Good morning, traders. Welcome back to Monday, and a look at our week ahead in the gold market and related assets.

The economic calendar for this week is especially light and even has far fewer scheduled public appearances by FOMC officials than we typically see post-meeting. Heading into the weekend, my narrative this week was going to be about being vigilant during the week in regard to US-China trade relations as those seem likely to be the primary driver in an otherwise quiet week. I do think it’s important to keep your fingers on that ever-quickening pulse, but for the worst reasons imaginable I think (honestly, I hope) that Washington will have less time for launching trade salvos across the Pacific this week as the US grapples with the horrific terror attacks that were carried out this weekend.

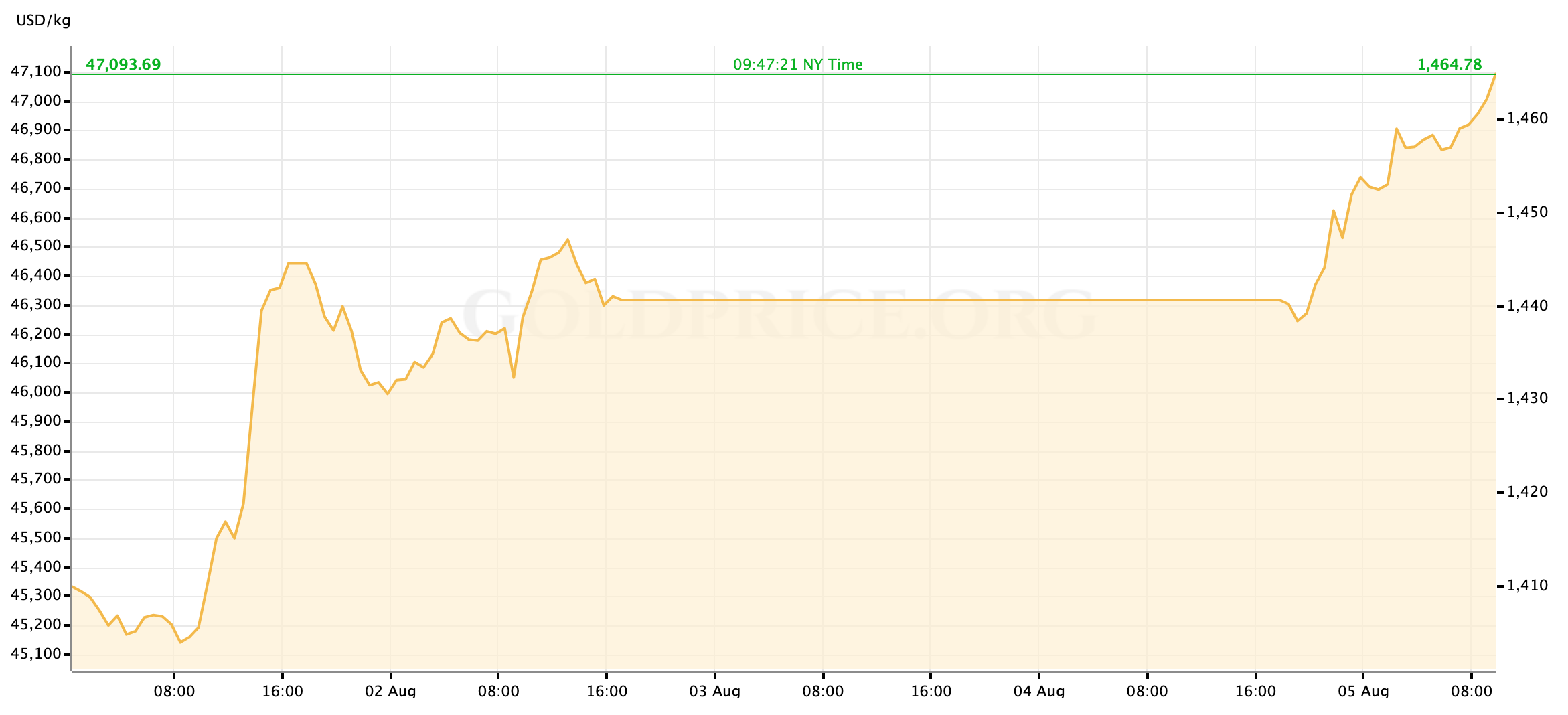

Gold is trading at a six-year high this morning, ticking at $1462/oz in the spot markets at the time of writing.

The powerful risk-off swing is driven mostly by battered equity markets continuing on the turmoil that characterized the end of last week with Donald Trump’s re-escalation of the trade war. Asian markets were roiled overnight as the Chinese Yuan fixed at its weakest level in more than a decade, signaling that among other combative measures China is no longer concerned with keeping the USD/CNY below 7.00 in an effort to cool trade tensions; the situation on the ground in the trade bulwark of Hong Kong also seems to be worsening. The equity weakness has passed through to the European markets and US futures, showing few signs of slowing. Gold has ridden each trade and headline higher, as the turmoil of the last fifty-something trading hours has fundamentally changed the landscape where some (myself included) were calling for no further monetary easing from the Fed.

Let’s take a look at a few points on the docket this week.

US Economic Data to Watch

Monday, August 5 at 10am EDT // ISM Non-Manufacturing PMI (July)

[consensus expectation: 55.5 // previous: 55.1]

While other survey measures of the manufacturing sector have been fluctuating over the last few months, the ISM’s index—historically the “best” of the metrics—has remained consistently low. And often time’s those arguing for a still-growing US economy say this trend doesn’t warrant as much concern because in this modern age America’s is now mostly a services economy. While the numbers bear that out to be true, they also show a services (“non-manufacturing”) sector that’s starting to lag as well. Given the market’s recent focus on the Fed, an as-expected print this week or a moderate beat probably doesn’t move gold or Dollar markets in a noticeable way; but a slip closer to the 50.0 line that divides expansion from contraction would fuel the push for a second rate cut in September and add a tailwind to gold prices.

Thursday, August 8 at 8:30am EDT // Initial Jobless Claims

[consensus exp.: +215k // prev. +215k]

Friday, August 9 at 8:30am EDT // PPI (July)

[consensus exp: +0.2% MoM // prev.: +0.1%]

Similar to Monday’s services PMI reading, producer price inflation has been trending downward since the spring and given investors current point of focus this data likely only impacts metals and major currency markets in the event that it comes in as a large miss to the up- or downside.

FedSpeak this Week

I’m actually surprised by how light the FedSpeak calendar is this week, although I suppose it’s due in part to the longer-than-usual span between meetings with summer ending. The committee members, I suspect—the Chairman most of all—are probably glad for the opportunity to adjust their language about the outlook following the President’s trade-war salvo just after last week’s FOMC meeting.

My feeling is that Evans’ media interviews on Wednesday will be the most likely to push through into the gold and forex markets.

- Tuesday, August 6 at 12pm EDT: St. Louis Fed President James Bullard (FOMC voter)

- Wednesday, August 7 (time TBA): Chicago Fed President Charles Evans (FOMC voter)

And that’s how our week lays out, at least as of this morning. I wish you the best of luck out there, traders; and I’ll look forward to seeing you back here on Friday for a recap of the week’s market action.

Gold Price Chart

More articles from John Moncrief