Happy Monday traders, welcome to your look at the macroeconomic week ahead as it pertains to gold markets.

This morning gold spot price is trading roughly where it had closed last week’s session on Friday, but that doesn’t quite tell the whole story. As a result of a rash of tweets from the President of the United States which warned that tariffs on Chinese goods will increase substantially this week if better progress is not made in US-China trade talks, the Sunday evening market open saw gold prices gap-up more than $5 as the Greenback and US Equities floundered.

Those tailwinds failed to hold through the NY morning start however, and at time of writing we see gold for immediate delivery trading around $1279/oz with hopes of re-taking previous support at $1280. My best guess is that yesterday evening’s dramatic trading was the result of headline-focused algos “reacting” to the news flow, but as more adaptive human traders came online and remembered that we’ve done this dance before to no real effect, they were happy to take the arbitrage opportunity and “correct” equites and US Dollar prices which in turn have driven gold lower again.

With a particularly light economic calendar, it’s clear that re-heated tension around the US-China trade talks will be a dominant story for us this week and we’ll elaborate on that from a gold trader’s perspective a bit when we discuss reporting on the trade deficit; still, there are other unrelated economic releases later this week that matter, and culminate with April inflation data on Friday morning.

US Economic Data to Watch

Thursday, May 9 at 8:30am EDT // Producer Price Index (Apr)

[consensus expectation: +0.2% MoM // previous: +0.6%]

Energy prices held pretty strong for most of April, which should feed into a month-over-month increase in producer price inflation. Still, we won’t be expecting a large increase as—let’s all say it together with the Fed—Inflation. Remains. Muted.

This gauge of producer prices shouldn’t do anything to alter that narrative. The consensus number implies a year-over-year rate just above 2%, so as long as we arrive in that same neighborhood, I don’t see this being a mover for the gold market. Caveat Spectator, of course: a month-over-month number close to or above 1.0%, or a yearly mark nearer to 2.5% could take some wind out of gold’s sails by suggesting increased odds that the Fed returns to the hiking cycle.

Thursday, May 9 at 8:30am EDT // Trade Balance (Mar)

[consensus exp.: -$51.1bn // prev.: -$49.4bn]

The last two months have seen the US trade deficit unexpectedly decrease, theoretically letting some pressure off of the Washington side of US-China trade talks. For March, economists are again expecting a slight expansion of the deficit, but after the tweets coming out of the White House on Sunday evening it’s hard to imagine even a third-consecutive reduction “taking the pressure off.”

As I’ve said before, it’s really not easy to take a view on gold markets based around these trade talks. For one, while we’ve been regularly told of late that negotiations are going well (at least from the US side,) I still can’t confidently handicap what the resolution will look like to either side. For another, there are so many gold-influencing cross currents tied to this trade dispute—the US Dollar and Chinese Yuan, as well as the perceived health of their respective economies—that even if we knew the exact state of play at the end of these talks it would still be a Gordian Knot-level complication to discern whether it would imply higher or lower gold prices.

The short version: as a gold trader, or someone otherwise exposed to price risk in the gold market, be cognizant of how this macroeconomic story develops; but maybe avoid the temptation to take any positions based specifically on a US-China outlook.

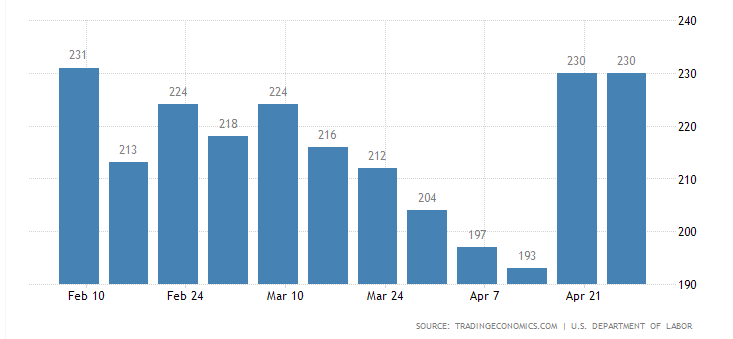

Thursday, May 9 at 8:30am // Initial Jobless Claims

[consensus exp.: 220k // prev.: 230k]

I felt compelled to post the recent chart here because what amazes me the most about the last month is not the historically low weekly claims numbers, we saw but the identical back-to-back prints. Expectation is for that number to pull back towards 200k a little bit and, to me, that seems totally reasonable from a trend standpoint.

