Good morning, traders. Welcome to our preview of the week ahead in macroeconomic data for the precious metals and currency markets.

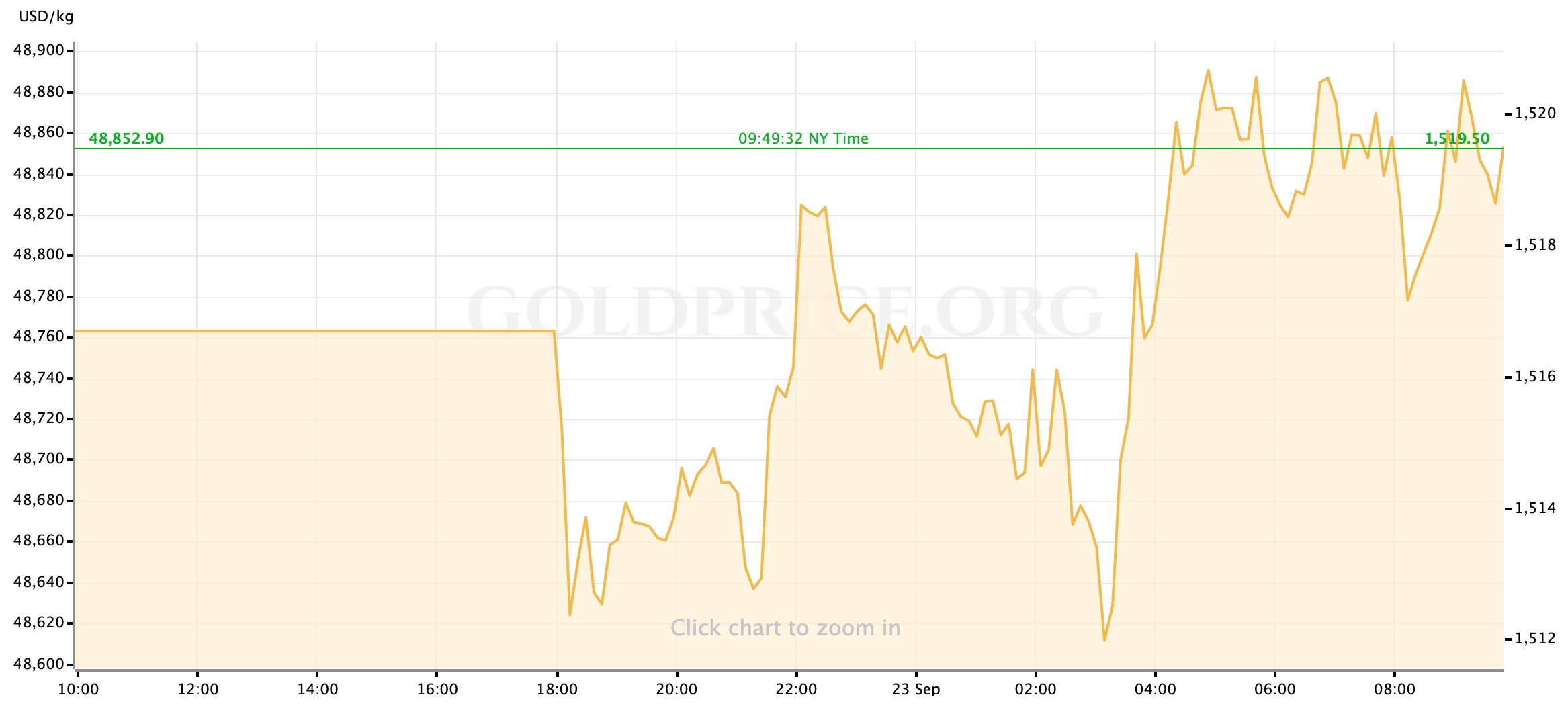

Gold is trading higher this morning, near $1520/oz, after initially gapping lower at Sunday evening’s open; silver prices have started the week strongly as well, trading around $18.45/oz.

While the initial selling pressure on gold yesterday evening was a result of global investors regaining their risk appetite as over the weekend both the US and China corrected initially ugly reports about the Chinese trade delegation returning home early than planned. I suspect that wary investors will still maintain a little bit of Friday afternoon’s caution, as there has been no stepping back the President batting away the possibility of an interim deal.

That story will certainly be the top focus for us in the headlines this week; as the actual data calendar is fairly light until Friday, I expect those kinds of developments to be a key driver of safe haven assets like gold and the Dollar this week. In the early hours of the morning however, it was concerns about the European economy that drove gold prices higher. Data reported that German manufacturing fell at the fastest rate in a decade, while the PMI for the Euro Zone as a whole unexpectedly felt to 50.4.

