The Institute for Supply Management (ISM) PMI came in at 41.5 last month, down from 49.1 in March. While this indicates a steep contraction, the figure is better than the expected drop to 36.9. Employment sunk dramatically to 27.5, while new orders fell to 27.1.

Key Takeaways

- The ISM manufacturing purchasing managers index sunk from 49.1 to 41.5 vs. 36.9 expected.

- The employment index fell from 43.8 to 27.5, with 30 million Americans out of work in the last six weeks.

- ISM manufacturing business survey committee chair Timothy Fiore described the survey comments as strongly negative.

Out of 18 surveyed manufacturing industries, only two reported growth in April, namely paper products and food, beverage, and tobacco products. 15 industries reported contraction, led by printing and related support activities, furniture and related products, and transportation equipment.

Sentiment was very low, with three negative comments for every single positive comment. Survey committee chair Timothy Fiore stated that sentiment had taken a dive due to the impact of the coronavirus outbreak and the recession in the energy market.

April ISM Manufacturing PMI comes in at an above consensus expected 41.5. Scratch beneath the surface, however, and there lay some truly depressing numbers.

New Orders - 27.1 (down from 42.2)

Employment - 27.5 (down from 43.8)

This will be a long road back for US Manufacturing

— Michael Gawda (@MichaelGawda) May 1, 2020

“The coronavirus pandemic and global energy market weakness continue to impact all manufacturing sectors for the second straight month. Among the six big industry sectors, Food, Beverage & Tobacco Products remains the strongest. Transportation Equipment and Fabricated Metal Products are the weakest of the big six sectors,” said Fiore. Sentiment is now at the lowest point since the 2009 financial crisis.

Report Data

New orders fell 15.1 points from 42.2 in March to 27.1 in April. Production fell 20.2 points to 27.5. Backlogged orders fell 8.1 points to 37.8, with businesses having more time to catch up on backlogs due to reduced demand for their services despite staff reductions. Employment fell 16.3 to 27.5, with 30 million Americans filing for unemployment benefits in the last six weeks alone. Supplier deliveries rose 11 points to 76, indicating delays in delivery times and disruption to national and international supply chains.

Any reading below 50 indicates contraction, and the current state of the manufacturing industry indicates that it may take years to recover.

Survey Respondents

A respondent from the heavily-affected transportation industry commented to say “COVID-19 has created a wave of activities, including vendors closing, vendors focusing only on the medical industry, employees not coming to work, [and] delayed shipments from overseas..”

A respondent from the apparel, leather, and allied products industry commented on the increased demand for essential items. “The company I work for manufactures personal protective equipment [PPE], specifically N95 masks, face shields, as well as selling protective clothing and hand protection. In the area of PPE, our backlog has spiked to numbers we have never seen. While no doubt some of the backorders will be cancelled, many of the orders are longer term commitments from [the] U.S. government.”

Similarly, a respondent from the chemical products industry stated that production stopped in their plant for everything except the production of hand sanitizer.

Market Reaction

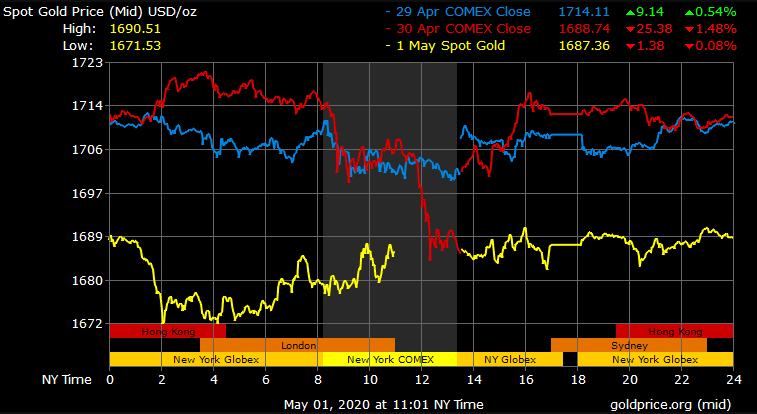

Gold prices are down today, sliding further after breaking support at $1,700 in yesterday’s session. Spot gold last traded at $1,687.36/oz, down -0.08% with a high of $1,690.51/oz and a low of $1,671.53/oz. Spot gold prices saw little reaction to the ISM data, which outperformed expectations despite indicating a sharp contraction in manufacturing. Soft inflation and improved performance in the stock markets are likely factors in the downward pressure seen in the gold market today.

Gold Price Chart

More articles from Conor Maloney