Good morning, traders. Welcome to our preview of the first full week of trading in 2020. As always, we’ll be talking a look at the macroeconomic data items on this week’s calendar that have the most relevance for traders of gold and other precious metals, as well as the US Dollar and its major trade partners.

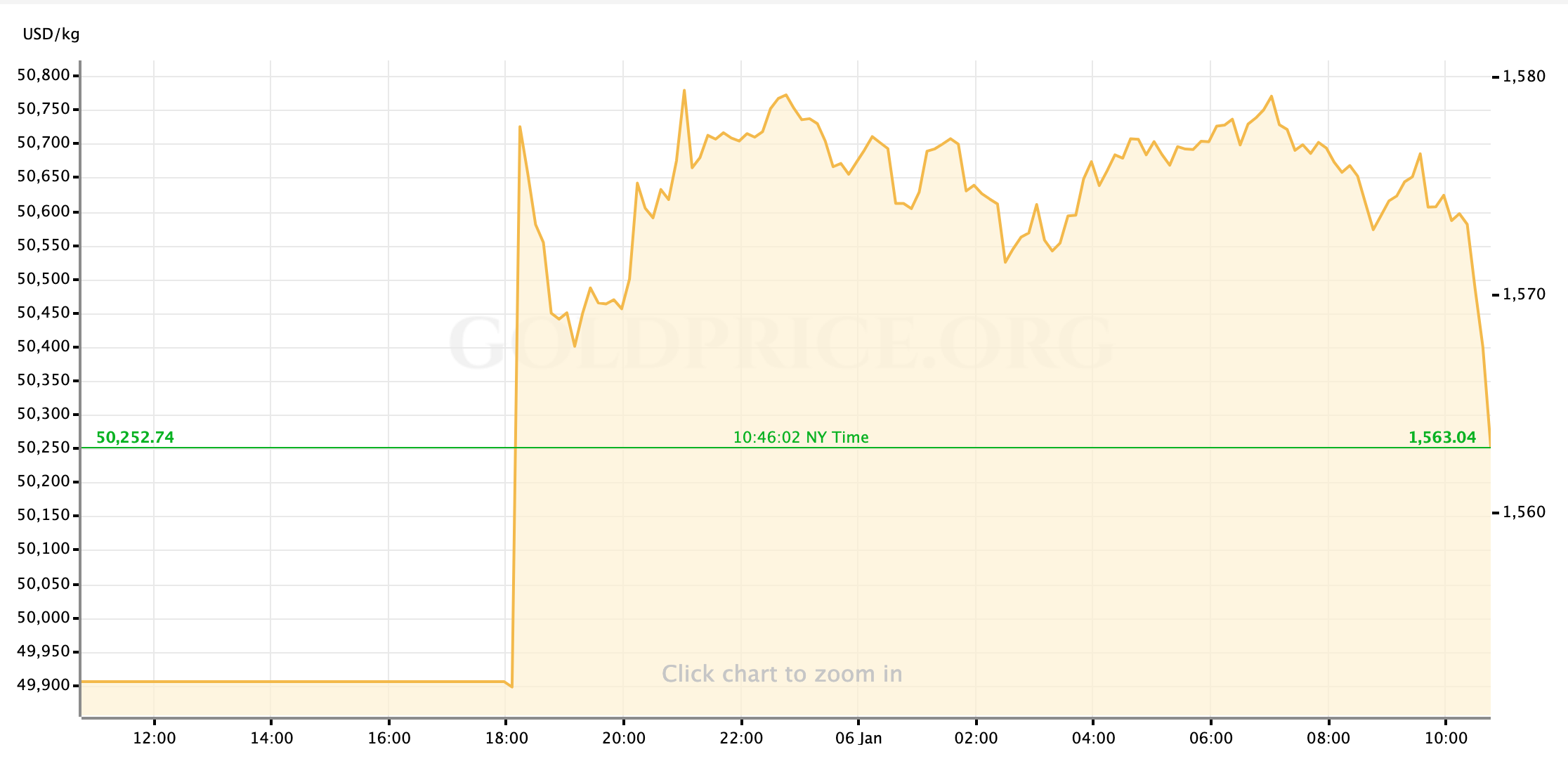

This morning, we are seeing the new week begin broadly as we ended the last one: with pervasive market turmoil driven by the escalation of tensions between the US and Middle Eastern nations—a group that now includes American ally Iraq as well as Iran. Global equities have been pushed lower along with the dollar while the flight to safety has boosted Treasuries and of course gold.