Friday, May 10 at 8:30am EDT // US Inflation (Apr)

[core consensus exp.: +2.1% YoY // prev.: +2.0%]

[headline consensus exp.: +2.1% YoY // prev.: +1.9%]

At this point, and this environment could persist for the foreseeable future, inflation data for the gold trader is entirely about will it or will it not force the Fed to move off of the current interest rate target which the FOMC has said they’re comfortable to hold until they see the whites of inflation’s eyes. To repeat the familiar refrain: the suggestion that the Fed will raise rates again would be a drag on gold prices; the opposite being true for implied cuts.

In terms of the health of the American economic cycle, April’s inflation report is expected to be a positive signal, a return to both headline and core inflation running at the Fed’s 2% target. I don’t expect the data to have a lasting impact on markets however, as the market’s consensus expectations doesn’t imply seeing “the whites of their eyes” so much as “hey, is that something moving on the tree line?” and, really, it’s probably just the wind.

Fed Speak This Week

In last Friday’s wrap-up, I definitely said I was surprised at how sparse the calendar of public remarks from Fed officials looked this week given that we just had an FOMC meeting/statement. Turns out, I had just looked at the schedule before it was fully updated by the Fed and/or most banks! Below is the list of speakers (currently) scheduled for this week, selected according to which I think might include some meaningful text or discussion, which actually makes up most of the macroeconomic calendar on this sparse week. As usual, it’s tough to say which engagements, if any, might provide some moments of insight that make waves in metals or currency markets but it’s always useful to at least be aware of them.

- Monday, May 6 at 9:30am EDT // Philadelphia Fed President Patrick Harker (non-voter)

- Tuesday, May 7 at 7am EDT // Dallas Fed President Robert Kaplan (non-voter)

- Wednesday, May 8 at 8:30 EDT // Fed Governor Lael Brainard (voter)

- Thursday, May 9 at 8:30am EDT // FOMC Chairman Jerome Powell (voter)

- Thursday, May 9 at 9:45am EDT // Atlanta Fed President Raphael Bostic (non-voter)

- Thursday, May 9 at 1:15pm EDT // Chicago Fed President Charles Evans (voter)

- Friday, May 10, at 10am EDT // New York Fed President John Williams (voter)

Global Economic Data to Watch

Wednesday, May 8 at 2am EDT // German Industrial Production (Mar)

[consensus expectation: -0.5% MoM // previous: +0.7%]

The German economy makes up the engine room of overall European growth, and the engine room of the Germany economy is their industrial sector; so the anticipated return of contraction in that sector (which would be the seventh negative change in the last 12 months) is problematic for the EU in a way that will likely shake the Euro currency lower on the news. The pass through to US Dollar (higher) and then to gold pricing (lower) shouldn’t be seismic but could have a larger effect if it comes at a time when gold spot is trading around vulnerable support levels.

Friday, May 10 at 4:30am EDT // UK Q1 GDP

[consensus exp.: +0.5% QoQ // prev.: +0.2%]

Like most top-line UK macro data these days, Q1 GDP this week serves primarily as a check-in on how much damage is being done—or implied for the future—by the protracted, Sisyphus-ian Brexit negotiations. In fact I’m only including it here for those of your who want to dig particularly deep into the currency movements than can underly gold strength or weakness: I don’t expect any kind of immediate movement in gold markets regardless of the outcome, but I think it will be a useful data point of those of us trying to assess the next turn in the Brexit saga—which will have something to say about gold pricing.

And that’s your week ahead, traders. As always, best of luck out there, and I’ll see you back here on Friday for a recap of the week’s events.

Gold Price Chart

More articles from John Moncrief