Good morning, traders; Welcome to our market week preview, where we take a look at the economic data, market news and headlines likely to have the biggest impact the price of gold this week and beyond, as well as market prices for silver, the US Dollar, and other key correlated assets.

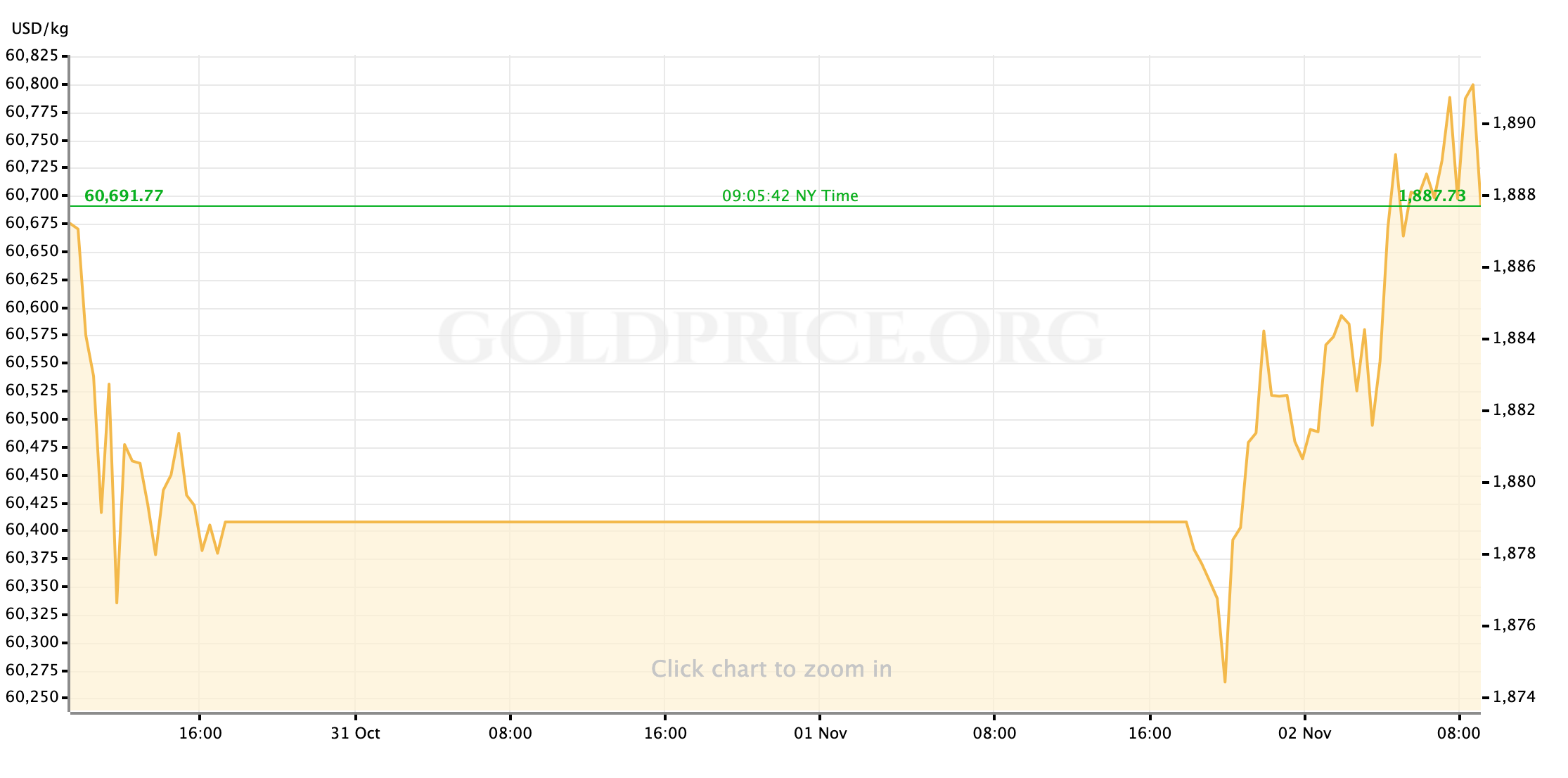

Gold prices have risen overnight and into this morning, alongside Asian and European equities. At the time of writing, gold spot prices are trading close to $1890/oz again and silver has retaken at $24 handle; the Dollar has weakened.

Investors and managers this morning are taking note of another drop in oil prices, with WTI barrels selling for below $35. This suggests to me that if gold’s momentum turns bad later in the day, there’s a good chance that the yellow metal’s drop could be a steep one.

Below, you’ll find our usual breakdown of the top tier economic data on order for the week. This week, of course, is incredibly unusual: it will pack an FOMC meeting in with a monthly Jobs Report that could be key to projecting the US economy’s health through the end of 2020; and it does it all on a week where both released could be overlooked by markets because of a monumental US federal election ending midweek. And the biggest unknown that this week’s Election Day kicks up is that we can’t say for certain when the important results will be known and certified: it’s fairly rare in recent US history for the presidential election to be wrapped and settled by midnight of the first day; But will markets have a reliable outcome to trade around on Wednesday night? Friday morning? I genuinely can’t follow the logic of anyone saying they know one way or the other for sure. And that makes it very tough for me to outline for our readers where metals prices might go on, say, Thursday morning—so I won’t make much of an attempt at that this week.

