Good morning, traders; Welcome to our market week preview, where we take a look at the economic data, market news and headlines likely to have the biggest impact the price of gold this week and beyond, as well as market prices for silver, the US Dollar, and other key correlated assets.

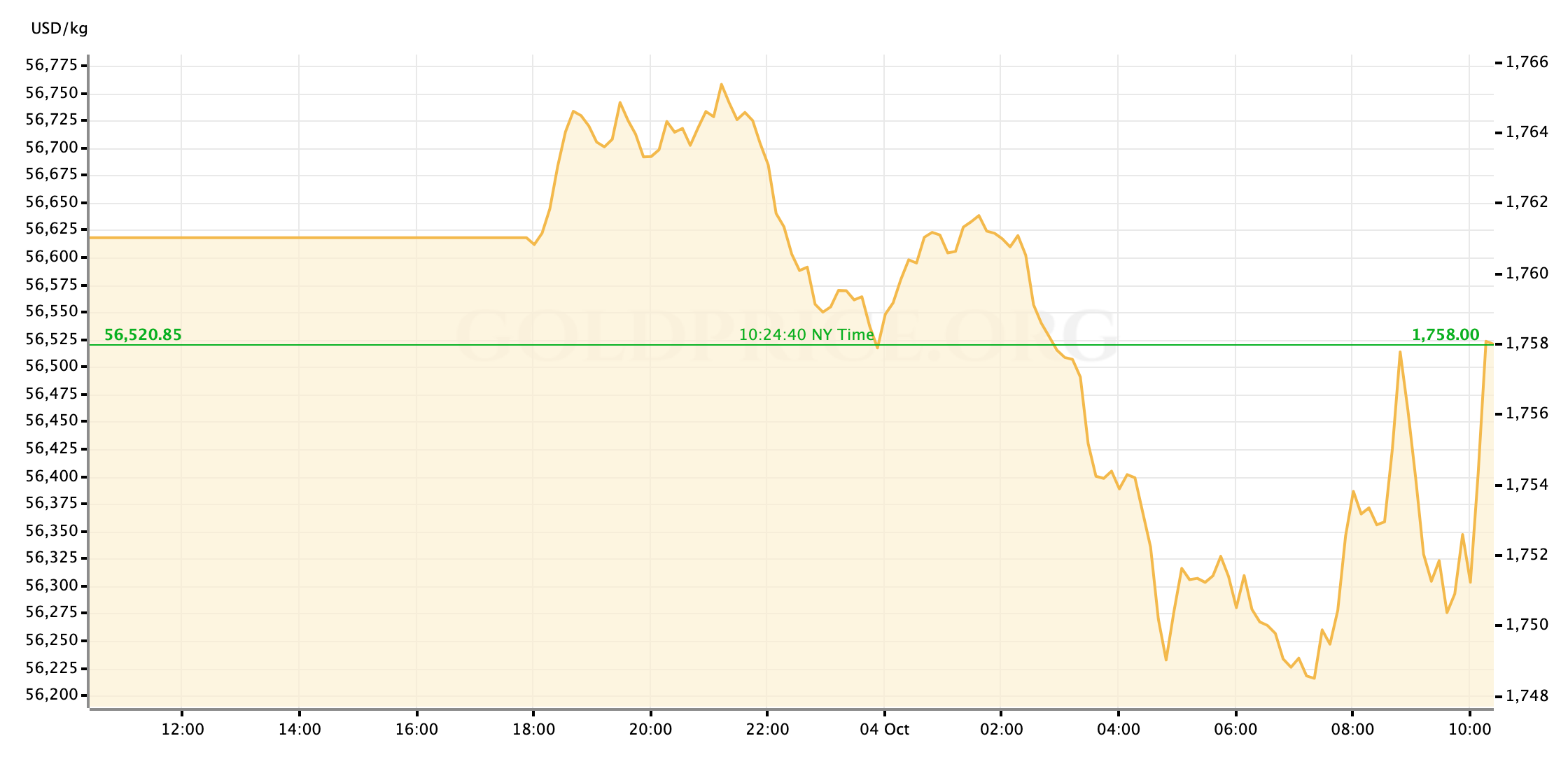

Following some up-and-down charting through the overnight sessions and pre-market hours in the US, gold prices are trading roughly on par with Friday afternoon’s closing prices, maybe solidifying what gold bulls will hope is a platform from which to advance this week ahead of the September Jobs Report on Friday.