The yellow metal has traded as high as a 7-year high since markets reopened for the week, although at time of writing we are seeing an optimistic rebound in US equity markets that has pulled gold spot prices back to a still-elevated level around $1565/oz.

The slate of economic data this week is fairly light before Friday’s Jobs Report, so that only emphasizes the fact that the core driver for gold and US Dollar trading this week will be the evolution of the tension around the Middle East. Markets will also look for the next step in US-China trade negotiations: there are reports that the US President’s announced January 15 signing date for a “phase one” agreement is moving forward, but still no official confirmation from the Chinese delegation.

US Economic Data to Watch this Week

Tuesday, January 7 at 10am ET // ISM Non-Manufacturing PMI (Dec)

[consensus expectation: 54.5 // previous: 53.9]

The consensus estimate is for service sector PMI to move slightly higher in December’s data, but given last week’s downside surprise in the manufacturing-focused variant I’m inclined to say it’s more likely that the number remains unchanged at best. A slight pullback from the prior month probably doesn’t make any big moves show up on the gold or Dollar charts; but the closer we get to the contractionary zone below 50.0, the bigger the swing to safety might be. After all, even amid global markets being roiled by US-Iran tension on Friday morning the poor ISM showing sent gold prices straight up by a another $4-5/oz.

Wednesday, January 8 at 8:15am ET // ADP Employment Report (Dec)

[consensus exp.: +160k // prev.: +67k]

Not for the first, time, the blockbuster Non-Farm Payrolls number in last month’s Jobs Report was preceded by a much lower than expected private payroll number from ADP. It highlights this data point as one that you should always be paying attention to at release (because in the event of a big improvement/disappointment relative to expectations, the Dollar and gold markets will usually move on it,) but should not inform your expectations for (or positioning ahead of) Friday’s labor market data. With that said, the strong November NFP data leads most observers and analysts to believe we’ll see a healthy rebound in ADP for December.

Thursday, January 9 at 8:30am ET // Initial Jobless Claims

[consensus exp.: +220k // prev.: +222k]

The long-term trend of weekly jobless claims does seem to be calming after some odd November/December volatility, which will make it a fairly inert data point once again. Still, it does seem to be settling slightly higher—closer to 225k than 200k—so don’t ignore it in 2020.

Friday, January 10 at 8:30am ET // December Jobs Report

[(NFP) consensus exp.: +158k // prev.: +266k]

[(unemployment) consensus exp.: +3.5% // prev.: +3.5%]

Analysts generally anticipate a vanilla Jobs Report of December—non-farm jobs added is expected to moderate from last month’s blowout to a still very strong level around 150k; the headline unemployment rate is expected to remain nailed to the floor at 3.5%. In that scenario, while there always is some computer-driven trading around the release of such an anchoring data point, markets will react mildly: we’ll see some strength from the US Dollar, maybe enough to slightly weaken gold’s spot price.

In the event that the data is a disappoint though, we should be aware of this question: How sensitive will the Fed be? A week ago, I’d have said that the FOMC seemed so (rightly) certain of their decision to hold interest rates, likely through all of 2020, that one poor Jobs Report or set of bad inflation data would be written-off as “transitory” without effecting the policy path. But now, with global markets reacting badly to the US ratcheting Middle East tension higher, would the Fed feel compelled to step in much sooner? We won’t get the answer to this on Friday, but it’s something macro traders should be trying to solve for over the next few weeks.

FedSpeak this Week

Last Friday’s FOMC discussion minutes really solidified the assessment of a Fed that is firmly committed to the current pause, but also aware of global pressures on the US economy (to which we now need to add “tension in the Middle East” and the possibility of inflated energy prices that may come with it.) With that in mind, there will be some added attention paid to this week’s docket of public commentary by Fed officials, on the chance that they may shine some light on how the FOMC might react to the downside risks to the economy posed by the US’ airstrike last week. It’s a short list this week but there are still some appearances worth noting:

Thursday, January 9: Federal Reserve Vice Chair Richard Clarida (FOMC voter) (8am ET); New York Fed President John Williams (FOMC voter) (11:30am); Chicago Fed President Charles Evans (FOMC voter) (1:20pm); St. Louis Fed President James Bullard (FOMC voter) (2pm)

And that’s how this potential volatile week lays out ahead of us, traders. I wish you the very best of luck in your markets this week, and an excellent start to 2020. I’ll see everyone back here on Friday for our recap of the week in in economics and the metals markets.

Gold Price Chart

More articles from John Moncrief