I’ll say this explicitly here, mostly to avoid being redundant in the notes that follow: with Covid-19 cases surging to new and frightening highs across the US, and Britain joining with many other major European nations in re-instating lock downs for the winter, the near-term outlook for the US economy is not very positive, regardless of who will sit in the Oval Office at the end of January. While I believe that, at this point, that pessimism is priced into most major assets, anything other than big upsides surprises from this week’s data will only underline these concerns. In a more “normal” week, I would tell you that I’d be expecting to see uncertainty rise in markets with each one of these data points, and that it would be a battle between the US Dollar and other core safe haven assets like gold all week to see where investors and managers feel more confident about hedging their risk exposure. Unfortunately, as we can’t make much of an educated guess whether the US elections will send the Dollar to the moon on Wednesday or crashing back to the ground on Thursday, there isn’t a way for me to both be honest and to make reliable, directional calls on metals prices this week.

The best advice I can give traders this week—and every week, really—is to trade smart, trade safe, and keep your head on a swivel.

With the self-indulgent preamble out of the way, let’s take a look at the week ahead.

US Economic Data to Watch

Monday, November 2 at 10am EST // ISM Manufacturing Index (Oct)

[consensus exp.: 55.8 // prev.: 55.4]

The vital thread connecting this week’s economic data is that it’s important primarily in terms of allowing us to mold a near- to medium-term outlook for the end of 2020 into 2021. The elections this week will, with the possible exception of Friday’s jobs report, overshadow any kind of sustained market reaction to better, worse, or “just right” numbers.

With that said, US manufacturing activity is expected to hold its tepid pace just north of the 50.0 breakeven for the first month of Q4. Looking ahead, this doesn’t leave the activity index a lot of cushion in the ever more possible event that the US economy is pushed back into some version of a shutdown to combat Covid-19 in a winter without a vaccine; So, this sets the stage for some continuing uncertainty into the end of the year.

Wednesday, November 4 at 815am EST // ADP Employment Report (Oct)

[consensus exp.: +650k // prev.: +749k]

As I said, it’s very possible that by this time on Wednesday morning we will still not have a certified result either in the Presidential race, or in any number of congressional races that will determine the balance of the House and Senate. In that scenario (or even just one in which we have firm results but markets have exhausted themselves overnight,) it’s tough to imagine October’s private payroll numbers lading with much impact. (Re)Hiring in some sectors post-spring looks like it has continued through October, so the ADP number is expected to come in well enough historical averages but slower than the recent pace, reflecting our recent concerns about the health of this “recovery” independent of the coronavirus resurgence we’re seeing today nationwide. I do want to point out that although the published “consensus view is at +650k, I’ve seen a number of reliable teams whose prediction is for a weaker number-- below 600k in some cases.

Wednesday, November 4 at 10am EST // ISM Non-Manufacturing Index (Oct)

[consensus exp.: 57.5 // prev.: 57.8]

ISM’s read on economic activity in the services sector should remain at least slightly higher than in the manufacturing sector (released on Monday.) This lines up with the broad trends in the US economy over the last decade, and that extra cushion will come in handy should another round of economic lock downs come to American metro areas as retail and hospitality sectors would once again fall under the greatest amount of strain.

Thursday, November 5 at 830am EST // Initial Jobless Claims

[consensus exp.: +735k // prev.: +751k]

Weekly jobless claims should continue falling and pulling the 4-week average—which is finally below 800k—down with it. In any Jobs Report week, the initial claims number tends to get overlooked and that certainly could be the case on this of all weeks. I suppose it’s possible though, if the most important seats in the US federal elections are certified by Thursday morning with a result that markets appreciate, that an as-expected (or better) initial claims number could boost that wave a stability and encourage greater risk appetite.

Thursday, November 5 at 2pm EST // FOMC Interest Rate Decision

[No relevant changes to monetary policy are expected.]

Falling on an odd Thursday due to the elections, it’s likely that this week’s FOMC meeting, statement, and press conference will go down as the least talked about, and least impactful of 2020; And all by the Fed’s design. If history is any indicator, while it’s generally expected that the Fed will start offering more specific forward guidance soon, there’s virtually no chance that Chairman Powell & Co. will attempt to squeeze that into the same week as a presidential election.

Friday, November 6 at 830am EST // October Jobs Report

[(NFP) consensus exp.: +600k // prev.: +661k]

[(Unemployment rate) consensus exp.: 7.7% // prev.: 7.9%]

Looking at Friday, which feels roughly 45 miles and seven weeks away from Monday morning, it becomes somewhat more likely that we could have—for the purposes of financial markets—settled election results. If that’s the case (big if, huge if,) we may see risk-sensitive assets like gold or the Dollar react in a mor normal way to the October Jobs Report. I don’t know that this is a likely scenario, but smart traders will be prepared for it.

As with October’s private payroll growth (to be released on Wednesday,) the headline non-farm payrolls data is expected to represent that Americans are continuing to return to work at a moderate pace following the spring’s pandemic-driven lock downs. However, the data should also reflect the concerning slowdown in the pace of (re)employment which comes at same time as the end of any government stimulus for consumers and a worrying slide backwards towards record highs in Covid-19 infections.

All of this, however, is likely priced into the markets’ outlook for the US economy through the end of the year; I don’t expect there’s much chance that we see Friday’s jobs report spook markets and investors (any more than they already will be.) But it’s possible that, if markets have begun moving on from the immediate impact of the 2020 election, as stronger than expected report on the labor market could see risk appetites return to the market. Based on recent trends, that could look like the Greenback’s pressure on gold prices easing at the end of the week.

And that’s how the week lays out ahead of us, traders. As always, I wish you all the very best of luck in your markets in the coming days, and I’ll look forward to seeing you all back here on Friday for our market-week wrap up.

Gold Price Chart

More articles from John Moncrief