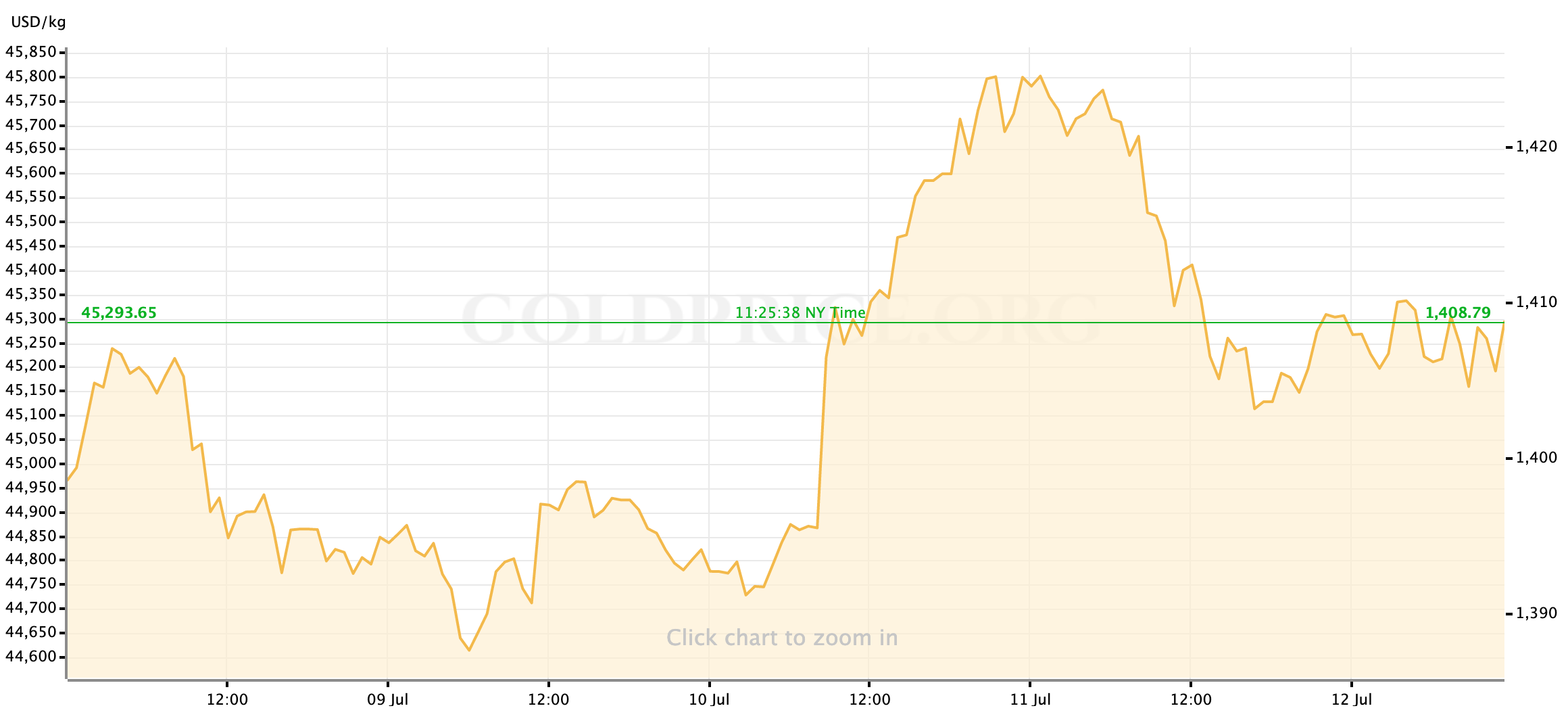

As we anticipated, the action on gold charts was pretty heavily condensed to the middle of the week and we’ve seen a wide $30 trading range over the last five sessions. At the time of writing, gold prices are holding steadily just below $1410/oz in the sport markets; prices are largely unchanged from Thursday morning and represent a fall from the weekly highs but a somewhat bullish net gain for the week.

So, what kind of week has it been?

Gold Prices Had a Calm Start to The Week

Monday and Tuesday played out quietly, as expected, in the metals markets following the selling in gold priced that began the week as we moved into the second half of 2019. Aside from a brief dip below $1390/oz in the early hours of Tuesday morning in New York, trading was choppy by mostly sideways; spot prices per ounce mostly clung to $1395 as the value of the yellow metal competed against a resurgent US Dollar which by Tuesday has reached a 3-week high. There was some light, gold-adjacent news flow, with reports that many central banks—most importantly China—have continued increasing their gold holdings; while fearful headlines out of the Persian Gulf have dramatically tailed-off over the last week, gold probably found some support from safe-haven buyers on an announcement from Iran that it will continue pushing it’s uranium enrichment beyond the bounds of the now practically defunct nuclear agreement.

