Good morning, traders! Welcome to our weekly preview of the economic calendar and market narratives in the week just ahead of us. We’re coming in on Tuesday this week, following a bank holiday in the US and the UK as markets reopen for a shortened four-days of trading.

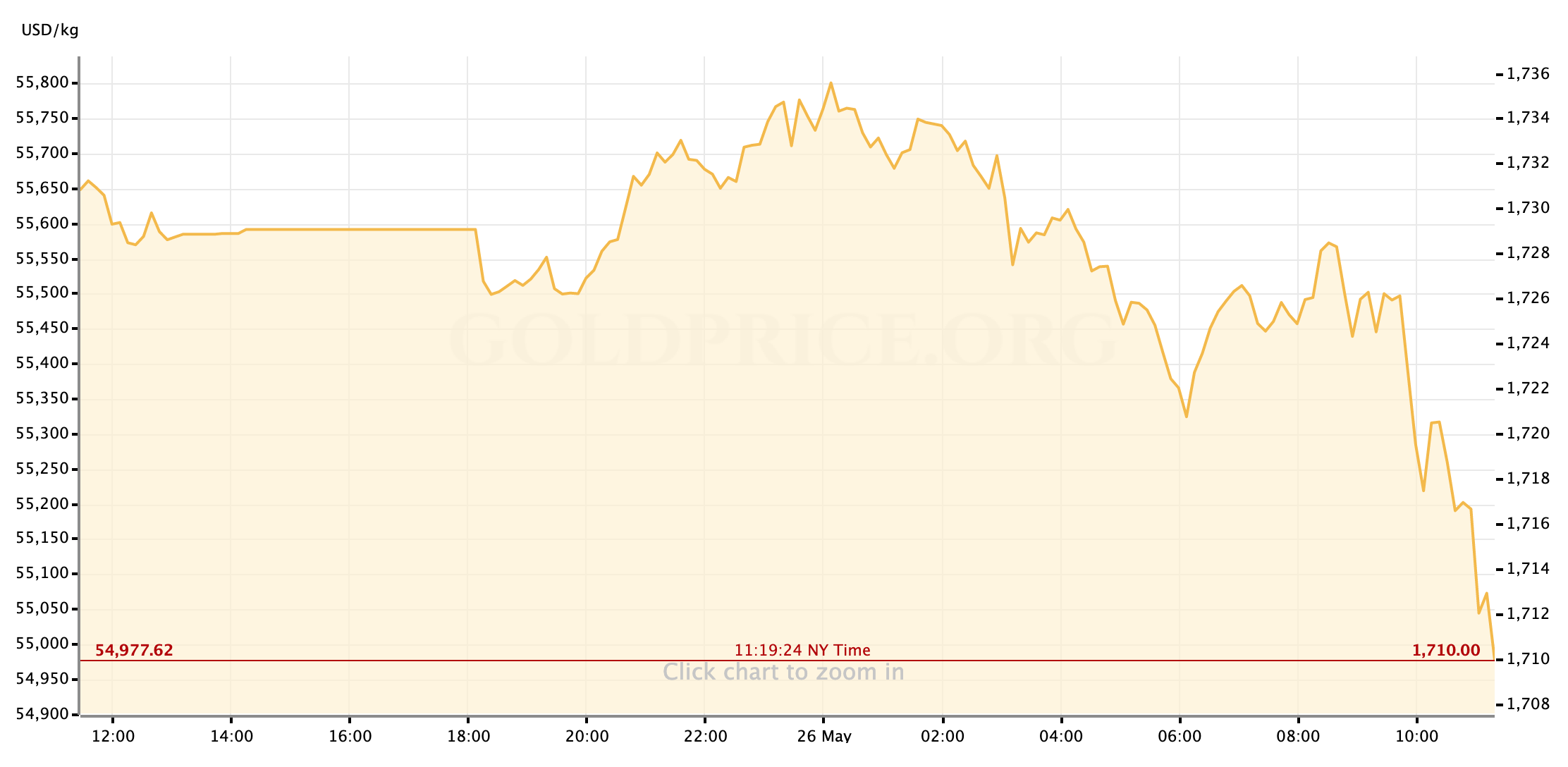

Gold prices are markedly weaker this morning following a very light Monday of global trading, and some mild support in the overnight sessions. The yellow metal has been sold-off alongside the major safe havens as US equities have surged higher from the open this morning. The general tone of global markets has been positive to begin the week, with investors and managers seeming content to look past the still-growing threat of a US-China trade war and instead trade on the optimism of economic “re-openings” continuing apace.

S&P 500 trades above 3,000 for the first time since March 5 https://t.co/6hYKUhWb74 pic.twitter.com/U8ttK8bjJw

— Yahoo Finance (@YahooFinance) May 26, 2020

We’ll continue to monitor the larger narratives of the tentative steps towards economic recovery, especially in the US, and the state of play between the US and China while the global effort to end the coronavirus’ spread continues. On the data front, here’s a look at what’s on our calendar for the next four days.

US Economic Data to Watch

Tuesday, May 26 at 9am EDT // Case-Shiller Home Price Index (Mar)

[consensus exp.: +3.4% YoY // prev.: +3.5%]

[actual: +3.9% YoY]

This week’s data calendar kicked off early today with a more developed looked at the housing market for the month of March, with the Case-Shiller report showing that housing prices continued to rise modestly year-over-year. The increase slightly beat analysts’ projections, but we can chalk that up to the difficulty of estimating what the impact of Covid-19 would be for the housing market in March when the economic shutdowns were still rolling out at different paces in different places. April’s data can be expected to reflect a more affected decline. Gold prices saw a slight tick downward around the release but given the larger macro issues in play markets were little changed.