Along with those stories, we (along with the rest of the market) will be shifting our attention to interpreting the Fed’s outlook and probably next moves. As you’ll see shortly, what this week lacks in hard data in more than makes up for with a crowded FOMC dance card.

Let’s take a look.

US Economic Data to Watch

FedSpeak This Week

As expected, there’s a deluge of public appearances by FOMC members this week in the wake of last Wednesdays rate-cut. And, honestly, that’s great. With the most recent cycle of central bank meetings wrapped up, we’re moving into the next without the clearly laid forward path that we’ve had for most of the last quarter; thanks in large part of the picture of a fractured FOMC that was painted by last week’s votes and projections. Hopefully, the sheer volume of FedSpeak over the next few days will give us some representative commentary from the different camps within the Fed and allow us to reckon which data points for the economy the next FOMC decision will be dependent on. As always, these are my best bets at meaningful commentary, but you can get the complete schedule from the Fed’s website.

Monday, September 23: New York Fed President John Williams (FOMC voter) (9:50am EDT); San Francisco Fed President Mary Daly (11:30am); St. Louis Fed President James Bullard (FOMC voter) (1pm)

Wednesday, September 25: Chicago Fed President Charles Evans (FOMC voter) (8am); Dallas Fed President Robert Kaplan (7pm)

Thursday, September 26: Dallas Fed President Kaplan (9:30am); Fed Vice Chair Richard Clarida (FOMC voter) and SF Fed President Daly (11:45am); Minneapolis Fed President Neel Kashkari (2pm)

Friday, September 27: Philadelphia Fed President Patrick Harker (1pm)

Tuesday, September 24 at 9am EDT // Case-Shiller Home Price Index (July)

[consensus expectations: +2.2% YoY // previous: +2.1%]

Case-Shiller has been a reliably reliable indicator that the housing market in the US remains solid and based on the performance of other housing price indices for the summer there’s no reason to suspect that will change.

Wednesday, September 25 at 10am EDT // New Home Sales (Aug)

[consensus exp.: +3.3% MoM // prev.: -12.8%]

New Home Sales, on the other hand, have been more volatile but ultimately still supportive of the idea that things are still moving along steadily in the later stages of the economic cycle. Last month’s print was rough, and so the expectation is strong for a mean reversion. It would take a big miss—roughly the size of last month’s—to move the market this week, but without much on the data calendar before Friday it’s worth keeping an eye on.

Thursday, September 26 at 8:30am EDT // Initial Jobless Claims

[consensus exp.: +211k // prev.: +208k]

Friday, September 27 at 8:30am EDT // Personal Income & Spending (Aug)

[personal income consensus exp.: +0.4% MoM // prev.: +0.1%]

[personal spending consensus exp.: +0.3% // prev.: +0.6%]

Even the FOMC has made note of how important consumer spending is in this stage of the US economic cycle, and I suspect it’s a metric that Fed officials will rely on in assessing how the American economy is doing as we head into the end of 2019. With that in mind, we can pretty safely assume that an unexpected drop in data like Personal Spending towards 0% would shake the Dollar (at least in the immediate term) and push gold and other safe haves higher.

Friday, September 27 at 8:30am EDT // PCE Price Index (Aug)

[core PCE consensus exp.: +1.8% YoY // prev.: +1.58%]

[headline PCE consensus exp.: +1.4% YoY // prev.: +1.38%]

Last week’s sudden spike in oil prices, had it persisted (or should it return,) would’ve created more obstacles for those members of the Fed who are pushing a more dovish stance, by ratcheting up inflation in the economy through higher energy prices. While that possibility has faded for now, recent reads of PPI and CPI inflation have both moved higher, suggesting we’ll see the same moderate but meaningful increase reflected this month in PCE, the “Fed preferred” measure of inflation.

If higher inflation lessens the likelihood of further interest rate cuts from the Fed, expect that to be reflected in the market by a stronger US Dollar and weaker gold prices; the opposite would of course be expected should we see a pull-back in inflation.

Friday, September 27 at 8:30am EDT // Durable Goods Orders (Aug)

[consensus exp.: -1.2% MoM // prev.: +2.1%]

Analysts this month seem to be anticipating a month-over-month drop in Durable Goods Orders as a result of the summer’s weakness in the industrial sector as well was growing negative pressures put on US manufacturing by the ongoing trade conflict with China. From the point of view of the gold charts, I expect that a print close to expectations won’t have much of a market impact; a miss to the downside has the potential to drive some Dollar-selling and safe haven buying, while a stronger number than expected might bring a relief rally in the Greenback and risk-on assets.

And that is our week ahead. I wish you the best of luck in the markets this week, traders; and I’ll see you all back here on Friday for a recap of the macroeconomic week.

Gold Price Chart

More articles from John Moncrief