Good morning, traders! Welcome to another preview of the macroeconomic calendar for the next five trading days with a focus on what’s relevant to the precious metals and Dollar markets.

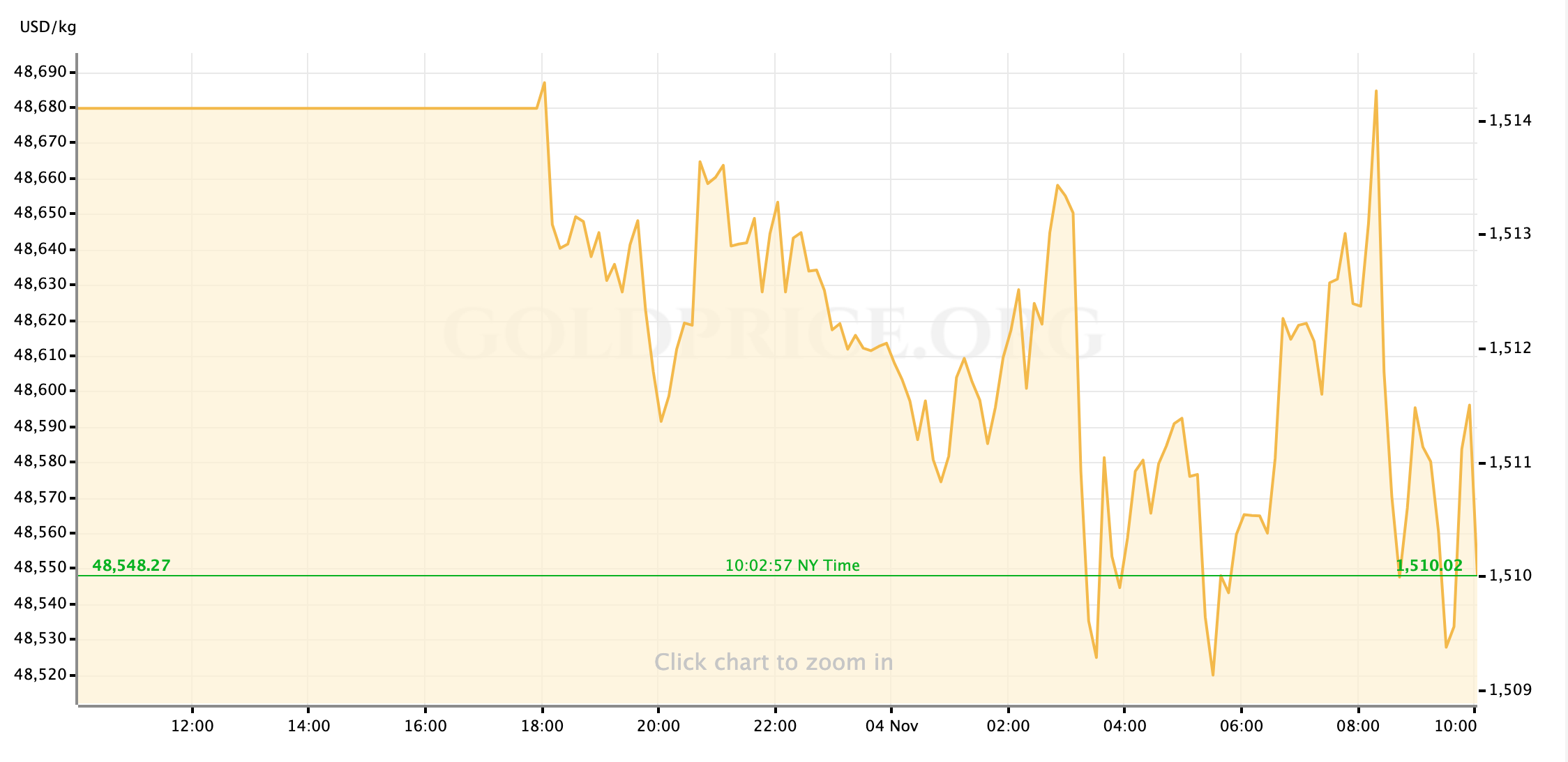

Gold and silver prices this morning are slightly lower than Sunday evening’s open, but the yellow metal is still sitting near to $1510/oz in the spot markets at time of writing. This is in spite of rising yields on US Treasuries and a healthy start to the week for equities, driven by—you guessed it—mostly unsubstantiated claim that US-China trade talks are going well.

We will, of course, keep tracking news around the negotiations this week as well as impeachment proceedings in Washington; with Brexit’s focused turned towards new UK General Elections, those will likely be our main sources of market-moving headlines this week apart from what’s on the calendar.

Speaking of which, let’s take a look at the week.

FedSpeak this Week

Right away we’ve got the usual flood of public remarks and appearances by Federal Reserve officials on the heels of an active FOMC meeting. Whereas the last month’s parsing focused on how committed the opposing camps within the Fed were to either cutting a third time or holding rates, this time around the general view is of a committee that is largely on board with a data-dependent pause. Between now and December 10, our focus should be on clarifying which economic data sets the FOMC apply the heaviest weighting to (presumably that’s still the monthly jobs report and both the PCE and CPI measurements of inflation; manufacturing sector data as well) and we’ll also want to puzzle-out just how high the committee has raised the bar for eventual rate hikes.

