Happy Friday traders. Gold prices are up for the week, as high as $20 above the lows at time of writing. Quite a positive turn, all things considered.

So, what kind of week has it been?

This week has been very back-loaded for gold traders. After spot prices spent the first half of the week flirting with new lows beneath $1270/oz, Thursday and Friday’s gold trading—spurred on by some quietly concerning data on the US Economy—drew a decidedly upward trajectory that has lead to a break back above $1285.

Monday Markets Quiet as the Easter Holiday Tails-Off

Monday’s trading session was a net-loss for gold markets amid a quiet and calm environment that carried over from last week. With the majority of European traders offline in the morning due to the Easter Monday holiday, there was a relative glut of dollar bulls in the markets for the US Greenback and correlated assets so the brief extension of spot prices towards $1280/oz that we saw in the early Asian session Sunday night was sold off in an orderly fashion.

As is typical, Monday was a mostly bare day in terms of macroeconomic data with the one exception being the March assessment of Existing US Home Sales. Gold prices were provided a little bit of a tailwind on the release, as the month-over-month sales shrank more than 1% deeper than consensus expectations. Ultimately however, with a bland market backdrop the move failed to create enough momentum to pull gold prices out of what would become a very flatly-traded range for the rest of the session.

Strengthening Dollar Applies Pressure to Gold Prices

Tuesday was similarly sparse day on the macroeconomic calendar, but one that saw gold prices making a round-trip below $1270/oz resistance and back up again, as more traders came back online following the Easter Holiday Weekend, beginning with a sharp sell-off at 8:30am EDT that coincided with a strengthening US Dollar:

#USD holds resistance near monthly highs, with buyers yet to provoke a push beyond the 97.50 level. #Gold prices, on the other hand, are breaking down to fresh 2019 lows.Get your #TechnicalAnalysis from @JStanleyFX here: https://t.co/sTdmNtKCk6 #BreakoutorFakeout $GLD pic.twitter.com/bl1MC0ZgfE

— DailyFX (@DailyFX) April 23, 2019

The New Home Sales data for the month of March, which spiked to the highest level in over a year, put a bit of a dent in gold spot’s rebound from the floor at $1267, but prices for the yellow metal would manage to reclaim $1270 by late morning. Afternoon trading would when remain fairly flat for the remainder of the session with little in the way of relevant market news or data. An Asian trading session marked by the return of selling pressure (and another probe below $1270 in the spot markets) would be followed by a rebound in the European morning session towards $1275/oz.

Gold Markets Get A Breather Mid-Week, Solidify Support

The gold market seemed to find it’s footing on Wednesday. After making some very pointed threats toward the 200-day moving average in European and early US trading, a calm calendar day and slumping yields on US Treasuries helped to steady spot prices back above $1272/oz and staged another (still unsuccessful) run at $1280.

Even after pulling back from heavy resistance mid-morning, the gold market maintained a level around $1275 for the remainder of the session.

As Jobless Claims Normalize and Markets Question Manufacturing Health, Gold Rebounds

As did seem to be the trend for this past week, gold prices had another challenging run in the Asian markets through to the European morning session—likely due to a discouraging week of news and data out of the major global economies leading to Dollar-positive trading. Still, the yellow metal’s price-per-ounce in spot markets held onto the solid base built in Wednesday’s trading and was well positioned heading into US trading for Thursday.

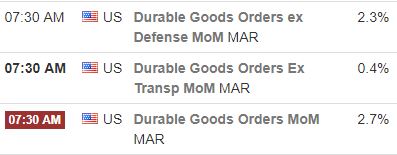

The morning’s US economic data was a bit of a mixed bag from a gold or US Dollar trader’s perspective. The headline number for Durable Goods Orders in March, reached an 8-month high, and the measurement ex-defense spending did as well; but the data Durable Goods data was nearly flat month-over-month when the volatile transportation component was stripped-out.

Overall, a somewhat conflicting report: the headlines, so to speak, are indicative of a still-growing US manufacturing sector and, by extension, economy. Still seeing that “core” number so close to flat demonstrates that the lion’s share of that expansion in March was driven by aircraft orders, for which Boeing has created a degree of uncertainty, and autos; a sector vulnerable to the current administrations combative trade stance that might soon put more of a strain on the industry. We can’t say that this is definitely problematic but using this data we also can’t feel confident about the near- to medium-term. I think you saw that reaction in gold markets as price action was back-and-forth immediately following the release, and then gold prices ultimately began their move north that would continue throughout the trading session.

Released at the same time Thursday morning, we finally saw the anticipated snap-back in Initial Jobless Claims as the measurement saw its biggest week-to-week uptick since 2017. It’s likely that traders’ and algos’ knee-jerk reactions to the number drove the gold market’s pop to some degree, but under examination—and taking the recent trends into account—this was still very much an “everything is fine” print and shouldn’t set the table for anything meaningful in metals markets.

Concerns About Underlying US Growth Increase, Gold Surges to End the Week

Friday’s report on GDP in the US for the first quarter and the US Dollar and metals market reaction to it follows the same thread as the Thursday report on Durable Goods Orders. Once again, the flashy headline number was not just positive but strongly above expectations as the first assessment of Q1 GDP arrived at +3.2% growth when analysts were expected something much closer to 2%. In a vacuum, this should be a strong buy signal for the US Dollar and headwinds for more risk-off assets like gold.

But, like Thursday’s data, a look just beyond the surface shows more concerning data, as measurements like private sales suggest an economy that it’s still decelerating.

Headline GDP was much stronger than expected in the first quarter. But final private sales, a measure of the underlying pace of growth, suggests an ongoing slowdown.https://t.co/QGxbBaoJ1V pic.twitter.com/4hTOnG1u6Z

— Ben Casselman (@bencasselman) April 26, 2019

To determine which data points markets are more interested in, you only need to look at your gold charts: at the time of writing, the yellow metal is looking at an $8/oz gain as the US Dollar slumps.

As we head towards the weekend, baring any nasty surprises through the afternoon, this may prove to be a more constructive week for gold pricing in the near-term than anyone suspected based on how quiet the markets have been recently.

Next week our calendar will be much busier, with heavy hitters on deck: PMI for the manufacturing sector, the all-important jobs report on Friday, and Wednesday’s FOMC meeting which is expected to be relatively quiet but still important for metals and currency markets.

Until then, traders, I hope you enjoy your weekends and I’ll see you back here on Monday for a look at the week ahead.

Gold Price Chart

More articles from John Moncrief