Hello traders, happy Monday and welcome to our weekly preview of the trading week with a focus on the economic data, news flow, and market narrative that looks most likely to have an impact on the price of gold as well as the US Dollar and other correlated assets.

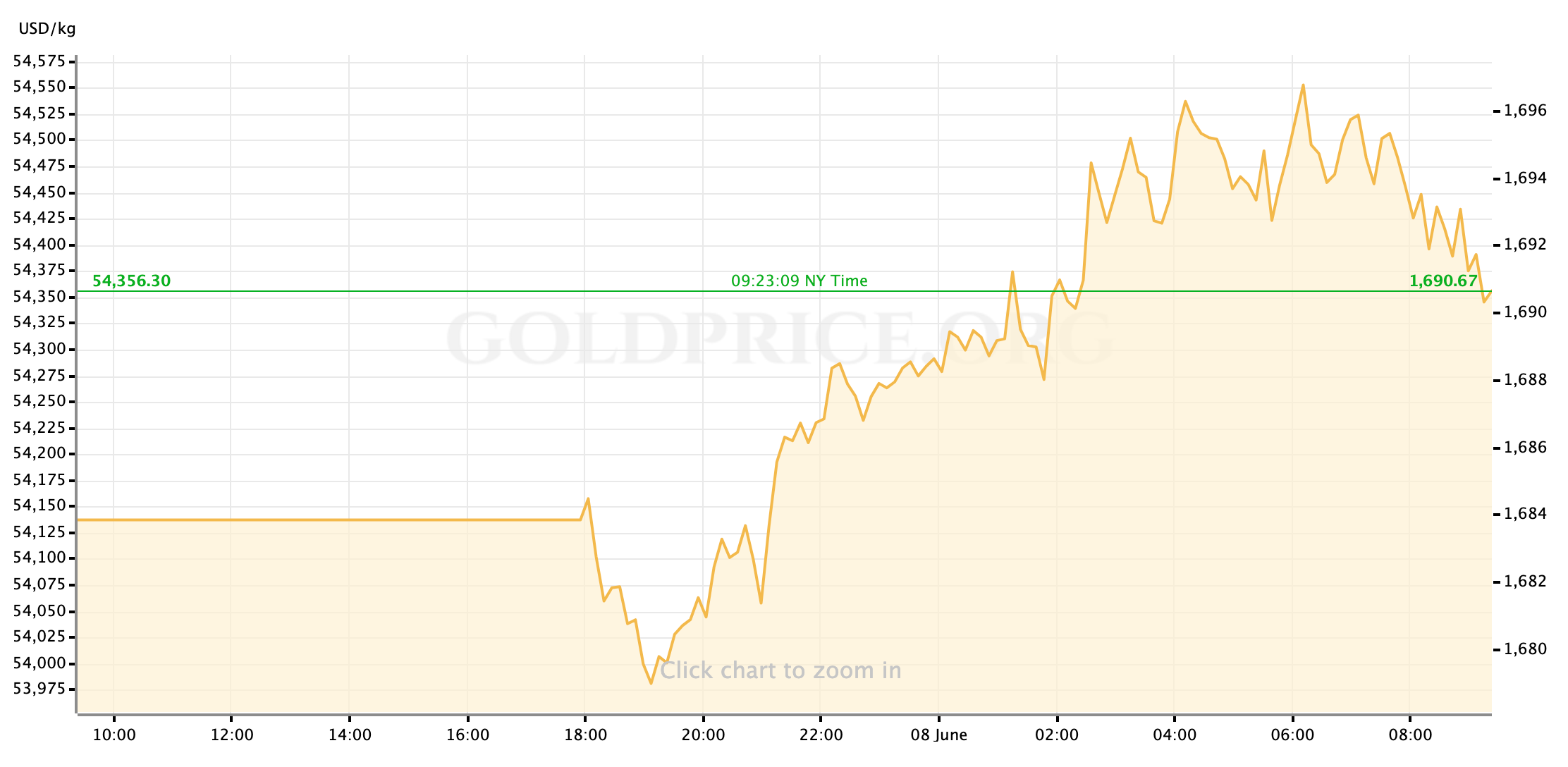

Gold prices are slightly higher this morning after steadily climbing throughout the overnight session to mark near $1690/oz in the spot markets ahead of the start of US stock market trading.

Whether the yellow metal can make a tangible recovery this week—and to what extent—will depend largely on how last week’s burst in risk-appetite carries on. We’ll also be looking out for headline risks around US-China trade tension, and the result of New York City entering “phase one” of its economic re-opening plans.

