Happy Friday, traders. Welcome to our weekly market wrap, where we take a look back at these last five trading days with a focus on the market news, economic data and headlines that had the most impact on gold prices—and may continue to into the future—as well as the charts for silver, the US Dollar and other key correlated assets.

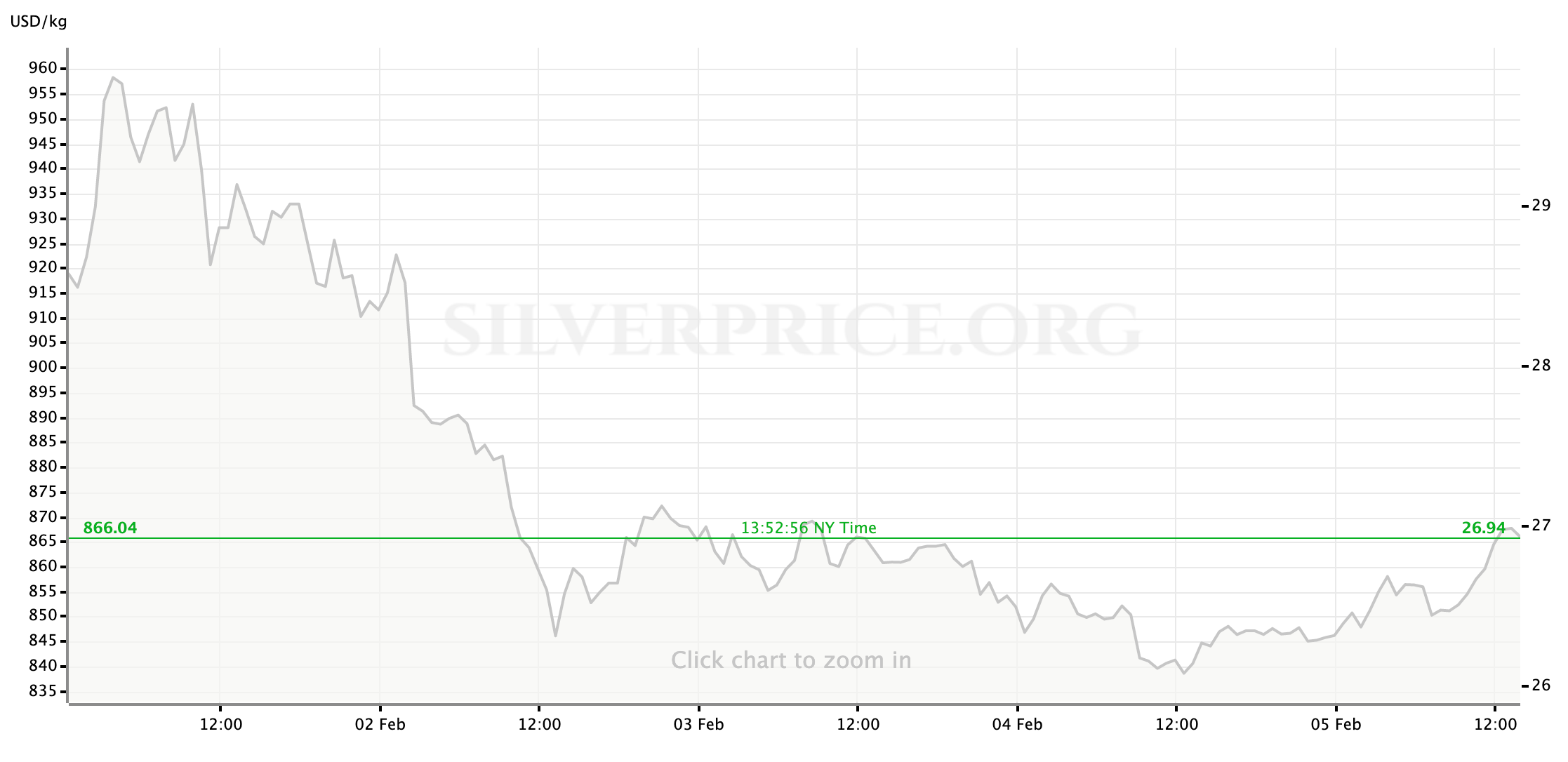

Spot prices for both gold and silver are both considerably lower than where they began the week. While some retracement from Monday’s highs was always anticipated once the acute spike in silver prices lost momentum (which happened fairly quickly,) investors’ risk appetite has moved steadily higher with every day of trading this week and so the precious metals have been subject to continual pressure as positions continued to rotate out of safe havens and into yielding risk assets.

So, what kind of week has it been?

Gold & Silver Moderated After the Weekend’s Spike in Silver Demand

Gold’s path through Monday’s trading after our weekly preview piece went up was a flat one; Relative disinterest in pushing the yellow metal in either direction kept spot prices consistently close to $1860/oz. Silver prices, after failing to break above $30/oz in the morning, were more subject to gravity. On Monday at least, silver maintained enough buying interest to hold off any steep drops but ultimately was unable to close the session above $29.

As US investors fired up for the week it became clear that, by whatever combination of implied regulatory action and “natural” market forces, the berserker volatility of last week was already being corrected out of the market. Investors and managers jumped hungrily back into the equities markets and bought the major indices higher: US stocks had their best day in 2 weeks of trading, led by a 2.5% gain in the NASDAQ 100.