Thursday, May 28 at 8:30am EDT // Q1 GDP (2nd Est.)

[consensus exp.: -4.8% QoQ // prev. Q1 est.: -4.8%]

The consensus estimate that I find in most places this morning calls for the second look at Q1 growth in the US economy to match closely to the initial try, which is fairly common in most quarters. I do think that, in this case, “unchanged” is a very optimistic projection. Given the general chaos around surveying businesses data throughout the US economy as the current Covid-19 crisis gripped America, and the issues of non-responses from businesses that were shuttered (temporarily or otherwise) specifically, I fall in the camp that’s expecting a considerable revision downward this week as those numbers are better resolved. Goldman Sachs’ team is calling for a nearly -2% QoQ revision.

Even a drop of closer to -1% would be well outside the norm; even with some level of expectation in the markets, I expect a (further) swing towards risk aversion. Once an initial burst of algo trading passes, the question will be whether investors make their big moves into USD and cash alone as we’ve seen before, or if the other major save havens like gold will rise as well.

Finally: this revision will be released at the same time as Durable Goods data as well as Initial Jobless Claims for the week, so there may be a lot of noise in risk and save haven markets, especially if the data present different views of the state of the economy.

Thursday, May 28 at 8:30am EDT // Durable Goods Orders (Apr)

[consensus exp.: -19.8% MoM // prev.: -14.7%]

Durable Goods will be some of the last middle-tier economic data we’re receiving for the month of April, and like most of the numbers for that month it’s going to be ugly with a nearly 20% decline in the headline orders category. While it’s certainly not good news for the US economy or investors, we have to assume it’s fairly well priced-in at this point. Given that, and the fact that Durable Goods data will print in a noisy Thursday morning for data, I’m not anticipating much action in the gold charts (or the yellow metal’s correlated assets) here.

Thursday, May 28 at 8:30am EDT // Initial Jobless Claims

[consensus exp.: +2,100k // prev.: +2,438k]

The downward trend is expected to continue in jobless claims this week, while still remaining catastrophically high above 2 million. There’s a lot of psychological sensitivity around this number, especially in this time. So, while I think it’s unlikely, if this number were to come in below 2 million—however slightly—that would probably force a risk-on surge into major markets and while I’ve pointed out that Thursday morning in very “noisy” from a data perspective, this would be the one to rise above the rest and set a tone of higher risk appetite for Thursday’s US session; most likely it would translate to strong headwind against gold.

Friday, May 29 at 8:30am EDT // PCE Price Index (Apr) // Personal Income & Spending (Apr)

[consensus exp. (core PCE): +1.1% YoY // prev.: +1.70%]

(headline PCE): +0.5% YoY // prev.: +1.32%]

[(personal spending): -12.8% MoM // prev.: -7.5%]

[(personal income): -6.5% MoM // prev.: -2.0%]

It’s unusual outside of the month Jobs Report, but we have a big Friday morning of economic data this week. The Fed’s tabulation of inflation in the US economy will take the expected damage for April, with the important “core” number falling to nearly 1%. The more volatile headline number will be brutalized by April’s disaster of a month for energy prices. As with a lot of April data, the hurt is mostly accounted for in current asset prices and I don’t expect risk appetite to be sensitive to PCE in the way it has been to labor market data.

Nor do I expect much movement off of Personal Spending and Income data this week, unless the Personal Spending number that we know is watched closely by the Fed beat expectations. As it stands, we’re expecting to see a much deeper pullback in spending vs. income, as higher-earning jobs were demonstrably less effected by the current crisis to-date, but the economic gloom as increased saving across the board. If the data shows that the vital US consumer was more resilient in April than expected, that would be a big boost to the outlook for a speedy economic recovery as major cities around the US reopen. Gold prices would likely weaken in that scenario, but the downside could be capped by a general increase in investment and boost to the broad commodities complex.

FedSpeak this Week

The steady schedule of public remarks and commentary from Fed officials will continue this week. Typically, by this point we’ve kind of exhausted the well of useful insight into the FOMC outlook and potential actions moving forward, but the feasibility and relative success of both the Fed’s own support actions and facilities as well as local authorities’ efforts to reopen parts of the US economy is being constantly updated. So, it’s actually nice that we’ve had regular check-ins to see where the voting and relevant non-voting members of the committee see the near- to medium-term monetary policy path going. Officials will likely continue to brush aside any talk of negative interest rates at this time, but we’ll pay attention for any other unconventional measures that might be brought forward.

Tuesday, May 26: Minneapolis Fed President Neel Kashkari (FOMC voter) (2pm EDT)

Wednesday, May 27: St. Louis Fed President James Bullard (non-voter) (12:30pm)

Thursday, May 28: New York Fed President John Williams (FOMC voter) (11am); Philadelphia Fed President Patrick Harker (FOMC voter) (3pm)

Friday, May 29: Federal Reserve Chairman Jerome Powell (FOMC voter) (11am)

And that’s how this shortened week lays out ahead of us, traders. As always, I wish you the very best of luck this week in your markets and I hope everyone stays safe. I’ll see you all back here on Friday for our regularly scheduled market wrap.

Gold Price Chart

More articles from John Moncrief