Gold’s 5-week uptrend was still holding, but its bulls were in search of another push from fundamentals to restart momentum. They got it on Wednesday morning.

Fed Chair Jerome Powell Nailed a July Cut to The Table

Wednesday, as predicted, is where we found most of our action this week. Ahead of his semi-annual testimony to congress, the Federal Reserve published the text of his prepared opening remarks. Later that afternoon markets also got their first look at the discussion minutes from the FOMC’s June meeting, but surprisingly it would be this first publishing of Powell’s statement that dominated market movement (gold in particular.)

On the release of Chairman Powell’s remarks at 8:30am EDT, gold spot priced surged from heavy support at $1392 to once again surpass $1400/oz. The move was entirely driven by the re-trenching of market certainty that the Fed will implement an interest rate cut at their July meeting. In June’s statement, the committee made it clear that there was an amassing uncertainty around global and domestic economic factors (effect of the US-China trade war, slowing growth globally,) and the FOMC’s would be tracking whether these pressures would have enough of an effect to “call for additional monetary policy easing.” It was language like that which solidified market anticipation for, at minimum, a 25 basis-point “insurance cut.” That confidence was wobbled a bit last Friday, as a banger Jobs Report raised the issue that maybe the economy had already righted itself before any policy easing was necessary.

Jay Powell’s remarks on Wednesday reaffirmed the market’s interpretation of the June meeting, and underlined it. First, Chairman Powell specifically touched on the language of the June statement in his prepared language, saying “it appears that uncertainties…continue to weigh on the US economic outlook.” Later, in his testimony before the House, Powell was asked if the outstanding non-farm payrolls data from June improved the Fed’s assessment at all. Powell’s response was as clear as can be: “the straight answer to your questions is no.” To fully drive the point home, the Chairman reiterated:

“the bottom line for me is that the uncertainties around global growth and trade continue to weigh on the outlook. In addition, inflation continues to be muted and those things are still in place.”

Most major assets would continue to move throughout the latter half of the US trading session, as equities surged and the US Dollar’s recent strength waned. Gold priced would make their way back to $1420/oz. That level would find support throughout the Asian and European trading sessions as those markets digested the central bank headlines in much the same way.

Jerome Powell suggested that the Fed has room to cut interest rates as the tie between the inflation and jobless rates has broken down https://t.co/qgbzgwsJQG

— Bloomberg Economics (@economics) July 12, 2019

US Inflation Data Surprised as The Market Shifts Its Valuation of Gold Prices

Gold spot prices would breakdown from that re-elevated level on Thursday morning as updated US inflation data beat expectations with the core number coming in (just) above the all-important 2% target. As sellers stepped in—at least some of them likely to be short-term profit-takers—prices for the yellow metal dropped through $1410 and settled a few dollars below. For the most part, through mid-day on Friday the price has remained in a sideways chop around the same levels.

It’s obvious that if a blowout jobs report wasn’t enough to shake Powell and Co.’s seemingly inexorable drive towards a rate cut, then a +0.1% (annualized) surprise in core inflation—not even the “Fed-preferred” assessment of inflation, that’s PCE—isn’t going to change things either. So we can assume that gold’s drop on Thursday morning was not a result of the bond markets cutting their odds of a rate cut. What then?

What I think is that we’re seeing the markets move on from pricing/handicapping the odds of some kind of rate-cut on July 31. Now, the question is no longer “Will Powell cut in July?” but rather, how much will the cut be (the usual 0.25%? A one-timer worth 0.5%?) and how many cuts is the Fed considering? How I think this is reflected in the gold market specifically is as follows: the near-certainty of an interest rate cut in July clearly justifies (for the market) gold spot prices above $1400/oz, but the yellow metal’s reaction to Thursday’s improved inflation data suggests that for prices to trade consistently north of $1420 would require confidence that: a.) the Fed’s July cut will be larger than 25 basis-points and/or, b.) there will be at least one more cut before the end of 2019. Until either of those additional moves are more priced into markets, I think gold will have a hard time maintaining the uptrend on monetary policy alone.

Of course, other factors like further trade war escalation could prove other drivers for higher gold prices. For the time being, gold price movement seems to largely be a reaction function of US and global central bank policy.

Next Up

Next week’s macroeconomic calendar is a pretty vanilla edition, with a few scheduled FOMC appearances (including more words from Chairman Powell,) and a few new looks at the manufacturing survey data that took such a beating in June.

Enjoy your weekend, traders! I’ll see you back here on Monday for a look at the new week ahead.

Gold Price Chart

More articles from John Moncrief