Enthusiasm for Silver Waned Quickly, While Investors Poured Back into Equity Risk

By the time that overseas markets re-opened on Monday evening, it was clear that the retail trading frenzy of the prior week had faded considerably, and with it many more “traditional” investors’ will to be cautious. No surprise then that, as we predicted, the weekend surge in silver demand and futures pricing (which, it has to be said, may or may not have been primarily driven by Reddit-based trading groups as was initially reported) was a flimsy rally at best. Precious metals fell under pressure from a return of general risk appetite, influenced not only by a presumed return to “normal” but also the same horses that have been jerkily pulling the carriage for weeks now (US fiscal stimulus incoming! Vaccines rolling out!)

While the bleed was slow during Asia’s trading session, the arrival of Europe’s trading centers brought even more risk appetite into the markets as the US Dollar advanced and riskless US Treasury paper sold off, driving the benchmark 10-year yield back above 1.1%. The drag on gold and silver proved too much for support and both fell sharply at the start of the trading day in Europe and later in the US. At the start of cash trading for US stock markets on Tuesday, gold spot prices were scraping to cling to $1835 while silver challenged support at $27/oz. The intraday patterns of the precious metals diverged there—gold would once again trade mostly flat through the day while silver traders, trying to discover the white metal’s true price inputs, saw a more volatile chart—but both would close Tuesday’s book of business within touching distance of those same levels. US stock markets, meanwhile, carried on with the feel-good rally, boosted by another round of strong earnings reports.

Spot trading for gold held the yellow metal in another modest range all the way through the overnight session, into and through Wednesday’s book of business in the US. $1835/oz proved a reliable level of support, but as the Dollar held its lines and a climbing 10-year yield continued climbing away from 1.1% gold was given little room to rise. Silver again endured some choppier trading with $27 having become stubborn resistance against holders’ last effort to press the weakly-backed rally further.

Despite the optimistic signal of a steepening yield curve, the risk-on rally across the world’s largest equity markets briefly slowed during Wednesday trading in the US, perhaps because investors were reassessing the possible over-extension of some gains in specific sectors or even individual stocks; retail and tech stocks were the main drags on the benchmark indices and fell hard enough to see the NASDAQ 100 close at a loss although the S&P managed to just eke out a gain.

Thursday’s Trading Saw the Market Appetite for Risk Reach New Highs as Gold Temporarily Fell Below $1800/oz

Weekly trends accelerated on Thursday, for both risk assets and safe havens. Overnight trading between US sessions saw the Dollar strengthen further as Asian and European markets reflected the hesitant patterns of US investors on Wednesday; the US 10-year’s yield continued pushing closer to 1.15%. Subject to these headwinds, gold and silver struggled to hold serve through the core hours of Asian markets but the start of European trading once again ratcheted up the pressure and both metals weakened ahead of a much sharper drop at the start of US trading. Ahead of Thursday’s economic data reports, gold sat limp near $1815/oz while silver at retraced to $26.50.

As Thursday’s US session opened and went on, it would become clear that Wednesday’s break from supreme confidence in the markets’ rise was only blip. Coinciding with—and probably accelerated to some degree by—better than expected weekly jobless claims data, the US Dollar surged once again while safety hedges like gold saw the bottom of demand drop out: While silver fell sharply to $26/oz. gold prices quickly collapsed through support at $1800 before finding buyers roughly $15 lower. Both metals were cheap enough to recover somewhat during the trading day, but silver still could only retake $0.25 of its losses while gold struggled to find any support above $1795.

US stock markets picked up the rally after Wednesday’s brief pause; Big and small names across the board rallied on Thursday, driving the S&P 500 to yet another “record” and a closely watched section of the US Treasury yield curve pulled up to its steepest level in more than 5 years. Investor optimism in the US and abroad, as Thursday made clear, is the driving force in markets to begin February.

Traditional Safe Havens Like Gold Are Higher on Poor Labor Market Data, but Equity Markets Continue to Thrive on Risk-Appetite and Investor Hopes

Investor optimism in running at such a high level, in fact, that (at the time of writing) on Friday it has continued right on through a really ugly Jobs Report for the month of January. Despite kicking the week’s final trading day off with this:

Economists ‘hope’ the disappointing jobs report was the low point for 2021 https://t.co/DjaPiFfCy3 by @ewolffmann pic.twitter.com/5WIHZoAn2m

— Yahoo Finance (@YahooFinance) February 5, 2021

US stocks continue to move higher, en route to the market’s best week since November 2020. It seems counterintuitive on the surface, but there were actually some rumblings mid-week that recent economic data was looking too good (because we can’t just have nice things, I suppose) and might slow the rush to pass the Biden Administrations massive stimulus package on which so much of the market’s optimistic outlook hinges; A dour reality check in the form of an anemic labor market recovery then, in that context, should serve to reinforce the urgency of the need to flood the US economy with fiscal spending.

Although risk assets are continuing to have a great week, gold and silver have made gains on Friday as well. Gold prices were briefly bid higher in the European session and made a test run above $1800/oz before losing steam. Later, they were much more reactive to the ugly non-farm payrolls number and, as the historical record would expect, jumped sharply higher. This time the thick line at $1800 has once again become support, allowing the yellow metal a platform to build higher. At the time of writing, near mid-day, spot prices look well bid at $1810/oz to close the week. Silver has enjoyed a rebound as well; whether it will make another attempt at breaking $27 is yet to be seen.

Next Up

On the next economic calendar most attention will be focused on an updated read for consumer inflation, and then a round of congressional testimony from Fed Chair Jerome Powell. We’ll also be tracking whether or not the narratives and outlook around US fiscal stimulus and the global vaccination effort continue to support so much risk taking in financial markets.

For now, traders, I hope you can get out and safely enjoy your weekend for the next couple of days. After that, I’ll see everyone back here on Monday for our preview of the week ahead.

Gold Price Chart

More articles from John Moncrief