For now, let’s take a look at the important point on this week’s economic data calendar.

US Economic Data to Watch

Wednesday, June 10 at 8:30am EDT // Consumer Price Inflation (May)

[(core CPI) consensus exp.: +1.3% YoY // prev.: +1.4%]

[(headline CPI) consensus exp.: +0.3% YoY // prev.: +0.3%]

Looking at inflation rates from a month-to-month perspective, it seems the economists expect that the gradual steps towards reopening parts of the US economy which began in May will have done enough to halt the deflation we saw in April’s CPI numbers. In annual terms then, expectations are for both the core and headline CPI reads to match the prior month. In terms of the gold market, I’m not seeing much room for movement in prices. As suggested by last week’s big labor market data for May though, there’s some increased risk to the upside of economists’ predictions about the rebound in economic activity ahead of a real recovery; so while the weaker fuel prices that have suppressed headline inflation for several months still remain in play, be on the lookout for an upside surprise in core CPI which may add to the recent pressure on gold prices.

Wednesday, June 10 at 2pm EDT // FOMC Interest Rate Decision

[no change to monetary policy is expected]

There are extremely long odds for any change to interest rate policy coming out of this week’s FOMC meeting, but we’ll be looking at Chairman Powell’s press conference and at the quarterly update of the Fed’s Staff Economic Projections for signals that could be bullish for gold prices in the near- to medium-term. In the presser, I expect Powell to reassert the party line that the Fed will continue to act as needed to support the economy through and out of the current crisis (through ultra-low interest rates, among other operations.) The Chairman may also allude to the possibility of the Fed enacting some kind of yield curve targeting which NY Fed President John Williams and others have discussed recently. Both of these related stimulus policies should be generally supportive of gold prices in a low-yield environment.

Because Wednesday brings the first update to the Fed’s economic projections since the coronavirus crisis full took hold of the US economy, I think there’s possibly going to be some sticker shock as the FOMC meaningfully elevate their unemployment rate projections and make cuts to their outlook for inflation; the survey is also expected to project a flat rate path as far as the end of 2022. The downgraded economic projections may be enough to shock some risk-aversion into the markets in the immediate term, while the promise of ultra-low interest rates again suggests a positive outlook for gold prices.

Thursday, June 11 at 8:30am EDT // Initial Jobless Claims

[consensus exp.: 1,550k // prev.: 1,877k]

There were some clear concerns around last week’s jobless claims data, particularly the uptick in continuing claims, but the data was sandwiched between the surprisingly good ADP payroll data and May Jobs Report, so any signal sent into the market was unclear. This week, I think expectations are high for the initial claims number to continue dropping and I think any other negative surprised will be felt much more strongly in the market, boosting safe havens like gold.

Thursday, June 11 at 8:30am EDT // Producer Price Inflation (May)

[consensus exp.: +0.1% MoM // prev.: -1.3%]

There shouldn’t be a lot of trading action around Producer Price Inflation until we start to see a more energetic recovery in the US manufacturing sector; until then, we’re mostly keeping an eye on it to see that it’s moving (or at least not deteriorating) in step with consumer inflation, in hopes that the economic recovery is felt by American industry as well as the consumer. That’s expected to be the case this week.

Friday, June 12 at 10am EDT // Consumer Sentiment (June)

[consensus exp.: 75.0 // prev.: 72.3]

As the US economy continues to take its tentative steps towards re-opening, we’ll probably continue to see a tight feedback loop in the month consumer sentiment surveys: the sentiment data will be supported by the seemingly unstoppable rise in the stock market, and the stock market will continue to get a boost from strengthening consumer sentiment, and so on. Generally speaking, this will continue to be a point of monthly resistance for gold prices, but not a strong one.

Global Economic Data to Watch

Elsewhere in the world, the data calendar is fairly low-impact for our markets. In Europe we’ll mostly be looking out for headline risks as ECB officials will be giving public remarks following last week’s monetary policy meeting, and there will also be a Eurogroup meeting to discuss what could be a monumental stimulus package for the shared currency area. In Asia, the economic calendar is quiet with the exception of a read on Chinese inflation due Tuesday night; Chinese-produced economic data is generally taken with a healthy dose of skepticism, so don’t expect market movement here unless the data blows out in one direction or the other.

And that’s how the next five days lay out ahead of us. As always, traders, I wish you the very best of luck in your markets this week, and I’ll see everyone back here on Friday for our usual market wrap and recap.

Gold Price Chart

More articles from John Moncrief