Good morning, traders; Welcome to our market week preview—the last of the year!— where we take a look at the economic data, market news and headlines likely to have the biggest impact the price of gold this week and beyond, as well as market prices for silver, the US Dollar, and other key correlated assets.

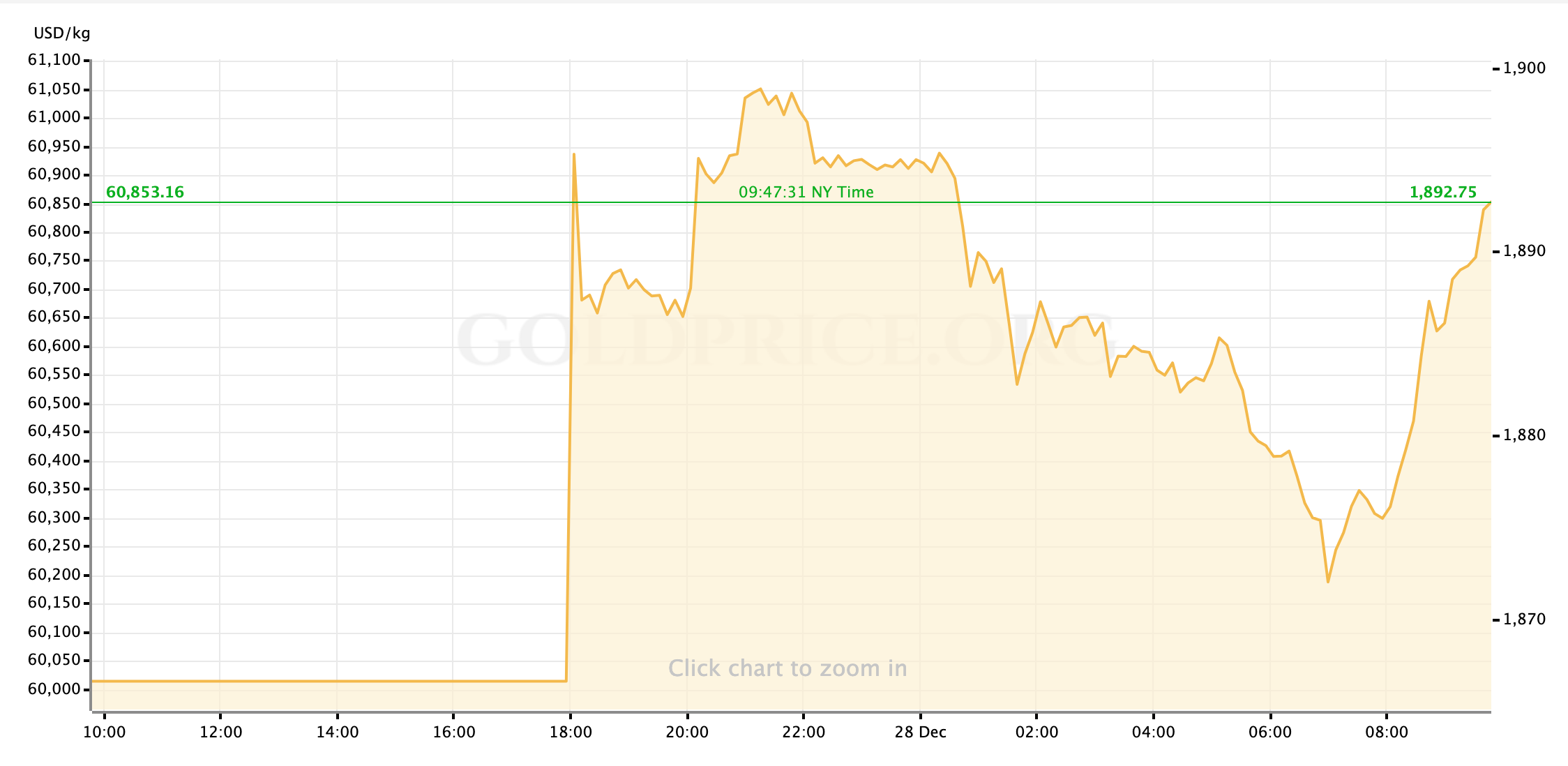

Gold prices are moderately higher this morning, following an active overnight session as thin holiday markets reacted to the US President’s capitulation to signing a government funding bill that included a roughly $900B round of fiscal support for American consumers and small businesses. Asian markets initially bit gold sharply higher alongside equity prices, with the yellow metal briefly looking to challenge resistance at $1900/oz.

After failing that test, the more sparsely attended European session let gold prices lag, but the start of US pre-market trading has again seen buyers (more steadily this time) shifting into gold positions in favor of the Dollar or US Treasury debt. At the time of writing, even as US stock markets get off to a decent start on the news of the stimulus bill’s signing, gold spot prices are rising towards $1895/oz.

With the New Year’s holiday falling too late in the week for us to see the December Jobs Report just yet, the economic data calendar is light and market action will likely be dominated by traders and analysts’ efforts to work the imminent round of fiscal stimulus into models and projections. It’s a feel-good party right now, even if it’s a subdued one, but I suspect that the positive vibes may not last long into January as nearly everyone agrees that the size of the stimulus is dwarfed by what is actually needed to keep major sections of the American economy—indeed, American life—afloat until we see the other side of the COVID-19 crisis. While the mood may not turn worrisome again this week, I think it’s something that smart traders should already be keeping an eye on.

With that in mind, let’s take a brief look at the shortened week ahead.

US Economic Data to Watch

Wednesday, December 30 at 830am EST // Chicago PMI (Dec)

[consensus exp.: 56.6 // prev.: 58.2]

With most trade desks running light and precious little else on the economic schedule for this week, a higher percentage of trader/market attention will go to typically second-tier data points such as the more important regional activity indices. After an outsized spike in September of this year, the Chicago PMI indicator has been steadily sliding back towards 50.0 and is expected to continue that track this week. Slowing economic activity is more or less priced into market expectations for the next few weeks, but with thin liquidity a worse than expected print, seen as a prelude to worse national numbers to come, could spook markets back into a more risk-off stance that likely bids gold prices higher than the US Dollar.

Thursday, December 31 at 830am EST // Initial Jobless Claims

[consensus exp.: +830k // prev.: +803k]

Last week’s unexpected decline in Initial Jobless Claims was a positive surprise for the US labor market’s outlook, but one that analysts are not expecting to repeat itself. A bounce back above 825,000 this week will ensure that the four-week trendline will remain above 800K well into January, before we see any tangible effects from the middling fiscal support signed into law Sunday night. As with the midweek PMI data, in a very quiet week a sharp tick higher in new unemployment claims could tip market sentiment back towards the risk aversion that has boosted gold and other safe havens in recent weeks.

And that’s how the shortened week lays out ahead of us, traders. As always, I wish you all the very best of luck in your markets in the final days of 2020; It has been…a year. I’ll look forward to seeing you all back here just before the turn of the year for our market-week wrap up.

Gold Price Chart

More articles from John Moncrief