Few Fed appearances will noticeably impact markets, but it can be difficult to predict which ones ahead of time so, as usual, I’ve tried to trim this week’s list down to the ones with the higher odds of being worth our time:

Monday, November 4: San Francisco Fed President Mary Daly (non-voter) (5pm ET)

Tuesday, November 5: Dallas Fed President Robert Kaplan (non-voter) (12:40pm ET); Minneapolis Fed President Neel Kashkari (non-voter) (6pm)

Wednesday, November 6: Chicago Fed President Charles Evans (FOMC voter) (8am ET); New York Fed President John Williams (FOMC voter) (9:30am); Philadelphia Fed President Patrick Harker (non-voter) (3:15pm)

Thursday, November 7: Atlanta Fed President Raphael Bostic (non-voter) (7:10pm ET)

US Economic Data to Watch

Monday, November 4 at 10am ET // Factory Orders (Sep)

[consensus expectations: -0.5% MoM // previous: -0.1%]

While this isn’t typically a data point that I’ve been watching closely, as I mentioned above, it’s possible the manufacturing sector could be watched closely by the data dependent Fed through the rest of year and into early 2020. The initial read on Durable Goods Orders for September showed a decline, so it’s reasonable to expect something similar in general Factory Orders for the same month. What would shake the Dollar and send gold prices higher would be a deeper than expected drop here, which would likely coincide with an ugly correction to the finalized Durable Goods data, due out at the same time this morning.

Tuesday, November 5 at 10am ET // ISM Non-Manufacturing PMI (Oct)

[consensus exp.: 53.6 // prev.: 52.6]

Manufacturing PMI, which printed last Friday morning after the Jobs Report, was a mixed bag for analysts and Dollar traders. Yes, it was an increase over the month prior after consecutive monthly declines, but not by quite as much as the consensus expected and the metric remained in contractionary territory. Tuesday, the service sector PMI won’t have the cover of a jobs report (or end of the week exhaustion) to distract from whatever impact it might have. That said, the minor lift in Friday’s data does suggest we could see the same on the non-manufacturing side, pulling the number away from the sub-50.0 range that signals contraction. If we do see service sector PMI fall further, however, that could be a clear risk-off signal with little else happening on Tuesday.

Wednesday, November 6 at 8:30am ET // Non-Farm Productivity (Q3)

[consensus exp.: +0.9% QoQ // prev.: +2.3%]

Like Factory Orders, I haven’t often put a marker down to observe quarterly productivity data. But, with the unemployment rate nailed to the floor and the longer-term trend in jobless claims still flat, I think analysts and investors are going to start looking deeper into some second-tier signals about the labor market in hopes of predetermining the Fed. The +0.9% print expected for the third quarter is right around the average mark for this economic expansion so far. I’m not sure, honestly, how deep of a miss would sink the Dollar and rally gold prices, or how big of a beat would do the opposite. But I think it’s worth having on our calendar for now, just in case.

Thursday, November 7 at 8:30am ET // Initial Jobless Claims

[consensus exp.: +215k // prev.: +218k]

Friday, November 8 at 10am ET // University of Michigan Consumer Sentiment (Nov. prelim.)

[consensus exp.: 96.0 // prev.: 95.5]

Similar metrics for consumer sentiment in the US have be flagging a little bit lately, so I think the expectation for this month’s UofM number to be flat-ish to October (much less, a slight improvement) is a vulnerable one. If the read drops closer to 90.0 on Friday, I think that will already be a little bit priced into risk markets; but if sentiment shows a strong improvement, the Dollar strength that follows might accelerate the profit-taking we usually see on the gold charts each Friday.

Global Economic Data to Watch

Monday, November 4 at 9:30pm ET // Royal Bank of Australia Interest Rate Decision

[no changes to monetary policy expected]

I’m going to continue keeping an eye on the RBA’s commentary, as the closest reliable proxy to the Chinese economy. There are fairly low odds of another cut this time out, and in fact the central bank’s Governor has made clear arguments against the need for further easing in recent comments. Of course, most of those remarks came before we saw just how rough the economic waves are in Hong Kong between the democratic protests and the ongoing US-China trade dispute, so I’ll be interested to see if the RBA has any new concrete concerns about the Asian economy or how that might bleed into the global system.

Thursday, November 7 at 6am ET // Bank of England Interest Rate Decision

[no changes to monetary policy expected]

This one is mostly just a check-in, to see if the BoE is raising any flags now that the Brexit deadline has been kicked farther down the road. With the focus on a General Election on December 12, I expect this meeting to be pretty dry and quiet.

And that’s out week ahead, traders—certainly a quieter one than last week on paper but given the narratives in play around economic growth and geopolitical tension around the world, there’s always potential for some fireworks in the gold and currency markets. I wish you the best of luck out there this week, and I’ll see you back here on Friday for our market recap.

Gold Price Chart

More articles from John Moncrief