Private payrolls rose by 67,000 jobs in November according to ADP and Moody’s Analytics. The figure was drastically lower than the expected results of 150,000 new jobs, indicating the slowest growth since May. The estimated minimum number of new jobs required to keep pace with growth in the working age population is 100,000.

Key Takeaways

- Job growth came in at 67,000 in November vs. 150,000 expected and down from 121,000 last month.

- Mark Zandi, chief economist for Moody’s Analytics, said “The job market is losing its shine.”

- The figure was well below the minimum number of jobs required to keep pace with growth in the working age population.

The big miss in Wednesday’s report casts doubts on the upbeat estimates for the upcoming nonfarm payrolls report due on Friday, predicted at 187,000 jobs. November’s growth marks a sharp decline from last month’s figure of 121,000, revised down from the initially reported 125,000.

Initial jobless claims have showed no signs of layoffs in the market, but hiring has slowed considerably. With a shortage of skilled workers and worsening economic conditions, there are a number of factors at play in the slowdown. The manufacturing industry accounts for 11% of the US economy, and has borne the brunt of the tariffs on imports and exports. Goods producing industries lost 18,000 jobs in November, with decline in natural resources and mining, construction, and manufacturing.

Trade transportation and utilities dropped 15,000, and information services declined by 8,000. Small businesses with under 20 employees fell 15,000. Other areas saw growth, like education and health services with 39,000, professional and business services with 28,000, and leisure and hospitality with 18,000. The end of the GM strike is also likely to boost upcoming nonfarm payrolls figures.

Manufacturing employment declined for the 3rd straight month, with the sector losing 6,000 workers in Nov., according to ADP estimates. It was the 5th decrease in net hiring for manufacturers YTD, but with employment in the sector averaging 2,280 per month over that time frame. pic.twitter.com/5K0hY6NXsa

— Chad Moutray (@chadmoutray) December 4, 2019

Expert Outlook

Moody’s Analytics chief economist Mark Zandi pointed the finger at the Trump administration’s ongoing trade war with China, stating that the conflict had done more damage than he initially realized. The trade war has resulted in punitive tariffs from both nations, impacting employment, manufacturing, and business investment. However, while the jobs market has so far weathered the storm and continued to drive the economy, it may be slowing down.

“The job market is losing its shine,” Mark Zandi, chief economist for Moody’s Analytics, said in a statement. “Manufacturers, commodity producers, and retailers are shedding jobs. Job openings are declining, and if job growth slows any further unemployment will increase.”

“The slowdown is more significant than I would have thought, and I do think that goes to the trade war,” he said in a separate statement. “The trade war is doing damage to the economy and the jobs market.”

“One bad month is not a trend, but the forward-looking surveys signal no relief over the next couple of months, at least,” Ian Shepherdson, chief economist at Pantheon Macroeconomics, said in a note. “This is not about supply-side constraints, with firms unable to find all the people they want; labor demand clearly has weakened as the trade war has dampened activity, both directly via the cost of the tariffs and indirectly by creating great uncertainty for businesses.”

Market Reaction

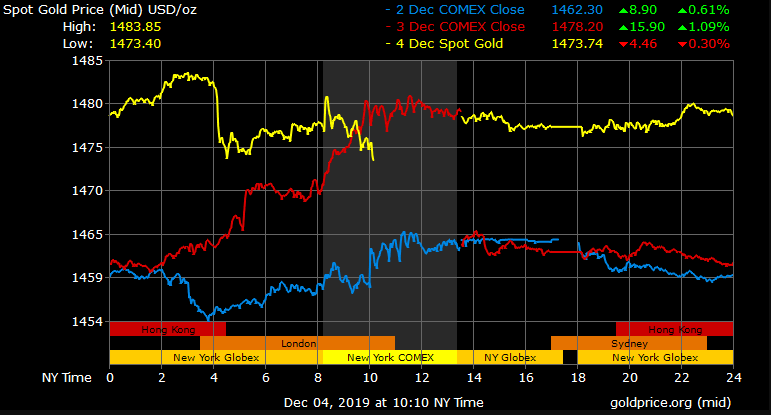

Gold prices saw brief upward momentum, but have since faced selling pressure following the news. Spot gold last traded at $1,473.74/oz, down -0.30% with a high of $1,483.85/oz and a low of $1,473.40/oz. Tomorrow’s release of the nonfarm payrolls report along with initial jobless claims will further clarify the state of the job market.

Gold Price Chart

More articles from Conor Maloney