The troughs for gold since the start of this week’s trading have pared with surges in US Treasury yields, particularly a failed bid by the 10-year yield to rise back above 1.5%. Clearly, then, gold spot may continue to be tightly tied to the US bond market this week, just as the last.

For now, let’s take a look at the rest of the calendar ahead.

US Economic Data to Watch

Wednesday, October 6 at 815am EDT // ADP Employment Report (Sep)

[consensus est.: +430K // prev.: +374K]

Particularly over the course of the last year it seems, the relevance of this monthly report on private payroll growth in the US economy (for gold or Dollar traders, at least) comes less from gaining real insight into labor market conditions present or future, and more from simply being aware that there is often general market volatility to be expected if the number misses above or below expectations. Whether or not a surprising number will actually correlate to a different NFP number than expected on Friday, or whether or not the volatility is a result of actual investor sentiment or just automatized algo-trading based on headlines, doesn’t ultimately matter. Just be aware that there may be some volatility around your positions on Wednesday morning.

Thursday, October 7 at 830am EDT // Initial Jobless Claims

[consensus est.: +350K // prev.: +362K]

We mentioned it in last Friday’s wrap: the weekly-reported Jobless Claims numbers have been sticky since unexpectedly rising at the end of August. This doesn’t necessarily imply that we’ll see another concerning NFP read for a second month, and this week’s read itself will probably be overshadowed as investors position for Friday’s Jobs Report; but, should September’s labor market data disappoint again, that will add focus to these higher-frequency reports heading into the November Fed.

Friday, October 8 at 830am EDT // September Jobs Report

[(NFP) consensus est.: +470K // prev.: +235K]

[(unemployment) consensus est.: 5.1% // prev.: 5.2%]

Friday’s is the last full labor market report that will be released before the November FOMC meeting, and as such will be the most “accurate” view the committee will have to factor into their assessment of whether the broader US economic recovery has become strong enough to allow the Fed to start tapering-off some support mechanisms. A better-than-expected number—which is certainly possible, given that we may see a snap-back from August’s disappointing read—can be expected to put some extra downward pressure on gold prices while boosting the Dollar; The view being that it would essentially lock-in the November taper. Even a roughly as-expected NFP number might do the same, at a gentler pace.

How markets will react to another miss to the downside is tougher to predict, because it’s unclear from today whether or not that might draw the Fed back from making a move next month after all. Most likely, a disappointing payrolls number will be more about reverberations through the market in the week (or so) that follows than any acute price action immediately following the print. Investors will first need time to parse the report and develop their own expectations for “what it means,” and then will closely watch any Fed commentary next week to judge how the FOMC views the matter. All of this to say: Should NFP disappoint again, the first reaction in the gold market is unlikely to be the reaction.

FedSpeak this Week

Last week’s appearances by FOMC officials suggested the relevant participants are mostly in-line with the current view that November’s meeting will be the appropriate time to begin tapering the central bank’s supportive asset purchase program, a first step in “normalizing” monetary policy. This week’s slate, which is really just two appearances to comment on fairly wonky topics should stray from the pattern; It’s next week’s FOMC-member commentary, reflecting on the key Jobs Report due this Friday, that will be of more interest.

There is another FOMC-related story that should be mentioned as a potential point of volatility or uncertainty in Dollar and Dollar-correlated markets: developing reporting on high-level Fed officials making (usually profitable) trades in personal accounts that could be seen as “front-running” Fed decisions and data that they had privileged early access to. The latest turn came at the very end of last week, with the report that Fed Vice Chair Richard Clarida made some questionable trades the day before Chairman Powell publicly announced some of the Fed’s pandemic policy actions.

It would be hard to say how—of even if, really—this narrative might impact US financial markets, because it’s tough find an analog for this happening before. As is often the case, then, the best practice for gold traders will be to keep an eye on the developing headlines this week.

And that’s how the week lays out ahead of us, traders. As always, I wish you all the very best of luck in your markets in the coming days, and I’ll look forward to seeing you all back here on Friday for our market-week wrap up.

Gold Price Chart

More articles from John Moncrief